Also, on the concall, management commented on a Q ‘is buy one, get one offer - is it leading to a loss?’.

Even at 50% discount (MRP 50g: Continental Extra , Rs 90: Continental Premium Rs 135), they are not making a loss. They are in the process of phasing out the discount.

Big retailers (my interpretation is DMart), are asking for private label coffee.

One of their premium customer, has bought their yearly quantity, in H1 FY18-19. In FY17-18 that customer had placed their order in H2. Therefore the earnings should be compared YoY and QoQ comparison does not shed much light.

Rise in ‘Total Other Comprehensive Income’, loosely reflects the depreciation of rupee.

Big retailers (my interpretation is DMart), are asking for private label coffee.

Dmart already has coffee private label. In my last visit to DMart, I was checking out coffees and saw DMart’s coffee brand (dont remember the name) and read the label to find out it was Mfd by Tata coffee.

Turnover stood at 292.11 Cr compare to 296.63 Cr same quarter last year

Net Profit stood at 47.18 Cr compare to 33.42 Cr same quarter last year

EBITDA stood at 77.62 Cr

PBT stood at 65.59 Cr

H1 Results

Turnover stood at 586.89 Cr compare to 545.94 Cr same period last year.

Net profit is 86.64 Cr compare to 73.46 Cr same period last year

Key Highlights

During the quarter company got some more profitable contracts from Vietnam which also contributed significantly to the bottom line.

Regarding the SEZ plant, company have commence trial production in the plant and applying for the necessary permission certifications by the end of quarter.

By Q4 company is expecting to reach all the client approval as well as certifications and company is targeting to start commercial production from 1st April 2019.

Also revising the guidance for this year from earlier 10-20 % bottom line increasing to 15-20 % bottom line. Top line is still expected in range of 5-10 %.

Q&A

What is company view on volume growth in India and Vietnam, in India company is running at full capacity in spite of company EBITDA grew about 20 % so volume growth was very healthy or production was far superior ?

In India company was operating at full capacity but company also started doing of little bit small pack orders this year which is also contributed to further value addition so there will be little bit of margin expansion also. Next year company is planning for a new small pack facility and company will go for more value orders. Company is moving more and more to small packs from bulk one and this makes the business more sticky because company supply to super market and brand owners in their brand name .

Does same Client base has been shifted to small pack orders or there are new client base ?

Company has get new clients for which company was applying from some years and that has translated into orders now. Some of existing customers also buying some additional small pack from company and that contribute to more sustainable profitability.

How is the volume growth in the Vietnam ?

15 % volume growth was seen in Vietnam.

What utilization and margin target is set for next year ?

50 % utilization target for next year with similar margin .

What has improved the profitability in the first half so sharp ?

Last year and year back company was mainly focus on the volume growth specially last financial year and company was adding new customers and that was the foundation for getting new customers on board and today whatever strategic decision taken by company last year that reaping is coming from this year onwards. Some of these customers whom company was supplying in bulk they has make the company a consistent supplier and started giving company small packs as well which also one of the reason behind growth this year as well.

How much percentage of business is in bulk and how much in small pack ?

70 % is for bulk business in India and 30 % in small packs in India

In Vietnam everything is in bulk.

So can high margins can be expected as more number of clients convert toward smaller pack ?

Correct

What is the advantage client get to shift from bulk to small pack ?

For them they have to now buy from only one single person earlier they were buying from resellers and company use to supply to resellers in different geographies. They use to pack the product at their place and then supply it. By buying directly from company is getting direct benefit of buying with manufacturers. So depending on the volume they buythey also get price advantage rather than buying from third party.

Will the margins will come down and volume will pick up because of new facility coming up ?

Not significant Company is introducing plant for free stride where there is huge demand and it is a premium product . So the purpose to open this new facility to expand company offering in free size not just playing like pure vanilla. There are range of products which is one of the reason why company is confident to maintain the same margins.

What has been the revenue for this quarter in retail business ?

For the first company had done 40 Cr revenue from the domestic market. Last month company have launched Maalgudi and this month Three in One and Three Mix. Company has started placing the product in the market . Company projection for this year is about 100 Cr and this Q3 and Q4 will give a clear picture of result of new product.

Does company have any plan on the expansion on the Vietnam side in next one year or two ?

