Any views? https://www.bseindia.com/xml-data/corpfiling/AttachLive/01e6e276-3a0b-4d63-8eb3-48dd54d1dac9.pdf

The annual meeting will be @ Amritsar on 29th sept 2018 the annual report one can find at http://www.beetalfinancial.com/report/chamanlal_Ar18.pdf strong numbers in terms of sales ,borrowing increased

1 Like

- Found Mohnish Pabrai (Dhandho Funds) in Top 10 shareholders. I believe just a tracking amount (0.49 %)

- Salary + commissions of the promoters are v. high compared to Net Profit (6cr / 41.6 cr)

- Promoting Maharani brand will be one of the top priority of the mgmt

- Hot water is re-cycled leading to lesser consumption of water and energy

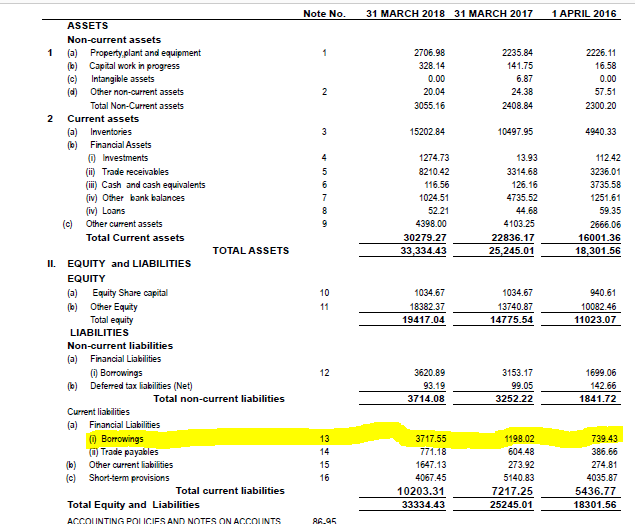

- Increase in sales is accompanied with increase in receivables

R & D Initiatives

a) Development of a system and method for parboiling paddy that obviates husk of paddy from splitting

b) Development of 100% insect killing technique by using 1/3rd of Pesticides

c) Development of quick cooking Brown Rice

d) Use of Neem as Bio-pesticide;

e) Improvement in Parboiling for improvement in quality parameters;

f) Use of Plastic Buckets in parboiling plant thus reducing cost;

g) Development of Bhatti Sella through automation for the first time in India;

h) Reducing broken in paddy with very high sun checks under process.

i) Rice bran stabilization for human consumption under process.

j) Making bio-compost from waste and reject of paddy under process.

“Bhatti Sella, Pesticide Residue free rice and quick cooking rice and Rice for Diabetic People having moderate G.I Sale is picking up in various directions of the World markets particularly the Maharani Rice suitable for Diabetic people” - as per report

8 Likes

Thanks Sushil for the notes. Chaman Lal is a very well-managed and a great company which has consistently reported very high return ratios and low leverage. This in an industry where every now and then, we keep hearing of rice processors/exporters going bust.

What is disappointing is the lazy balance sheet writing where they keep doing a cut and past job every year. Reading about their focus on promoting the Maharani brand can create a lot of excitement. Unfortunately they have been writing the same paragraph word for word over the last many years (I have balance sheets from 2010-11 onwards but I am sure they would have been writing the same paragraph in the earlier years also). What is hilarious is that the full stop is in the wrong place in the first sentence in each of the last 8 year balance sheets (laziness to even correct that).

2017-18 (Page 48)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand. The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

2016-17 (Page 37)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packaging’s of Maharani Brand. The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

2015-16 (Page 40)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand. The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

2014-15 (Page 38)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand. The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

2013-14 (Page 26)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

2012-13 (Page 8)

The promotion of flagship brand Maharani is on the top agenda of the Company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand. The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be the future strength and business stimulators of the Company .

2011-12 (Page 8)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come. Company has introduced very attractive and novel packagings of Maharani Brand The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company.

