Situation has changed subsequently with interest rate increasing which is affecting the cost of funds putting pressure on margins etc. Also, if you see the impact of RERA in states like Karnataka is still present. Hence, spirits are not as euphoric as earlier due to changing macro factors. Hence, have subdued my expectation

with a P/b multiple of 5.5 giving a valuation of 550.

1 Like

Can you give the source for this information. Thx

1 Like

Also the comparison with GRuh is not valid. GRuh works in different category of borrowers so has pricing power. Can fin does not have any pricing power. Lending is commodity business. Now interest rate cycle has turned up, we will see less PE, Less P/B and less NIM regime here onward. Please think over it. Only favour I see in can fin is small size of loan book and long runway. Return ratio wise I don’t see any benefit.

Disclosure - Invested from lower levels.

2 Likes

I have generally seen on this site that only facts and figures are presented along with opinion sharing by experienced boarders when sought.However your mail, though may not be intentional,appears to be speculative without evidence wherein some boarders may get influenced.pl remain within the core objective of this forum

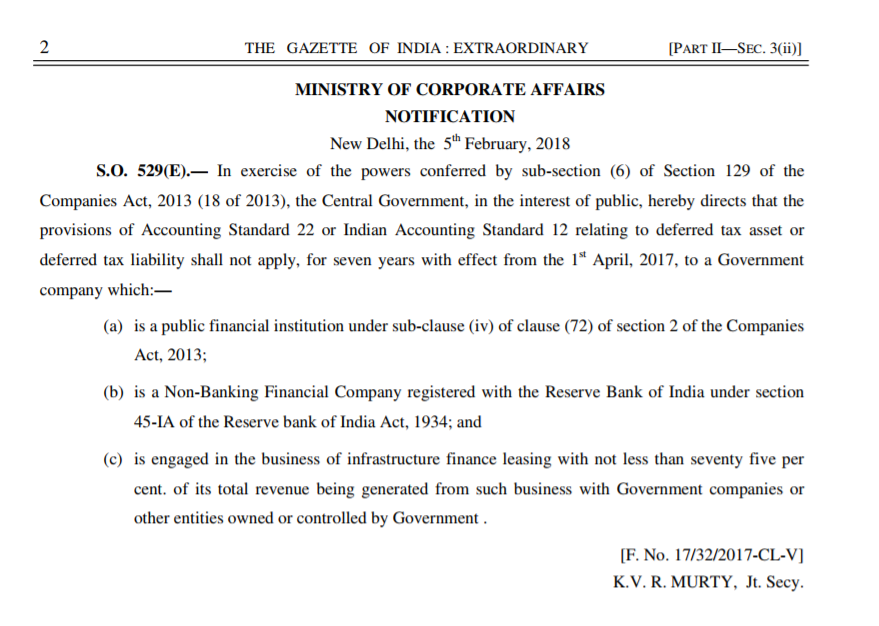

Just saw in TV (BTVI) that Deferred Tax Liability is removed for NBFCs for 7 years effective Apr 2017. So the bottom line of Canfin increases to that extent?

1 Like

Basant Maheshwari: Absolutely… but any of them 10 per cent lower, buy them now. If they fall 10 per cent, you do not lose sleep. You can just keep quiet and wait from them to go up. I mean these are the kinds of portfolios people are supposed to build. Of course, I do not own them because we own our HFCs and one of them should see a big corporate action in another next 30 days. We are waiting with bated breath for that as to who is going to pick up. If the girl is beautiful, she will find a boy. That is not a problem at all.

1 Like

1 Like

Does anyone with knowledge in this area (DTL) share his / her view on this notification? Does this apply to HFCs like Canfin homes? The DTL provision for 9 months of current FY is around 19 Crores.

The reading suggests that the exemption is available for Government companies only. CanFin should be a private entity. Would have been great though!

If such rules are applicable to Canara bank, will it not be applicable to its subsidiaries?

1 Like

CanFin is not Canara Bank’s subsidiary. It is majority owned by private entities; so, a private company.

Hi Pranav

Canara bank is the sole promoter of Canfin with 30% stake and is also the largest shareholder. The 2nd largest shareholder is Caladium (part of GIC Singapore) with 13.45% stake but they are not part of the promoter group.

http://www.canarabank.com/english/about-us/subsidiaries/

Canara bank’s promoter is Govt of India and hence it is a government organization. I just find it little difficult to understand why the subsidiary of a government organization is not considered as a government organization

my understanding of a company called a govt co is when min 50% of ts share holding is held by govt company

3 Likes

Another big PE player - Blackstone has met with Canfin management today. So, overall 12 companies have met so far incl. HDFC, Kotak and 8 big PE companies. The MD of Canara bank would be overwhelmed by now?

3 Likes

How does the bidding process work? How it correlates to CMP?

I am really looking forward to see if it continues to be listed.

I went through the concall transcript of Canfin. The thing that impressed me the most is that they donot wish to chase growth at the cost of quality. However, in reply to the question of how do they plan to defend their NIM’s in the face of rising interest rates and increasing competition - their reply was they 2 avenues of doing so

-

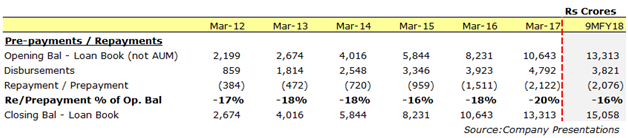

Increase the rates on Housing Loans - as most rates are floating. However competition is catching up - as can be seen in the Pre-payment / Repayment %

-

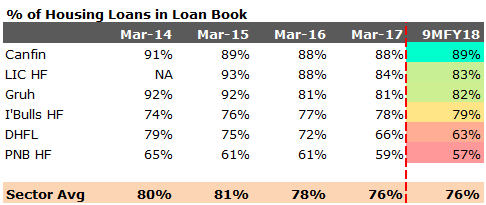

Increase the share of Non-housing Loans (12%+) which yield higher rates compared to housing loans(8.5%+). However, culturally Canfin has not been able to increase their share of non-housing loans as can be seen in the following chart.

Defending the NIM’s will be a key monitorable for the company going forward. Also, a strategic promoter who is a Bank (Kotak bank) or HFC’s (HDFC) will be far better off for the company compared to private equity player.

2 Likes

True, hence the stake sale is coming in at the right time. Hope Canara bank makes a good decision looking at long term. In my personal opinion, HDFC is the best & natural choice as HDFC itself is in the same business and they have excellent management pedigree (not that other firms don’t have it). PE firms can make a better offer (in terms of price) which is also important for Canara bank as they need money. So a better option would be (as mentioned in some recent news article in economic times), HDFC can offer cash & its own stock to Canara bank, so canara bank can sell the HDFC shares later at a higher price.

Point to note is: Just one day before that news article was published, Canara bank made a resolution to raise additional 1000 crores (apart from 3500 crores QIP & 4800 crores from government)

Any idea about the dates by which Canfin / Canara bank management will come out with bid & decision details?

They will come on 22 Feb 18

CanFin Book value is 98. current p/b is 5.5 . Will there be any taker in this High P/B? Company’s fundamental is also changed in few quarters.