TCI Express - Looks like accumulation is going on. Squeezed out of the downward trendline and is trading above long-term support in narrow price range with low volumes. Looks like a business with a very long runway and for a logistics business, they seem to be immune to crude as the OPM is in fact increasing YoY despite crude being high in Q2, FY18.

Shankara Building products has been on a free fall. Can anyone help with a good entry level using TA? Stock appears to be good to accumulate for long term? If the query is not proper on the forum, the moderators may please delete.

I have written to the company to find out more information on a lot of things. Let’s see if they get back. If this is driven only by Camphor price realisations, then it will die its natural death when cycle reverses. However, if the Camphor prices are sustainable at these levels because of structural changes in the sector, say increased pharma use of Camphor, then natural camphor being a product of trees, there is a possibility of sustainable numbers going forward - but the delta between RM prices changes and realisation changes will have to be watched.

There is one more angle here. Of the three Camphor players, Oriental Aromatics is valued higher probably because its also a play in flavours and fragrances and it has deals with some international customers there. Kanchi Karpooram seems to be a simple Camphor play while Mangalam Organics I think might be in the process of transformation. They have talked about branded retail camphor play in FY17 AR and they have kept their word and created brands Cam+ and Campure and are already selling well on Amazon at what appears to be very good margins. I see they are doing ad spends as well, considering their products show up in Sponsored products and also have “Amazon’s Choice” tag for Camphor. After doing some research on DRT, I think the deal with DRT could open up a lot of avenues for Mangalam to sell resins. If they make tyre resins for EVs in the near future, then they will be similar to a insoluble sulphur play like Oriental Carbon or a tyre chemical play like Nocil or a Carbon black play like Philips Carbon - this is of course just an optionality but very important to sustain higher valuations.

@mods - Please move the chain of conversation with @NamantS to the Mangalam Organics thread if possible.

Acrysil daily - At important resistance. Maybe this time it will have the steam to get over the line? 628 is the 52 wk closing high. The fundamentals are very good going by the performance in the last two quarters and going by the concalls, it looks like growth will sustain.

If the good performance continues, I think there is a good chance of getting there. Ratios are OK, debt is manageable but I think this is an early-stage candidate as ratios and debt will all improve if the business momentum they have built sustains. There is a 1:5 stock split as well coming up which could help the price momentum - I think it’s easier to jump the chasm of 125 to 150 than it is to jump 625 to 750 in this illiquid scrip and perhaps the management knows this

Disc: I have been building a long-term position here ever since I first came across it as I liked the story.

Not a stupid question at all. Their main costs must be fuel and people. If you see Blue Dart or Gati, their margins are moving with crude. TCI Express on the other hand is able to increase margins. This shows that they have pricing power to pass on the costs to their customers. It may have something to do with the quality of delivery (timeliness, security, efficiency) or the mission-criticalness of the bulk of the sectors it services (pharma, engineering, industrials) which makes these factors very crucial.

There is a big gulf in the operating profit margins of these companies where blue dart/gati are at 5% while TCI Express is pushing 11% which again emphasises this. I might be missing something else big otherwise but this is my reading based on the basic knowledge I have of the sector.

I would like to add 1 thing, such a difference in margin can be a red flag. eg. Moserbear in the past. Unless you are very sure that there is a moat or a competitive advantage to the company… you may want to watch out… I have never invested in Sun TV for this very reason. I wont say one management is fraud or accounts are fudged… However, such difference of margin on commodity type of business is worth investigating into.

Hi there,

You can broadly categorize transportation companies into integrators (Blue Dart, Fedex, DHL express) and logistics (freight forwarding, contract logistics, etc.). The former owns transport assets such as aircraft, trucks etc.and operate them on their own. Hence their margin and cost varies with oil price. This is typically 18-25% of operating cost.

