Hi Jiten,

are you still invested in MOIL and NALCO?

Thanks and regards

As indicated earlier, I have sold 50% of MOIL and hold 100% of my NALCO.

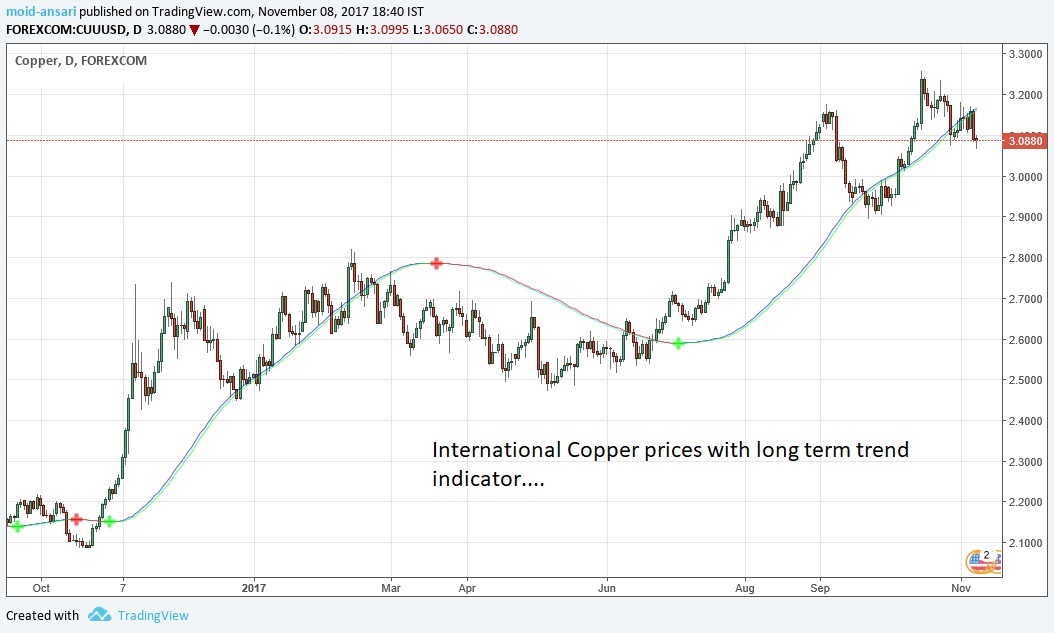

In my humble opinion, the best way to monitor a trend in commodity is to look at the technicals of the price charts of that particular commodity…and the worst way is to monitor it through newspaper / internet reports. Quite often, such reports are bearish at the bottom of the cycle and bullish at the top of the cycle.

Its not just pure coincidence that just when the news / internet reports started getting bullish on copper, the prices of copper in international market started correcting. Copper is now in a short term down trend, with in the larger term uptrend.