2010-11 (Page 8)

The Promotion of flagship brand Maharani is on the Top agenda of the company in the time to come .Company has introduced very attractive and novel packagings of Maharani Brand The Company plans to go for aggressive advertising in print and electronic media and brand equity is likely to be future strength and business stimulators of the company .

23 Likes

The increasing inventory has been a concern as it leads to higher working capital. Interestingly, this inventory picture is also very cyclical as they must be keeping higher inventory at March end which eases out by Sept end.

As per the last concall (which happened in June, i think) the company has already repaid the WC borrowing they had taken at March end

8 Likes

I have been tracking clse for a while now .The inventory is seasonal,the company here is trying to ‘time’ the market as it is expecting an increase in rice price going forward.It is not because the company is unable to sell.

The main putoff here is the low dividend payout.I know a lot of people would not mind it,but is there any justifiable reason why a company cannot pay atleast 10 percent dividend?10 percent of net profit to me is a reasonable amount.

Disclosure:

Not invested,following closely.

1 Like

Company has many times communicated on that issue , the final dividend timing coincides with the season of rice procurement whereby the rice prices are lowest plus they get 3% cash discount , so they utilise the dividend amount and add inventory at cheap and discounted prices.

1 Like

Rating advisory released by CRISIL. https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Chaman_Lal_Setia_Exports_Limited_RR.pdf

1 Like

This is not good. Company not cooperating.

Disc - Invested

1 Like

Hi @bimalb

This isn’t a negative in case of Chaman Lal as they have switched their rating agency from Crisil to Care, which is a pretty common thing in corporate debt rating. The last update that came in from Crisil was in 2017 and post that company switched to Care which had published a rating report in July 2018. It is only procedural for Crisil to post this rating advisory.

One can access the latest credit rating report published by Care from here.

Hope this helps!

Regards,

Yogansh Jeswani

Disclosure: Invested

6 Likes

Its good but why crisil still issuing rating notices for them if they have already switched ? The care rating you shared is dated July 2018 and after that there are two notices by crisil in oct and nov.

1 Like

Any idea why the curtly result not good. Revenue has fallen steeply YoY when KRBL and LT Food have shown improvement in the same.

Disc. invested

1 Like

As an annual surveillance exercise, CRISIL needs to update the ratings assigned within 14 months and that’s why they need to chase the company for latest data. If they don’t receive the data within stipulated time-frame, they will either downgrade citing inability to take a call or suspend the rating. Meanwhile, the company continues to have a live rating from CARE. So, rating notices from CRISIL are more of procedural rather than something to do with the company’s business /financial performance.

Disc- Invested / Have worked at a rating agency earlier

7 Likes

India’s Rice export volume.pdf (353.3 KB)

India’s Rice export value.pdf (392.4 KB)

Source- businessline

Flat industry volumes

2 Likes

what is the source for it sir

1 Like

Hi Ayush ,

You are right but what I know about Basmati is that it need some time before the paddy get milled .There is approximate 60 to 70% yield is expected from the paddy . Since there is a long time lag between raw material procurement and liquidation of inventory, the company is exposed to the risk of adverse price movement resulting in lower realization than expected. Even after long years of operation company is not eager to expand itself may be PUNAJBI want to enjoy the LIFE along with the Business

Also they are not eager for front or backward integration operation May be they are thinking asset light Business But in the Long Run it affect the overall profit .

they can saving transportation cost by opening Kerala’s Warehouse But they are wasting the resources which they can convert n to value added products Like Bran il. Bran Cakes etc

Disc: Holding CLS But now at 38% loss Position NOTIONAL But enjoying the learning Curve

2 Likes

Update

Third quarter result out

Notes at first glance

As compare to last year quarter the revenue is less but the Profit before taxes reverted by the company is better than last year quarter

ePS improved as compare to last quarter

Tax paid and deferred both increased

1 Like

I wrote a small article one can find it at

4 Likes

Looks like an old one sir.

1 Like