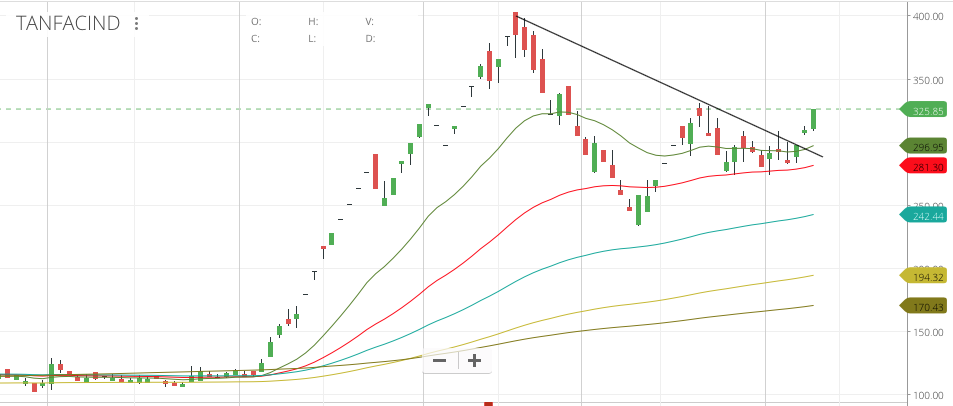

Mangalam Organics - Closed near all-time high but this will be strong resistance to break. Indecision might continue till results (14th Nov) which could be make or break. A quarter similar to the last is in the price. Hopefully this wont disappoint.

These two articles appeared on ET end of July. There were interviews to go along with it as well.

Indian Bank was trading at 370 when the articles came out.

To me at least the language of the articles screamed as an advertisement for the stock than anything else and so I made a mental note to revisit later. The stock made a brief spurt to trap people and then has gone only one way - down.

Avanti Feeds - Technically looks poised for a breakout which is why I was waiting for the results to pass before taking a call. Results have been bad and I think worse than what’s in the price. Maybe likely that the gap-up between 300-350 will get filled. Will hopefully get to buy this around 300.

Mangalam results should be strong. Diwali and ganpati season the sales are higher. Also the results will have a one time gain of 5cr cause of a settlement with creditor.

Disclosure not holding any of it now. Have traded strong moves in this counter right from 75 to 110. And then 190 to 370.

Looking to enter. Also have a look at its identical peer which will be posting results one day before managalam.

Kolte Patil both on monthly and weekly frames look very good. stochrsi on crossover on monthly seems pending. On a move above 250, can be a very interesting buy for previous peaks of 380-400 in 1 year or so (maybe less based on past surges from current levels).

Cosmo Films has also dilly dallied for long at current zone and indicators on monthly are aligning very well. Some strength above 270 can provide a good mid to longer term trade for prior highs of 420-60 in 1-1.5 years.

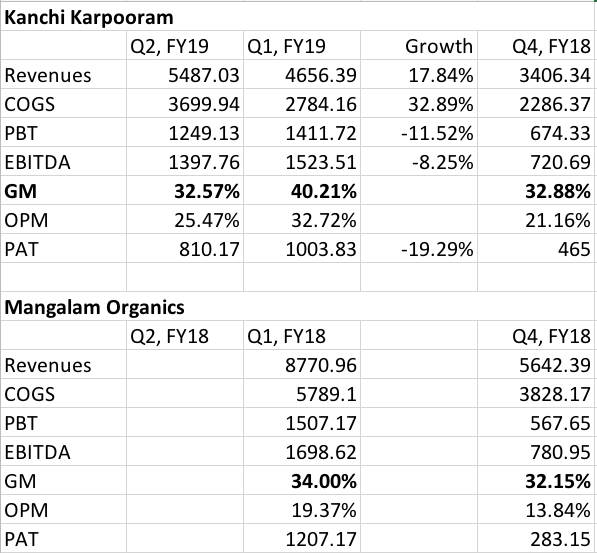

So Kanchi posted higher sales but 20% drop in profit QoQ.

