I remember Page Industries promoters Genomals regularly selling their shares in the open market a few years back (small quantities). Someone from the Chamal Lal promoter family is also regularly selling a few hundred shares in the last few months and it somehow reminds me how mistaken the promoters can be of the worth of their own shares (I think Page Industries is up 2 to 4 times since the promoters started selling their shares in the open market).

They maybe selling shares because of their own personal reasons,like buying house or other small biz .

As i saw in the q4 pattern uploaded, One of the several very small holding promoter individual sold entire stake and a son of the two main brother promoter sold a small part of his holding…I think two quarters back a trust promoter of escorts ltd sold a good quantity…stock has gone up big time from that level…promoter may have access to inside info but stock valuation is not something that he is an expert in…best is to ignore unless major selling is there …

Simply going by the export data and the fact that CLSE’s revenues are from 80% exports, there is a good chance that they could post numbers better than Q3.

Export numbers shows a strong uptick in both QoQ and YoY for Q4. KRBL’s export volumes moved up as well in the quarter, however since their export contribution to topline is only 40%, the numbers didn’t show a visible jump there (also since they lost domestic business to compensate for the exports rise).

CLSE should theoretically show a jump in revenues but they don’t disclose the countries they export to. From older reports for Maharani brand rice exports on Zauba, the countries were Israel, Mauritius, UAE, South Africa, Canada and many others - These top 5 countries have shown a 60% rise in exports for Q4 (Most of the contribution though is from UAE). If they don’t export to UAE anymore, the thesis may not hold out and there is no way of knowing. However I suspect the numbers for Q4 should be quite good and they should do a topline of over 200 Cr like they did in Q3. Margins might be similar or even lower as well since CLSE is more a trading type company and prices have gone up now.

Disc: Have taken a position in the recent fall near 200 DMA

6 Likes

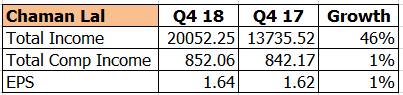

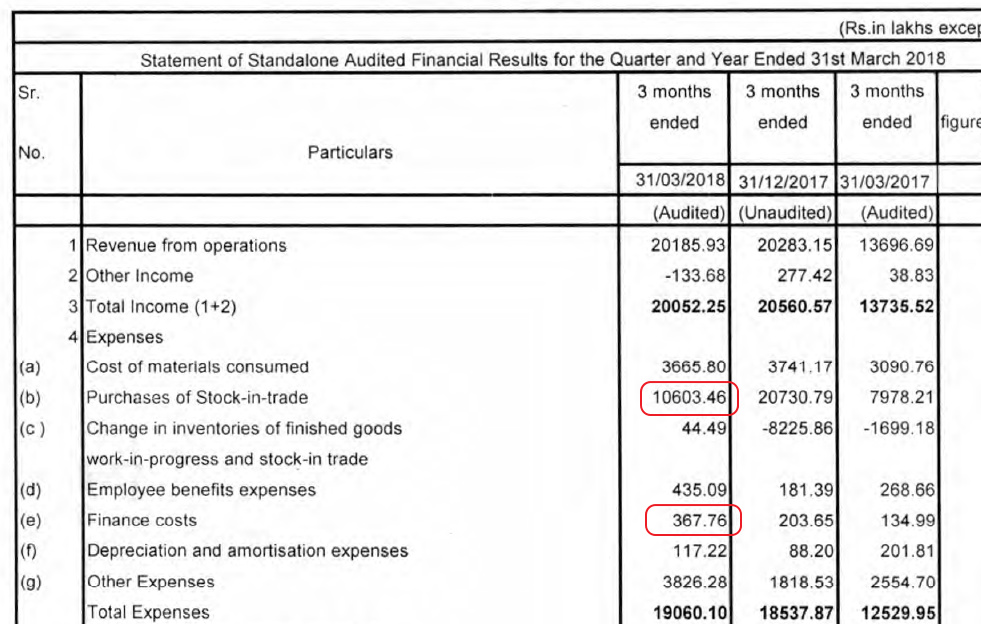

Q4 results are out. Good growth on the revenue but profit has taken a hit due to more expense on the stock-in trade and finance cost. @phreakv6 Your view on the results will be helpful.