On the other hand freight forwarding companies such as TCI, Allcargo, etc. sub contract transport to asset owners such as airlines and Ocean liners and hence usually can pass on oil price variation to customers with a couple of months of delay. This is via a fuel surcharge mechanism (hint: check your airplane ticket next time to look at how much surcharge you pay on top of base price.

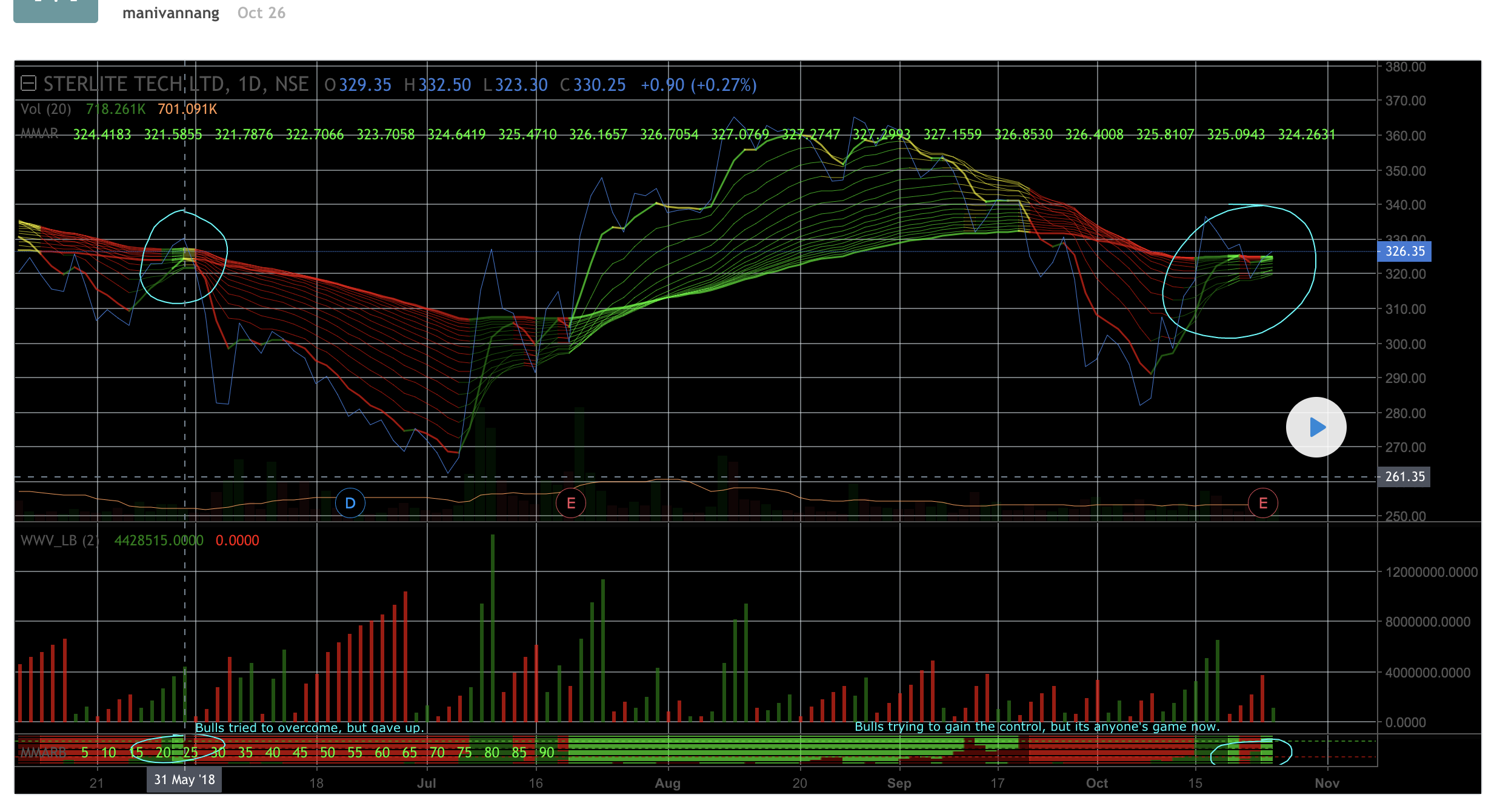

On weekly, one can see three white soldiers which confirms the uptrend for the coming weeks, also seeing this pattern in the recent past (just an observation, marked in the pink line):