Doing little bit of line balancing to enhance the capacity and this year company will reach to optimum utilization in Vietnam. So company need capacity expansion there so with minimum amount of investment company can do some line balancing and carry on to additional 3500 tons by next year. That will be ready by the end of FY20.

How much will be the new capacity of 3500 tons in Vietnam will cost ?

8 Million dollars on the higher side.

What would be the proportion of bulk and small pack in India business ?

A year ago maybe 20-25 % in India was in small packs and now it is 30 % and going forward it will pick up further more.

Is there any seasonality involve because the EBITDA margin shown spike in the same period last year ?

For this business on has to look on year to year basis because customer put order in one particular quarter. In Q2 company has executed some more profitable contract otherwise executed in Q3 or Q4.

On the material front the coffee prices are seen at all time low right now so how much the improvement in margin because of the product mix versus the declining trend in the raw material prices ?

Company business model is set in a way that coffee prices does not impact . Company cover on a pack to pack basis so prices volatility does not make much impact. Impact is on EBITDA percentage that increasebecause of turnover coming down. There almost a 20 % decline in the green coffee pricesin last year in spite of that decline company manage to make similar kind of turnover with 20 % additional volume growth also this year for the first six month.

On utilization level for first half , so will company continue with 95 % India and 75-80 % of Vietnam by then end of year ?

Yes

Will maintenance shut down will happen in second half ?

No it is already done in first half for 20 days.

Does company is planning anything on add spend in Hindi Media ?

No not in Hindi Media . Company is mainly doing into the south in Tamil , Kannada and Telegu. These are the three languages in which company is doing the add. Company is only targeting the southern states because their only company is selling the malgudi the Filter coffee. Big retail chains are also asking company to keep the Malgudi product in their stores because of very good response.

In terms of margins there is sharp improvement of 20 % in the first half compare to 21 % last year so any guidance on the margins ?

This is only appears to but the per Kg realization is still the same .Its only because of raw material priced coming down so it appears to be higher margin. So when the green coffee prices will go up than the margins will also come down.

How much will be the CAPEX for new facility of small pack and how it will impact the earnings profile ?

Inauguration of new packing unit by next financial year where investment is approximately around 12 million dollars in India and this is outside the SEZ in Sulurpay and company had already buy land few years ago so in balance portion company will set the facility.

SEZ plant is a separate unite catering to the export market . Company is setting up unit because of increase in volume in country and number of SKU company introduce in the domestic market has increased substantially. Apart from this company order for small pack in export market is also increasing. SO keeping these two requirement in mind company is setting up a DTI unit outside the SEZ unit.

Company is going to setting up a accommodation capacity of about 5000 tons and packing capacity of 3000-5000 tons. So their will be no additional product to come. There will be value addition come because of this expansion and this will be fully automated in packing.

What incremental realization expected ?

Around 5 % more because of the small packs.

Doe company get any INR depreciation benefit in terms of realization and better profitability ?

One that company is buying raw material in dollar and selling in dollar so this is a natural hedge . 70 % of the product cost is raw material and balance 30 % where company is doing the conversion aspect over there their would be a marginal benefit.

There were worry about the incremental capacity that are coming that putting the pressure on realization . Does that scenario change or moderated ?

Additional capacity is always their more than 50 % excess capacity in the past and even now the same situation, there are new capacities constantly coming on board as well. But one thing even the people building new capacity are realizing that just having a production capacity is not sufficient to generate sale. Working with coffee brand there is lot of R&D is required lot of product development is required. All this are quite expensive and time consuming. On top of all theseone need right partners and multiple geographies who can help to introduce the product in the market. Company have build relationships more than 20 year ago . Company has been able to get consistent repeat business because of that .So in last year also company would like to be more aggressive in the market and company was successful in adding more volume to company business. Now company is able to take the relationship to the next level as well. So this is an on going process. Going forward company don’t expect competition to reduce company have multiple advantage because of the plant being 20 years old and company also have lot of product development that company have done . Company have economies of scale. So these multiple advantages enabling company to be competitive. Going forward also because company is constantly adding capacity also.Company don’t see any problem to sell more volume in the future as well.

Did company mention that India base volume business growth is around 20 % this quarter for B2B business?

No there the volume growth range maybe 10 % .

Did the increase in CWIP is toward the Freeze capacity ?

Yes

Did the entire amount for that capacity has been spend?

No it is still under the capital working progress and since company has not declare the commercial operations.

What is the CAPEX requirement in next one year?