Additionally: Other expenses have shooted up to 38.26 Cr i.e.100% (QoQ) and 50% YoY ! Other income is also negative at -1.33 cr !

Any explanation towards this will be highly appreciated.

employee benefit expense has also shot up

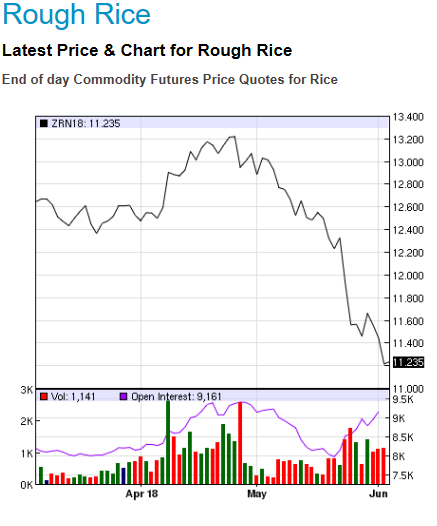

http://www.agriwatch.com/getarchreportpath.php?db_product_id=200041&type=f&file=UmljZS1Nb250aGx5LVJlc2VhcmNoLVJlcG9ydC0yMDE4MDQwNS5wZGY=

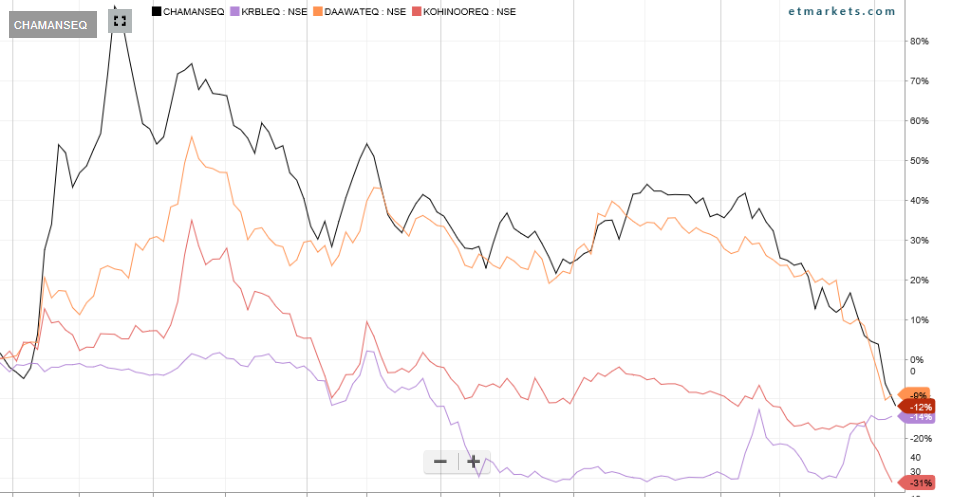

The sluggish perfomance by the major Rice stocks is mainlly due to

1 There is more of supply of rice than demand cuasing the globl rice very compeitive .

2 Indonesia /Pakistan / Bangla Desh & Thiland’s Rice production in 2018/19 is forecast likelly to increase rice due to better yield from less pest and disease incidents and larger harvested area.

3 Recent change in the Muthal funds they are dummping the small caps in the open market leading to panic selling by the small time retail investors.

a snip from Nasdaq https://www.nasdaq.com/markets/rice.aspx

Discl; Invested in the CLS

3 Likes

Concall Summary FY18:

@ayushmit please add if i have missed anything

Industry:

- Lot of industry players have gone out. REI, Laxmi. Even Kohinoor is in difficult position.

