nomura buys 9.2% stake in McLeodruss

Please do check who sold.

1 Like

I assume Nomura coming in would add some good management practices. Though Baheti was a kind of poster boy McLeod

@jitenp …curious to know whats your take on the logistics as overall sector? do you think its a good play for next 2-3 years?

Seems to have sold by CFO himself. Says will be used for deleveraging.

not tracking logistics sector closely enuf and have no investments. It should be a GST beneficiary. But many stocks are expensive. If someone can do some work and share, it can be good.

1 Like

Hi friends,

I am receiving many personal messages. Not sounding rude, but due to paucity of time, will not be able to reply to most of the messages. Hope everyone understands.

1 Like

Hi Jiten,

http://dipam.gov.in/sites/default/files/HINDUSTAN%20COPPER%20LTD%20-%20Corporate%20Presentation%20-%20Jan%202017.pdf?download=1

This old presentation by Hind Copper talking about expansion ( capital outlay 5000Cr) getting commissioned from 2018 December and will continue till 2023. I think , these expansions have potential to triple their sales in coming 2 to 3 years and contribute to the top/ bottom line and with significant cash flow. Only concern, if copper prices crash significantly, there will be down side , Nonetheless , chances are less likely, given that increasing global copper demand and limited ore supply due to EV, Economic development of developing worlds like India, China etc. Around 1000 odd Cr Capex for expansion has already been funded with Int accr and 400 odd cr debt. another 1500 required for mining expansion upto 2020. Excessive debt financing with low copper price could damage the balance sheet in future. However, scenario is less likely to be played out.What is your view on the copper for medium term, i.e coming 2 to 3 years.

1 Like

Disclosure: Invested 3% of my portfolio in hind copper recently

Here is update on trend in copper prices in India /MCX. On monthly charts, this is the first clearest signal thst copper is now in a bull market. There is a very strong bullish divergence and it may cause the price of copper to embark on the next leg of the rally.

Hence, insofar as copper cycle is concerned, the uptrend in copper price got a more stronger footing.

Bullishness in copper price makes Hindustan Copper a very attractive buy on dips stock. Incidentally, Hind Copper is poised for a volatility breakout on daily charts. I am hoping that it will be an upside breakout. Bullish copper price reinforce my expectations of an upside breakout in Hind copper.

5 Likes

Hi Jiten

Do you track Tea companies? Have any views on tea cycle?

Should we start a new thread on tea stocks.

Apart from supply shortage from Assam is there any more trigger in tea stocks.?Views are invited

Stay cautious of punters n painted news of shortage . M just sharing news,not sure of real situation

Check out @shyamsek’s Tweet: https://twitter.com/shyamsek/status/937159551333388288?s=09

Be Very careful. Even Vijay Kedia warned against buying. Punters are at play

@nil_71 @suru27 i am no tea industry expert but all these wise men have their own vested interest in what they tweet and preach.

Regards,

Suhag

I ve high regards for kedia Jee though agree with you . In this case , it seems he owns small tea planation business n has never tried to fool public ,so, I would trust him than people trying to punt. Anyone, one has to take his own call based on information shared. Disc : not invested in any tea stock

4 Likes

Though I invested only very less money in James warren tea (company is doing buy back @129 and I invested @147, so downside protection). however, why nomura will invest in mcleod @208, if the investment is not worthy. nomura is not novice/retail investor. almost all tea companies are at very low profit margin. tea prices this year are at higher level in comparison to previous year. so condition in ripe for turnaround in tea stocks. views are invited. will trace the sector.

Obviously Nomura has better finances, knowledge and network than us to invest in a particular stock. However, just following them for our investment decision is a recipe for disaster. Let me share you one example which i have closely followed. During the infrastructure boom of 2004-2008 many respectable PEs invested in GMR infra via QIP route multiple times. GMR infra kept on creating assets (Of course debt along with that). You can easily see where GMR infra is now. How much money those PEs would have made (Lost?) is anyone’s guess here. There are many such examples in market.

Hope this clarifies.

Regards,

Suhag

1 Like

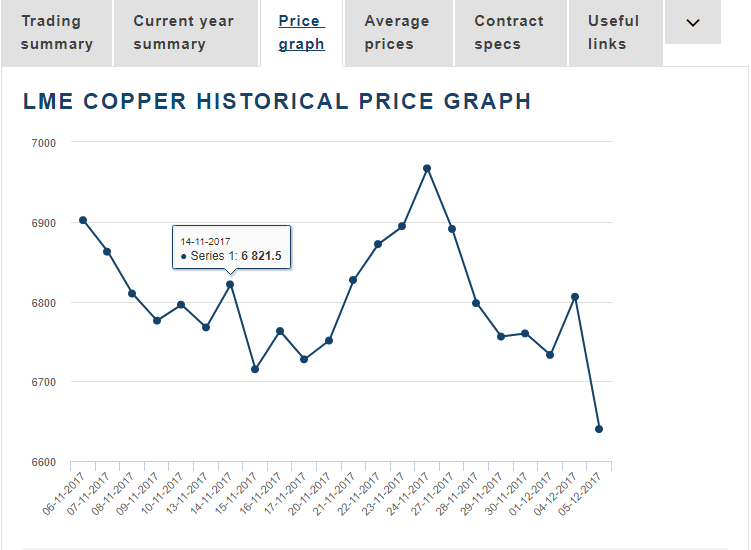

I have been tracking Copper prices on LME site. From the highs of mid sep-oct, the prices have mostly cooled off a little. I assume that copper prices all over the world would follow more or less similar trend. Attaching current LME copper price chart.

Would you please advise why indian prices are showing a bullish trend while the prices on LME are flat to negative for some weeks now?

Regards,

Suhag

1 Like

Thanks Suhag for your views. I am not suggesting to invest based on Nomura investment alone. However, tea prices as reported on tea board site are higher on week to week basis in comparison to previous year. most of stocks are making thin margins. cost of production have gone up. loss of production reports in Kenya. all point out that the cycle is ripe for turn around.

the twitter posts of vijay kedia and other big investors has taken out steam and punt. now, the stocks will perform based on fundamentals. let us see. keep a close watch on the auction prices. production of tea is also important. same should not go down drastically. slight dip is beneficial.