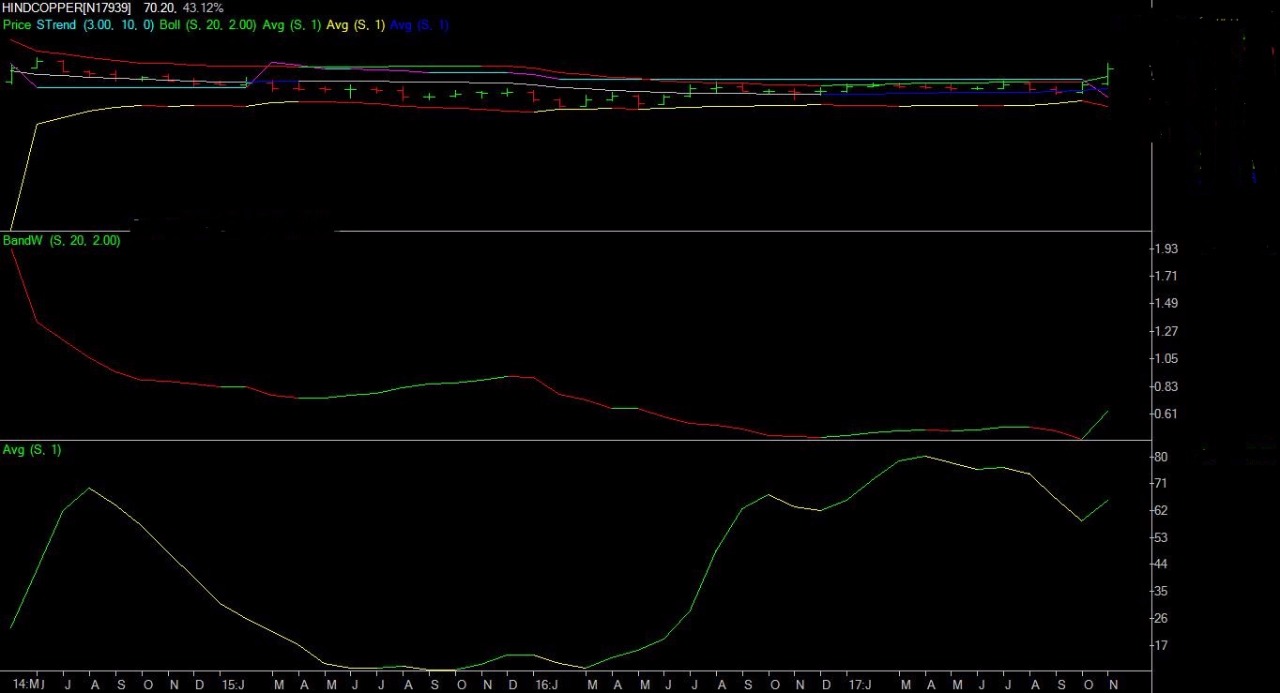

Secondly, those in india have the option of only Hind Copper to participate in the turnaround in copper cycle.

I am hoping to ride the rally in copper through Hind copper…long term charts are showing signs of turnaround…and that is backed by uptrend in copper prices in India…

confirmation of the uptrend in Hind copper is …if the stock closes the month of Nov above 80…as of now its quite possible that the rally may fizzle out, BUT good Q2 numbers and prospects of even better Q3 should provide downside support.

Have a look at the long term chart of Hindustan copper…the breakout / turnaround should be quite apparent even to those not conversant with technical

@Mehnazfatima Technicals are aliens for me. However, i am interested to learn. Would you mind sharing the source of these charts? Are they paid?

Regards,

Suhag

Interesting developments in Hind Copper.

I would request one of the senior members to create a separate thread for Hind Copper.

Hi mahnazfatima

Can you please post charts of other commodities like aluminium, zinc, etc as also suggested by Jiten with your view about future predictions. That will help a lot.

Thanks and regards

How did you come up with number 80?

Things looking good for tea - http://www.business-standard.com/article/companies/assam-tea-to-see-higher-prices-in-2018-auctions-as-production-falls-117111600638_1.html

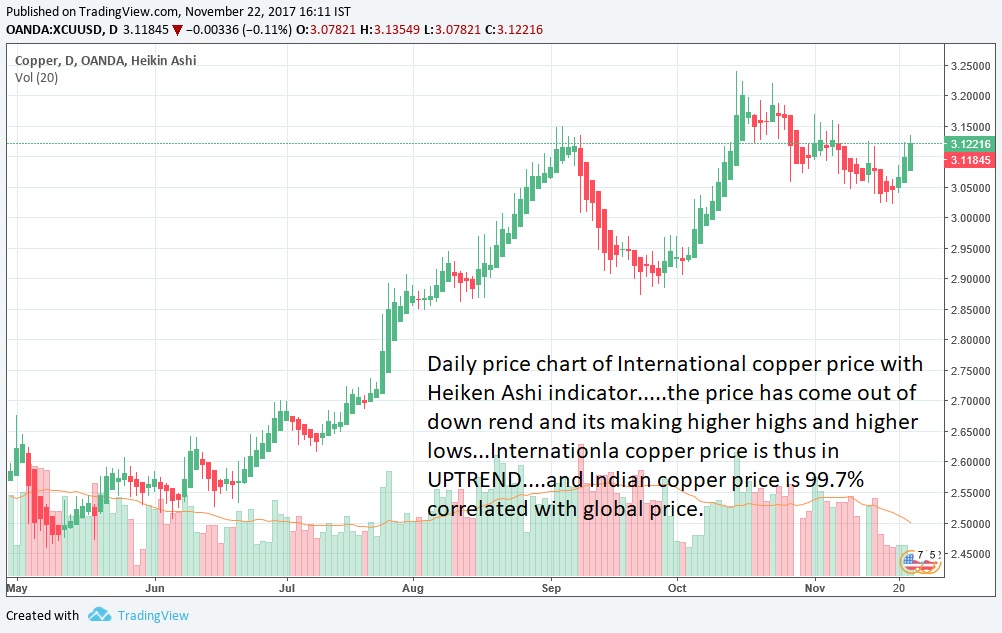

Looks like the uptrend in international copper price has resumed…or atleast the short term downtrend is over. just have a look at the price chart