- One of the big customer in Iran has defaulted on payment. Total hit is around 1500-2000crs.

Company:

- Added 107 customers internationally this year.

- We focus on smaller consignments, smaller customers and more countries

- Max 300days we can run in an year. 5-6 lakh quintal we can produce.

Paddy Prices:

- In Mar, prices were 33.5/34 per kg. It has gone down to 31-32 currently

- New crop is yet to be sown and hence we don’t know if prices will go down further

Customer profile:

- We are present in 83 countries

- We are also looking to grow in the US. Lot of meetings are lined up

- We had good traction in Canada, Middle east, Africa last year. Have not been doing business with Iran for last 5 years

- We don’t directly supply to supermarkets and chains as there requirement is daily or even on hourly basis. Hence they prefer to buy it from distributors. We indirectly supply to supermarkets through distributors.

Volume sold:

Maharani brand:

- Sells in 34 countries.

- Total branded sales is ~20%. (My comment - not too sure if this is only for Maharani because in background chatter, I heard branded sales is around 30-35%)

- Registered with Amazon. Will be doing online sales.

Margins:

- Margins have come down because our focus is on adding customers and increasing sales. Hence margins got affected.

- To get new customers, we even compromise on margins. At times, we sell at break-even or even lower.

- Going forward we will focus on margins as well.

- Branded sales have higher margins. KRBL sales 300-400$ higher realisation. We have good scope to improve. Sooner or later it will come.

- We have started aged rice as well.

- Gradually margins will grow but will take time.

Currency impact

- This affects margins on both the sides

- We factor in atleast Rs. 1-1.5 in currency when we take the order.

- 30-35% we book short and long term (forward contracts)

Balance Sheet

- Debt has gone up because topline has gone up and we had to maintain high level of inventory.

- Recievables had increased because of increase in sales. (not too convincing as they hardly give credit to customers)

- Currently we are again debt free. (this is likely because they debt was taken to buy the inventory and it has cleared by now and debt has been repaid)

Dividend

- We don’t pay high dividends because we need to hold cash for better pricing of of raw material.

- We get 2% cash discount on buying inventory on cash basis. (generally payment is made within 7days)

Guidance:

- Management expects they should ideally grow at 20%.

- Focus will be on margins as well this year

15 Likes

@Multiplier777 They have bought back again,check latest shareholding @kunal What is the utilization of the company?Will it need to add more capacity to sustain 20 percent growth.

Hi, any idea on how much does it affected CLSE ?

@manivannan.g

They had stopped dealing with Iran for past 5years. So not affected

they dont give utilisation numbers in % terms as such. but this is what they said on the call. 5-6 lakh quintals they can produce. Rest I assume would from outsourced units.

3 Likes

Sorry 6lackhs quintals per year?

So basically company is at half its utilization according to the 2017 production.

The number of quintals of rice produced is all over the place from 3.24 lac in 2010 to 1.74 lac in 2011 to 3 lac in 2013 to 2.33 lac in 2014 to 3.13 lac in 2015 to 3.10 lac in 2016 to 2.98 lac in 2017.

The problem with this guy is the profit margins,these guys dont seem to have used the strategy of selling at break even before.So why now?Only way we can estimate the future is if we can estimate the opm.Will the opm go down more?

Thank you for concall update

Can you please guide on Promoter loan issue & as per my research Iran & Promoter loan were two issues.

if company is not into Iran thats a good thing as inflation in Iran has doubled .even pricing issues in premium quality rice.

Please share audio transcript on 9687972119

Latest credit update provides some good insights - http://www.careratings.com/upload/CompanyFiles/PR/Chaman%20Lal%20Setia%20Exports%20Limited-07-04-2018.pdf

9 Likes

Thanks @ayushmit. This was useful. I was trying to find the Q4 FY18 concall transcript; unable to locate.

Anyone having concall transcript?

Thanks & Regards, Ranjan

Thanks, It was helpful