Market does not seem to like the results…as of now, stock is down quite a bit

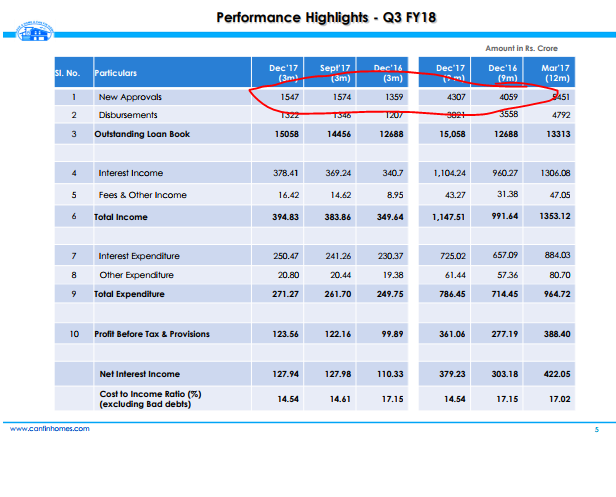

Q3 highlights

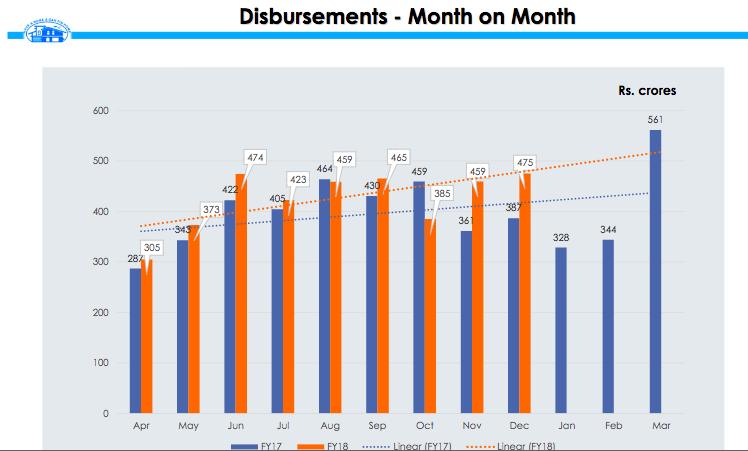

Fresh Sanctions in & Disbursements in Q3 up by 14% & 9% (Y-o-Y) resp.

Loan Book grew by 19% Y-o-Y and by 4% over Q2.

NII, OP & PAT for Q3 rose by 16%, 24% & 34% (Y-o-Y) respectively.

Cost to Income Ratio improved to 14.54% from 17.15% at Dec’16 (14.61% at Sep’17)

Gross NPA contained at 0.46% (0.40% in Q2) while Net NPAs stood at 0.25%.

90.5% of fresh loan approvals during the year were for Housing & 9.5% for Non-Housing

Average ticket size of incremental Housing & Non-Housing Loans are Rs.18 lakh and Rs.9

lakh respectively

92% of fresh approvals under Housing Loans are to Individuals with income below Rs.18

lakh of which, 40% to individuals with annual income upto Rs.6 lakh (LIG)

74% of the total loan book as at Dec’17 comes from Salaried & Professional segment.

Requesting Hitesh ji for analysis. Why market not liking this q on q growth after demonetisation, RERA, local Tamil nadu property registration problem etc. Management is consistent with their strategy. After demonetisation other HFCs are growing through LAP which Can fin Repco etc do LAP up to a limit only

May be the slowness in new approvals continues which market does not like. Also, quality of lending is undergoing a bit of dilution with % non-housing loans and non-salaried loans increasing but I think that is the call management has taken for growth as core segment competition intensifies

How much premium of HDFC vs Canara Bank as promoters is justified?

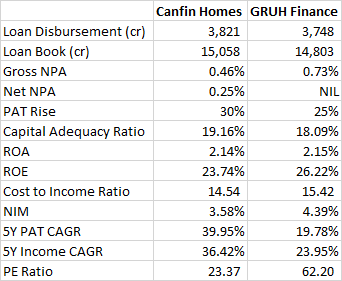

All data taken from presentations of the respective companies and is for YTD (9 months).

CAGR as per screener.

Price for PE Calculation - Canfin = Rs 485.6, GRUH = Rs 592.20

Disc: Invested from Lower Levels

this is about canfin homes… Capital first is another story… it was bleeding when it was a part of future group. After the new management took over it gave 7x returns.