I think what has happened is that RM costs have increased with increased selling price of camphor. However this was not reflected in Q1 because they must have old inventory from previous year at lower prices where they were able to sell at higher prices.

Now in Q2 the effect of higher RM can be seen with same sale price which has shrunk margins. I’m guessing managalam should have a similar trend.

Market was not expecting this and can react negatively.

@NamantS - Kanchi’s last quarter was an anomaly. See this. The Gross Margins for both companies were at 32% in Q4, FY18 but in Q1, FY19, Kanchi Karpooram had a way better Gross Margin than Mangalam Organics. Mangalam’s improved only by 185 bps while Kanchi Karpooram’s GM improved by 733 bps. This inflated Kanchi Karpooram’s OPM as well in Q1 while Mangalam Organics’ OPM improved only in-line with realisations for its products.

What has happened in Kanchi’s Q2 is GM reverting back to normal levels. I think Mangalam Organics will not have such a pronounced variation as they never had a pronounced GM gain in Q1, FY19 so QoQ Mangalam’s numbers tomorrow may not look as bad as Kanchi’s (YoY it should still be 2x at least). This is what my reading says but market is bound to have a knee-jerk reaction especially considering the needless rally today. I will make a decision after the numbers come out to see if I should book profits or hold on.

Yeah so this anomaly I think would have been cause of higher realizations on sale and lower costs of inventory which lead to margin expansion. In this quarter probably RM costs have gone up proportionately to selling prices so Gross margins have returned to normal. Right?

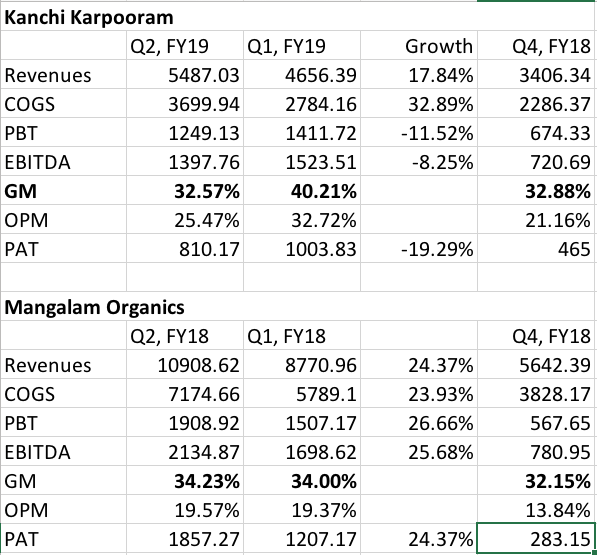

@NamantS - My theory has played out in Mangalam. GM is what caused the variance in Kanchi and the Market predictably threw a fit in Mangalam Organics as well today and thankfully I had the better sense to add. Results are very good QoQ and spectacular YoY.

Re Mangalam Organics Good results and the stock price falls - I seem to see this as a recurring theme in the stock market and am trying to understand it. Is this “normal”

That happens when everything is priced in. This is more common when there are a lot of short-term traders who book profits when their targets are met. Also, microcaps can be manipulated easily by a few traders. Prices don’t move up unless there is a big positive surprise as everything is discounted already. Also, worth considering is the VWAP (Weighted avg price) as the last few trades done on low volume can show the price as low.

In Mangalam’s case, market was pricing in the worst seeing Kanchi Karpooram’s results which is why it was in LC until the results. The results surprised the markets and there was high volatility as it went from -5% to +5%. I see more value in this scrip, so I have decided to hold on. I may not have, if the results were similar to Kanchi’s. Technically as well, It’s broken out above 500 after a long consolidation, so as long as it consolidates above this level, I think it should be fine.

Yes. Their DRT French deal can be the game changer. Somebody should contact the company and ask them when can we expect the deal to reflect in the books. Till I will wait for a correction or dip to get in.

Next 6-9moths look good for this. Currently it is trading at 9-10PE. Do you think we will have PE expansion going forward?

EPS growth plus PE expansion can best thing to happen to this stock.