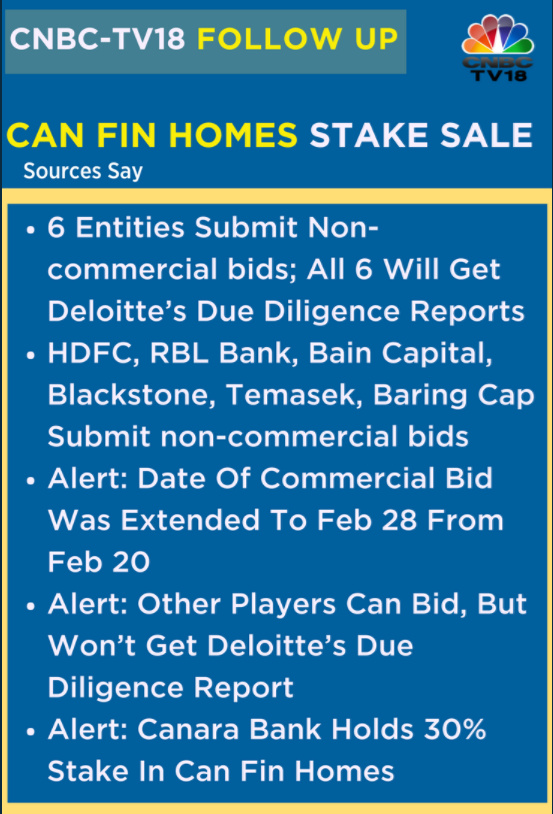

This is from CNBC TV18 Twitter handle

Continuous postponement of bid date indicating that Bidder is not ready to pay what Canara Bank is asking. Offer Price could be much lower from current stock price.

Views invited

One of the reasons mentioned in CNBC TV18 last week was that the process as such needs more time - For Deloitte to prepare the due diligence report, for bidders to do their own analysis etc. Let’s wait and see

The reasons for date extension (as mentioned in CNBC TV18)…

M&A is a complicated process and 8-10 days can happen for a variety of reasons. We should not read too much into it. It is still a non-binding round. Post this rounds the selected bidders will get access to for Due Diligence which should take another couple of months.

The news article says that the commercial bids are expected by Feb 28th. Hope the process doesn’t take 2 months.

Well, if the bidders haven’t as yet got the Due Diligence reports then the binding deal will take time.

What is the significance of due diligence report provided by the stake seller? Do to the bidders not have theirs on due diligence reports?

Good point. Also Canfin being a listed company, most of the audit reports will be available in public?

Listed below are the major steps in any M&A process

- Phase 1 - potential investors are approached with a no-name profile of the company, generally via an investment bank. If the bidder is interested then he signs a Non-Disclosure Agreement (NDA) and is taken to Phase 2. This phase takes 1-3 weeks.

- Phase 2 - Post-NDA an information memorandum is shared with the bidders which gives them limited information to evaluate the asset. For Listed companies, most of this information is available in the public domain via AR, concalls etc. Post review of this information the bidders are expected to make a non-binding offer which is subject to detailed due diligence. Depending on the level of bids and other condition, few bidders are taken to Phase 3. This phase takes 1-2 months.

- Phase 3 - The bidders are given access to all the books of accounts and other information they need to ensure what the company is saying is true and that there are no other unknown liabilities which the company hasn’t disclosed till date. The bidders hire their own advisors to do due diligence. Sometimes in order to speed up the process, the company commissions their advisors who prepare an independent due diligence report that can be relied upon by all the bidders. Post completion of DD, bidders submit their final and binding bids. With some negotiations, a Share Purchase Agreement is signed, which is subject to regulatory approvals etc. This phase takes 2-4 months.

- Phase 4 - All the necessary approvals are taken and the deal is closed.

I think this process is somewhere closer to the end of Phase 2.

6 Likes

Amit, if we are to believe the source based news on CNBC TV18, the DD report by Deloitte is given to the bidders who had already expressed interest (at least as of yesterday). If this is true, perhaps they are already into phase 3?

Also, in case of Canfin stake sale, what exactly will be the difference between a commercial & non-commercial bid? I thought the only discussion part will be the price / valuation, which will be the commercial bid.

And Canara bank clearly wants to sell their entire stake, so that is clear - ownership, promoter part etc.

HDFC can just look at the market cap of its subsidiary - GRUH and bid for Canfin stake.

Not sure what HDFC would get by acquiring Canfin homes as it already has Gruh!

