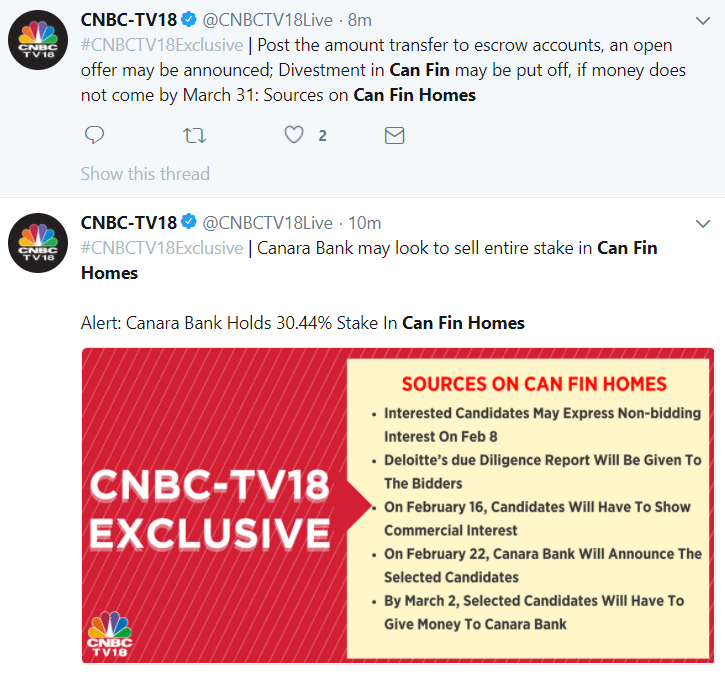

In the Q3 investor call, Canara bank MD had mentioned that they would complete the sale in the current quarter as they want to frontload all provisions to have a clean start to FY19

1 Like

All big names, they added one more to the list - T A Associates - another global PE. All put together,

- One HFC (HDFC)

- Two Banks (Kotak, RBL)

- 7 PE players (all big names)

- One AMC with a HFC subsidiary (Motilal)

Any guesses on the prices / valuations these firms would offer?

Personally, I would prefer HDFC as it is the only HFC in the list (and a mammoth at it), so buying Canfin Homes fits well into their core business strategy. And I believe Canfin business would fit well between that of HDFC’s own & that is GRUH.

Nothing new, but a good recap. The Canara Bank stake sale is wrongly mentioned as 4%.

So…When Canara bank sells its stake in Canfin Homes, do they have to pay LTCG?

The price as on 31st Dec 2017 would be taken as your buy price and any profit over and above it would be taxed as understood by me

31st Jan 2018 and not 31st Dec 2017.

Yes.thanks for correction

If it is 10 times the book, the stake sale should be at Rs. 1000 per share. The book value would be around Rs. 100 by March 2018. So a price of 550 will be 5.5 times the book. I too hope that the stake sale is done at a good premium as the buyer gets to be the promoter of a decent size HFC with excellent business metrics and high growth potential business. Hope the current market correction doesn’t have any negative impact.

1 Like

I agree with your content but not sure if the end message with tag “buy buy buy” adhered to spirit of forum.

I feel, Canfin has eveloved from a baby which was learning to a young adult that has super energy and waitng to run a marathon. Sad that Canara bank may not be able to reap whats coming. Hope they will hand it to someone who could let it run, imagine India’s mortgage penetration is just 9% compared to Denmark’s 100% and UK 85% and China’s about 30% (and China’s story also has just begun). Govts push for shelter to all will catapult the home finance. Its inevitable the valuations will catch up. Just a matter of time.

Canara bank stake sale big opportunity for investors:

Can Fin homes has a comparable loan book of Rs 146 vs Rs 148 bn for Gruh, RoA/RoE of 2.1%/24.6% vs 2.1%/26.4% for Gruh and C/I ratio is contained at 14.3% vs 16.4% for Gruh.At CMP of Rs 430 Can Fin homes trades around 5 times book while Gruh trades around 18 times.

I believe that although Gruh deserves better valuation due to HDFC parentage and higher leverage the valuation gap should not be that big. Expect the current stake sale by Canara bank to be around 10 times book. Hence,expect stake sale to be somewhere around 550 levels at least 25% premium to current price.

Also if we see the privatisation case of Hindustan zinc in 1999, the bidding process resulted in substantial gains of three to four times for the shareholders. In Canfin also there is big opportunity with so many PE players, domestic banks and financial institutions eyeing a formidable player in the burgeoning housing finance industry. It is no brainer for me.

I agree Saurabh - apologies, rookie mistake

2 Likes

Glad that you took it in right spirits buddy

GRuh ROE is 30%+. Please check. It is not comparable with Can Fin.

Yes Roe is greater. Canfins RoE is 25 around now. If Pe comes it’s Roe will increase to 27-28 due to change in management etc. Hence in future it will command higher valuations. Hence there should not be such big a gap in P/B in next 3-4 years.

1 Like

Yes currently the p/b is around 4.5. I expect the PE investors to give premium price of around 550. Even if they give such premium they would benefit 3-4 years down the line giving them an exit P/b of around 10 since Roe and ROA would move up to around 28% and 2.3% as per my estimates.

If the business is so good and future looks so bright, why are the promoters interested in selling the business.

1 Like

It is the directive from the government to monetize non-core assets.

Why 550?. Before Canara Bank announced sale of their 30% stake high was 666(3330/- before split). HFCs are reviving from the effects of demonetisation, RERA, GST etc. Have a tailwind of Modi govt’s housing for all by 2022 programme. 550 seems to be a very low price. They are buying one-third of a ready-made growing highly profitable business with long runway, not stock. Hope a great management with big vision buys it.