8 million is what company projected for improvement of line balancing at Vietnam which may add around 3500 tons capacity. Another 1 million dollar company is going to spend for agglomeration facility and atomized facility in India at Chittor.

Did the margins are better in India or Vietnam ?

In Vietnam because of better technologyand company is able to offer premium range of product from Vietnam.

What was the capacity utilization in FY18 ?

60 to 70 %.

What is the global production of Reobusta and Arrepca and their prices ?

There is a bumper craft in Brazil as well as Vietnam which is why the coffee prices are under pressure for the last couple of month. But in last week the market started recovering mainly because of the Brazilian elections and the party which is expected to come in power is more in pro business that’s why riyal started strengthening as well because of which green coffee prices also started increasing as brazil being the largest producer of coffee in the world. New news is coming that coffee rust is impacting the coffee but ground level realty is completely different. So the realistic situation will come to known in next year November only when the new crop tend to come.

Who are the company competitors foronline sales ?

There are competitors because in online sales company MRP in some case are higher than the competitor also. As far as product are concerned company product is significantly different from the competitors which are selling.

In India there is a Duopoly that is really natural such Nescafe andBru. So significant competition for them in the market is company own.Company is planning and growing the market also . Company is introducing lot of new product there is almost 15-20 % growth of coffee consumption within India. In India less than 20,000 tons is consumed today. In US they consume 80,000 tons , japan Consumes 35,000 tons. So potential for growth in coffee consumption is huge provided that company can also introduce product at a right price point. Company recently introduce a 3 in 1 mix at a 10 rs price point. So that a good alternate to even Tea. Company is also looking at the Hot beverage market.

Where company see B2C business as a percentage of total revenue ?

Today will be less than 1-2 % but hoping that it will grow consistently .From last year to now company B2C business has grown more than 100 %.

What is company advertising spend for FY19 ?

20 Cr

On currency benefit did company need to completely pass on the benefit or how does the pricing work their ?

It is not necessary to pass on but depending on whom company is targeting is there any Indian supplier who is supplying to that particular company so if that player is more aggressive than company have to pass on but usually that will not always the case because company is doing large volume across the world. The portion of people competing from India is very small. Company is more concerned about global competition and currency re-valuation is one thing that is not helping much because currency is revaluate in other countries as well so others are also getting the benefits as well. So competition is still there.

Any other CAPEX plan for FY20-21?

At this point of time company is planning for customer acquisition if things go well and volumes comes than company will go for another 10,000 tons of capacity expansion in Vietnam.

What were the export incentives for the quarter for the company ?

9 Cr in Q1 and 12 Cr in Q2 so it was 21 Cr in the first half year and company will get more in second half as well.

Of total Debt how much is for the new ChitorProject ?

180 Cr is the loan component and rest is all funded internally.

Does increase in PAT guidance is because of higher value added products ?

Yes

Does company see any attraction in US FMCG company ?

Company have already started supplying them but again there is small volume as of now. Going forward it will increase as they are asking for small packs. So company want to build some small pack capacity before getting into that business. That is also one of the reason company had set up packaging plant in India. Right now company is doing small volumes around 500 tons and it has potential of going up to 2000 ton but that again depend on multiple factor.

What is the margin gap between small packet and bulk packet ?

It depend on customer to customer and markets which range from 5 % to 20-25 %.

Who are company main competitors in instant coffeespace ?

There are several people across the world in Brazil there isSpecikii,Cocum ,Alcafee, Holam . Earlier there was Super, now there is a Chinese company called jiaHieeas well. In India there are 5-6 manufacturers. So across the world there are many geographies goring the coffee. There are lot of manufacturer already in the space. The highest capacity with competitor is 25,000 tons.

Kindly split the additional income between clients ?

Most of it is from Vietnam and they are new clients.

How much customer company is adding every year ?

10-15 customers every years minimum out of which higher volume wise there will be 2-3 customer every year.

How is the sales broken between existing clients and new clients ?

Existing clients keeps increasing their volumes with company. In some cases if company add one new customer than after 2-3 year the volume can go up by 50-60 % with the same client. Because initially they want to test the company. Because last year when company had added one customer there was one deal of pure vanilla base so it was not very complicated and now they have confidence and trust so that company can supply whatever they want within the time frame. They increase the products to small packs and other products as well.

Any particular reason for increase in personal expense ?

On commission part company is provisioning it on month to month basis.