@umang Joshi,

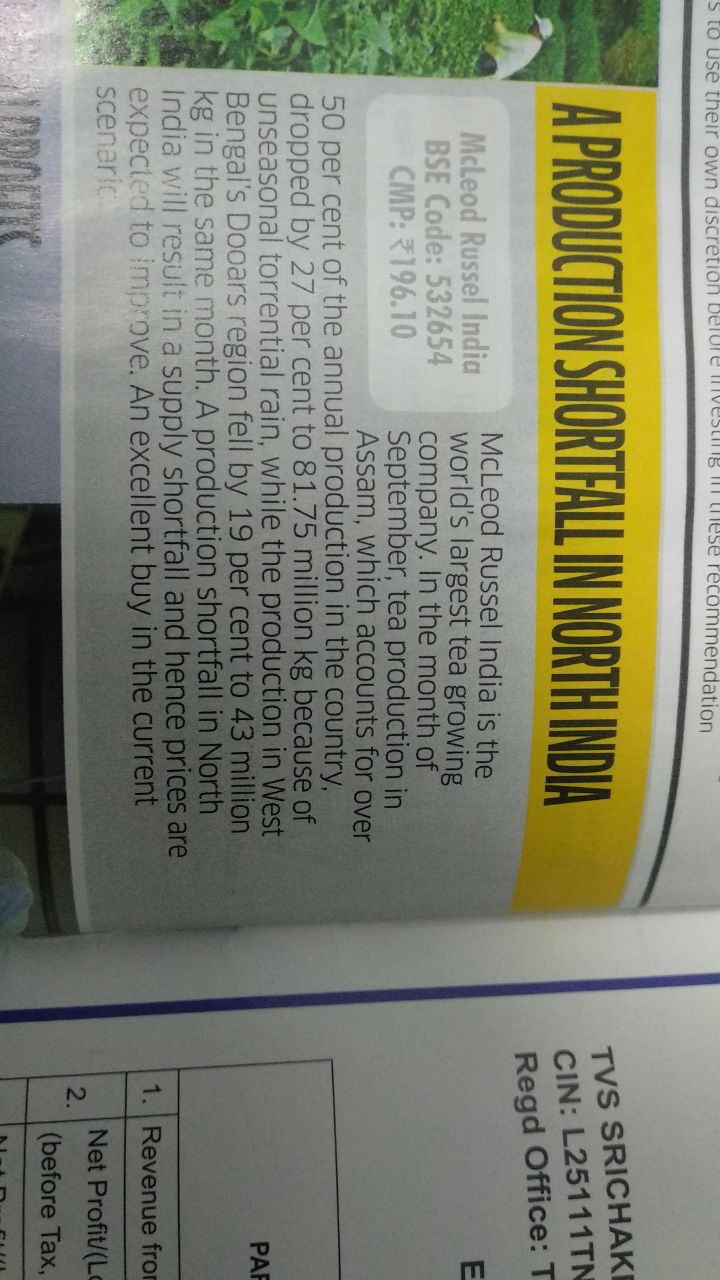

can you please analyse good tea companies. mcleod, jayshree, goodrick, dhunseri all started moving up. anybody having knowledge of tea sector can throw light on the good companies which can be added at early stage.

Frankly I am a green horn, but amongst the lot Mcleod is supposed to be good. http://old.sharekhan.com/Upload/NewsLetter/McLeod-Nov27_17.pdf

did some research. goodricke group seems far better from mcleod on almost all parameters (less Mcap/ sales, zero debt, better operating performance, etc). Jayshree tea Mcap/ sales ratio is lowest, but operating performance and debt of concern. however, if cycle really turn around, the company may become best performing. shri Jiten may guide us.

@jitenp thank you for sharing

Very positive interview, but he’s always sounded positive about the next quarter