Many things have already been covered, just wanted to share my 2 cents:

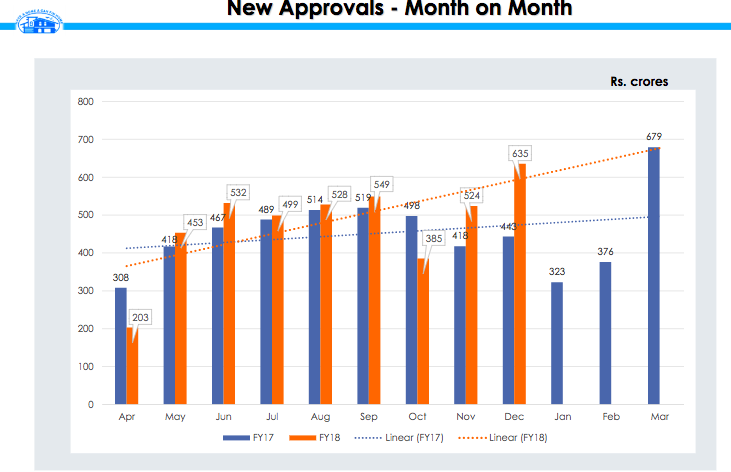

If we see new approvals and disbursements, these have picked up well in Nov and Dec. Percentage increase is really good if you compare all previous months in FY 18

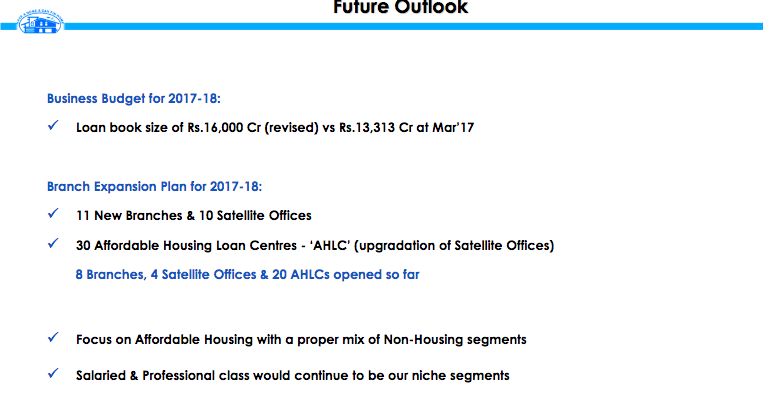

This time management has lowered their FY18 guidance for loan book from 17,000 to 16,000 crore. However this too means they aim to disburse about 2,000 crore ( considering Q3 with disbursements of 1322 the loan book grew by only about 600 crore) in Q4 which is very aggressive target considering recent past however if they achieve then it can somewhat cover up for the slow growth ( stock price and loan book) it showed last few months

I am not sure why markets reacted in negative after such a good result. Anyways if there is further drop, Perhaps its good for long term investors to grab more. More than the disbursement growth , i was more concerned with the LAP % and NPAs , i think none of them are out of range , when compared to the peers. 74% of the total loan book as at Dec’17 comes from Salaried & Professional segment is a huge thing which gives me more comfort on the asset quality side and perhaps the valuation. Increasing loan book is perceived to be fairly easy than maintaining good asset quality for which the market pays a premium. Overall I am satisfied with the results.

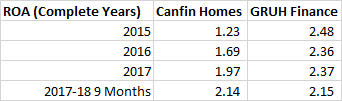

Most metrics look attractive now including price. Return on Equity is creeping up to 25% this year which defines winners from also rans. However, growth is a major concern. PBT has flatlined over the last 4 quarters and has shown zero growth. I hope this is due to weakness in southern markets due to RERA and demonetization. Tamilnadu is especially weak now. Hopefully growth improves fast or the stock will be quoting at 12-15 PE which is at least 30% lower.

It seems canfin & Canara bank management had met potential 30% stake buyers for 2 full days. all of them are highly reputed investors or companies, it would be interesting event to watch out.

I would be glad if they can sell their entire stake to Kotak, hopefully Kotak keeps it as is, as a independent listed company and builds on. I have been feeling, the current management though disciplined and ceonservative, are struggling to compete.

They may meet many more people over a long period before anything becomes final. It’s good news if Canara Bank still wants to sell its entire stake in Canfin.