What explains the increase in demand for agglomerationcoffee ?

In India , there are mainly two products one is pure coffee which sold by Nestle and second is trade ride powder which is sold in Chikri coffee pack by Bru. Company has introduced an continental extra which is an agglomerated straight rise coffee and volumes in this product is also increasing in the domestic market. So base on the projection company need to double the capacity by next year. So that is one significant reason. Apart from that company have some export customers also once company started doing more of small packs, most of the customers are asking company to supply it with agglomerated coffee. Earlier when company use to do company have to give straight rise powder. Agglomeration needs to be done by the reseller and than they use to sell to the customers. So company is now doing both agglomeration and small packs by own. Out of 7500 ton of global market of instant coffee market around 3000 tons would be Nestle and they are right now selling everything in agglomerated coffee. So any one who want to compete Nestle has to continue with agglomerated coffee.

How much is the global freeze rise capacity and how much is coming going foreard ?

150-2000 tons may be freeze ride consumption today in the world. At this point of time there is sufficient capacity to meet the demand. If freeze ride mix is increasing than automatically capacity has to increase. Company is seeing good growth rate because people across the world need more premium product under the freeze ride head.

Will be there any decrease in margin in second half ?

No because some of the most profitable product are construct in Q2 itself. Q3 and Q4 will be same as last year Q3 and Q4 almost. If things pan out properly than guidance will be hitting on higher number basically.

Any update on the Tax holiday in Vietnam ?

As of now company did receive an extension and same Tax holiday is continuing now.

Any update on the customers that company had mention from the continental ?

Volumes has been sold in the market and company is seeing very good relationship going to build over there. It is small in size right now.

Out of 150 Cr of CAPEX how much company is looking for raising ?

Mostly it will be done through internal accruals only.

Is there any Tax differences for the new plant in Chittor ?

Yes there will be and only MAT has to be paid by company.

What is the other comprehensive income of 25.44 Cr?

It is on consolidated basis. Company have the investment in the Vietnam subsidiary and Telegu subsidiary where in at the time of investment the rupee and current rupee price there is an appreciation so that stand at 25.44 Cr.

The operations from Vietnam should give similar margins as witnessed last year.

Target to increase domestic business revenue to Rs 100 crores from Rs 46 crores in FY19

The per kg production costs for the company are lower than the Brazilian counterparts because India

allows duty free imports of raw material while Brazil does not

Expecting volume growth to sustain around 10-20% for the next 3 years and post that the volume growth

will be coming down

The company wants to focus on the domestic branded business to be the next lever of growth post the

growth in current business slow down

The competition in both freeze dried & spray dried will continue to remain in the future as well because

new plants continue to get added

Whats so special about Ccl Xtra? How r other brands performing in Indian mkt ? How is the distribution reach of Continental so far? I am unable to find it in Ncr region .

A word of caution on this. It seems to have characteristics of a story stock/value trap.

It showed up on my screener for being relatively underpriced by this bull market. But it seems there could be several reasons for the market ignoring it.

Market probably expects its forex-arbitrage business fuelled margins to decrease going forward due to this aggressive Indian retail foray and initial investments involved. Question is its retail bet really worth it?

Company doesn’t seem to own its raw material and competition in retail coffee is stiff from giants like Nestle.

AR note also states that CCL will seek to increase packaged coffee consumption in (south) Indian consumers. It sounds like “market making”.

Market making is expensive and shareholders must not pay for it. Let giants like Nestle do market making. Product innovation doesn’t always pay off wrt expenses - trust Nestle to have studied the coffee market for viability of these new products/extensions. Question we must ask is why Nestle did not do what CCL now aims to do with the resources and data available to them?

Is there also a concern about the potential market size?

With focus on south india, is it a big enough market to be viable? Especially given the trade off versus CCL’s past lucrative high margin business?

I don’t think it is good to assume any stock as a value trap on the basis of prices not moving up or market not rating it. I don’t think any company owns its raw material. They all procure it. No doubt , there is a stiff competition from Nestle.

The company recently introduced instant Coffee “Continental This” and other products. They are introducing new products under their brand. It takes time to build a brand and i think it is already a good brand in South India.

Coming to North India , i have seen the Future Consumer Coffee (Big Bazar) is manufactured by CCL. Though it is not much visible under Continental brand.

I have seen some sachets of Continental coffee in Hotels in Surat as well as in some other places. They are trying to penetrate into North.