I beg to differ. I think right now we are at Assurance stage. Already death cross formed with a down sloping 200 SMA. Have a feeling this rally will fizzle out at around 10800-10900 and there would be a resumption of downtrend around year end. The below scenario may play out.

I am not a TA expert and please take it with a bucket of salt.

Next couple of days are important, as that will confirm will the Green becomes lime, or the green gives up to the red.

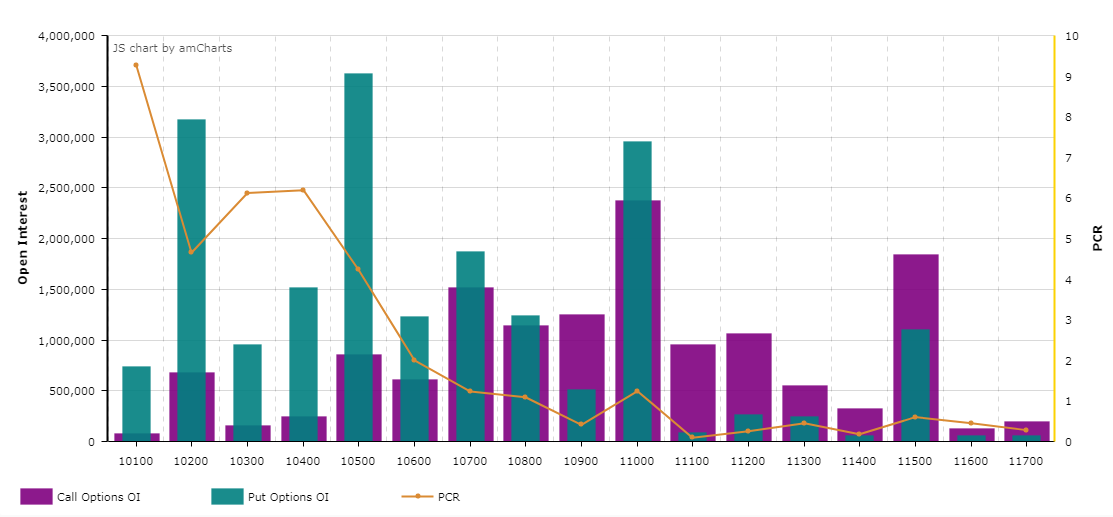

Also, another point I would like to add here is, the highest open interest is seen at two levels, 10800 and 11000. So I think minimum 11000 is possible.

was looking at NIFTY open interest data for dec and its looks like there is massive 29lac put written at 11k. never seen such aggressive position at this scale. someone is very bullish on nifty.

@timedimpulse : In the world of options, its the sellers who rule. So high OI in PUT is bullish as the big sellers believe market will go up and they will take the whole premium. And vice versa for huge OI in Calls

By 16th Nov itself 3/4 of the Complex Inv H&S pattern on daily had worked out. Trader seems to be timing the breakout point on 16th and fall till 22nd to avg out. Prices would have been 368 and 479. If equal qty was bought both times average would be 423. Though pattern target is 10500, even if this guy tries to square off at 11000, which seems real enough, then 11000PE would be around 184, which is 239 points. Huge cash can be made with volumes seen. I played safer by writing 10300PE on 21st to hold till expiry.

Now that we have come to an end of the month and hence crossed hump for CP redemption. Does any NBFC look interesting technically? Edel and Manappuram have stopped falling and seems to be forming base. What does technical say?