1 Like

Gruh primarily focuses on EWS section (and also LIG-1) and also prefer non-salaried class. Canfin operates primarily in LIG-1 (and LIG-2 to an extent) and prefers salaried class. HDFC operates at a band higher than that of Canfin (in terms of individual loan amounts). So Canfin fills the gap between GRUH & HDFC.

This is what I gather although there could be some overlaps.

In the latest quarter, HDFC itself had given lot of loans in LIG-1 & EWS. Perhaps this is a new focus area for them and perhaps wants to use Canfin to fill this space.

1 Like

Thanks @newone

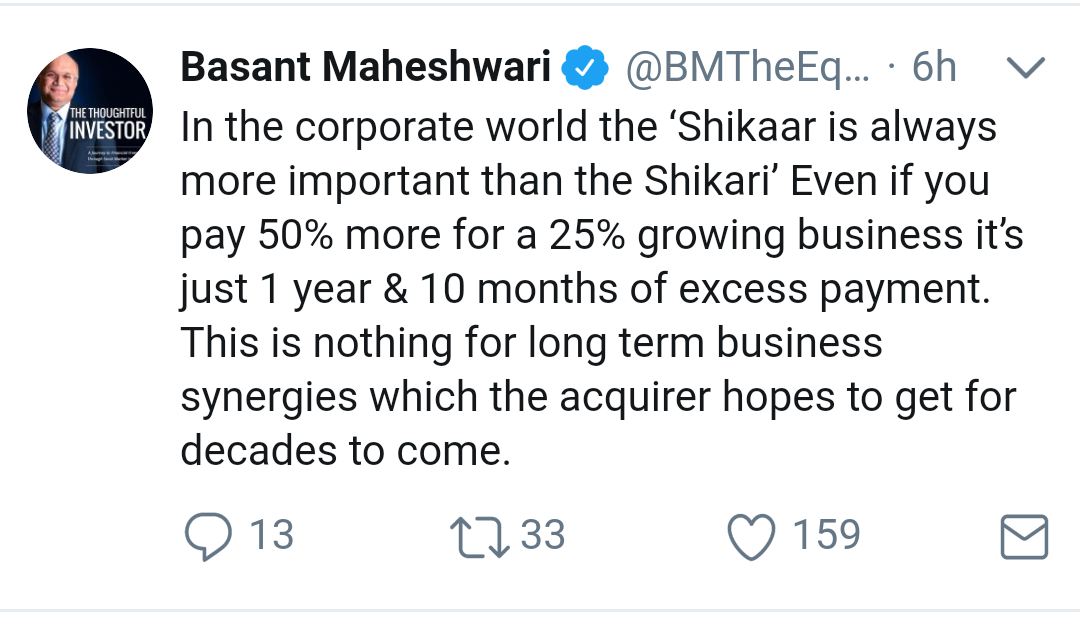

@sgjaclyn Yeah , we know the outcome by looking at past. By overpaying, once upon a time Tata steel also became shikar itself.(Shikari ,khud Shikar Ban gaya tha) . Pumping harms most to minority investors.

1 Like

@morigh82, it is not meant to influence anyone to buy or sell or meant to say the upcoming corporate action will happen that way.

But it is meant to make you think for yourself and judge yourself. If you don’t agree, you can happily move on. If you listen to him, read his wonderful book, you can easily relate to what he means by these kind of words. In fact in his book he even has a chapter on cyclical companies and if you followed Hitesh Bhai’s portfolio thread wherein he said in simple words “buy cyclicals when the PE is high and sell when the PE is low”, he expands it explains it to equip the reader with knowledge. So Tata Steel is out of question for a comparison with his qoute.

And again if you remember Charlie Munger’s words, they sound exactly the same.

Over the long term, it’s hard for a stock to earn a much better return that the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you’re not going to make much different than a six percent return - even if you originally buy it at a huge discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay an expensive looking price, you’ll end up with one hell of a result.

But we fail critically on one aspect that is to hold for a longggg… period of time, when the business is decent and may have its own occasional challenges, because we are impatient.

1 Like

Don’t feel bad Please. Somehow i did not like the screenshot of twitter you posted in this forum instead of doing analysis and self-view representation. BTW, if you follow peter lync you will also come to know that, every secular growth story also follow the cycle. People who were claiming Pharma is secular growth story in 2015, they now acknowledged it is also cyclical. We don’t know when this housing trend also turns cyclical from secular trend.

Which of these PE firms own companies which they operate on their own? If they buy entire stake - 30% from Canara bank, they become the promoter and hence have to appoint a new CEO and run operations as well. Do they have such companies in India?

PE firms - Blackstone, Temasek, Bain, Baring…