Their operating margins have improved over the years as well as the return ratios are good. Their is no equity dilution The cash flows are good. I don’t think there are any big/huge expenses towards marketing. It is all a part of predefined percentage for marketing. Every company needs to spend these to stay relevant in market. Nestle still does marketing for its brands.

The multi baggers are always made in companies like this where you have to take calculated risks and trust the management while for compounding it by 10-15% , One goes for nestle which are very visible brands.

Questions remain : How big the coffee market is and what CCL is doing to gain the market share.

I believe that market is very big to accommodate several players. The export market has a good potential where the coffee consumers base is very strong. CCL was earlier focused on B2B in many areas but now the intention may be to increase the market visibility of their own brand and thus going for some B2C too which looks better margin business. I have heard that the brand is visible in South and many people are finding the products in North too.

Disc: Invested and opinion are biased.

CCL is doing a business of 50 crores here which is 2.5% of the market. So the potential to grow domestic branded biz, assuming they capture 50% market share will be 20x. Assuming a price to sales of 2.5x, this business can approximately add 3000 crores to the market cap.

The legacy export business does ~ 1200 cr sales now and has a m.cap of 3500 cr.

So even in the best scenario, the domestic business may just end up doubling the current market cap. (Assumed export biz is low growth)

PS: Above are just very rough, back of envelope calculations and not precise. Also, the instant coffee market could grow really fast in the future.

I disagree with one point that the ratios are getting better. The standalone ratios are showing J curve and return ratios have decreased on standalone basis. Regarding ratios, two things to consider are increased leverage due to capex and also advertising/marketing expenses. Marketing expenses will be higher for an incumbent that is targeting premium categories like arabica and Nestle will always enjoy premium pricing like it does in other value added fmcg products. This is why size of pie is as important as is to draw customers away from Bru, Nescafé to CCL which should incur higher than normal marketing expenses. Capturing 50% market share is too ambitious a target.

They currently pass on spot price risk to buyers but if they own the instant coffee they sell, they may no longer be protect themselves 100% from fluctuations in raw material and currency prices. Going forward you may not see steadiness in return ratios as in the past.

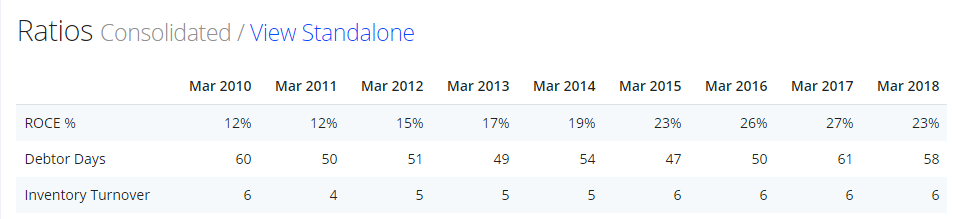

If one will look at the Ratios ,

The ROCEs have improved from 12% to current 20+% and are at same levels in last 4 Years

The debtor days have been in the range of 50-60 Days

The Receivables to Sales are in the range of 15-16% from last many years

The Asset Turnover has improved from 2 in 2014 to 3 in 2018.

There is no dilution , the debt is in control and balance sheet looks strong.

Though i have not compared it with September 2018 Data and even if it is somewhat lower in September 2018 , i don’t think such a short span of 6 Months is a good criteria to judge the ratios.

It will be tough for CCL to compete with the Giants but one thing should be noted that they have been in the market from long (Around 1994) and have grown their sales at around 10% Compounded in last 10 Years. May be the market is big and growing or may be due to their innovation and low cost products. I exactly do not remember where i have read this but it was mentioned that the CCL Products are way cheaper than Nescafe and there is no difference in Taste of both the products.

Marketing expenses are usual in any course of business unless they get extremely high. They were offering One+ One free offer from some time but that did not incur any loss to the company. They are also going to phase out the offer slowly. I believe that the focus is on building the Brand and reaching out to customers as of now.

Just a general comment, if you are a coffee lover just taste the their coffee you will really feel the difference.I have tried some of their products for last one year (xtra, premium, speciale) and it is far better and strong as compared with the populer brands. I was earlier using nescafe and bru. Yes it may be my preference or taste but just check the user reviews on the Amazon and you can see more than 90% consumers have rated >4. If you have time please read the comments you will know the difference.