yes, if i recall it right, it was 85% that he mentioned.

1 Like

True , Ashish Chauhan answered to the question to analysts who was saying are you going to give big dividend because of one time gain made on CDSL stock sale ?

Answer was we don’t want to raise the expectation of investors by giving high dividends, Rather we will try to consistently payout similar dividend ratio as we have been in past.

We always try to ask this questions why prices are going higher or going lower - Generally the answer is higher prices are the reason for higher and higher prices and lower prices are the reason for lower & lower prices.

Okay , with BSE - its still not trading at very attractive yield lets say 15% = Div + earning yield and its not going to grow at very high rate. so, it’s not very irrationally priced.

Even at 10% lower @ 750 … dividend yield is just close to 4-5% depending on cyclicality of profits.

@dd1474 whats your return expectation with the stock ?

3 Likes

I think it is good time to accumulate more as beginning October 1st (Around 2 months from now)BSE is going to start with Commodities Trading also trading hours are going to increase for couple of Derivative Products. Till the time we have people trading in & out of stocks day trading, swing trading, momentum trading, arbitrage etc…exchanges and brokers will continue to make money. The only downside i can visualise is during Bear Markets these companies will go for a toss…

Thats my 2 cents

In several analyses there are common references to the financialization story in India, low penetration and long runway. What I am struggling with is which business has the economic power to emerge as a true “lambi race ka ghoda” and which will get mired in the mud. I understand this is something done best in hindsight - if somebody has some models/ pointers to do this analysis - would much appreciate that.

I am reviewing these to decide where to bet on, what the opportunity costs are, and how to mitigate risks

- Insurance

- AMC

- Exchanges

- Depositories

- Other…?

I think, we can compare it with US economy where financialisation theme has played out. Eventually there will be 2-3 big players in all these individual area. But as they go through the journey, each one will have to face myraid of risk and corporate credibility and governance will ,make them stand out from the other.

Its a cyclical business in bull market they make > Rs 200 Cr of profits

and in bear nothing goes for toss they still make > Rs 150 Cr of profits.

They make whole lot of money from stable revenue stream.

So in short your view is wrong, As nothing will go for a toss and bear markets don’t last for ever . you have to see business from 10 -20 years prospective and how much Cash its going to generate over the market cycles.

Business or bonds or infact anything should be valued on the basis of how much cash they going to generate in years to come . Should not be valued on the basis of perception what going to happen in bear market.

BSE exists from 100 years many Bear markets came the business never went for a toss.

4 Likes

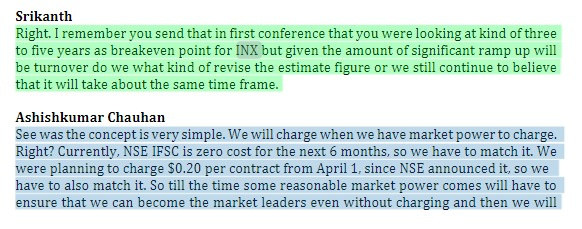

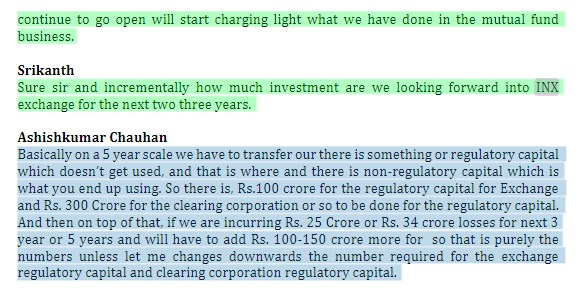

What are the company’s plans for monetizing the INX and mutual fund platform?

They’re currently doing avg daily premium turnover of $1.5-2m on INX. If we take 0.1%(not sure of this assumption) of this as revenue for BSE, they can generate around $500k in the first year. Considering the strong turnover growth they’ve shown, assuming the turnovers to grow at 50% CAGR for next 3-4 years, revenue from INX could grow to $2-3m or 15-20cr. Views invited

BSE Management indicated in Q3 FY18 concall about their plans to impose token charges (0.2 USD per contract) on INX. Though, in very next concall they informed they need to match NSE in terms of any such charges (NSE Gift City Exchange is free for first 6 months). Therefore, BSE had to change their plans. Here is a snippet from Q4FY18 concall.

Obviously, charges will be imposed at some point. In Q1Fy19, they managed to register ~28000 contracts on INX, so assuming ~14 INR/contract, it comes to 4 lac inr/qtr. Is nothing.They really need to build much more volumes or charge much higher to move the needle!

Where did you get the contracts info from? On the daily market turnover page on the site, it gives info on Number of Trades, Open Interest. Volume(Shares/ Contracts), Notional Turnover(US $) and Premium Turnover (US $).

The notional turnover and premium turnover have been consistently growing every month.

I am looking BSE as quasi debt investment of 5% yield with optional equity value. Would be happy to invest if price decline further as would match post tax fixed income return. I can hold as no opportunity cost on holding with free equity optionality

4 Likes

They talked about it in concall. Though 28000 is the average daily turnover…oversight… Stand corrected.

So, 3.5 cr rev per qtr at 0.2 usd per contract.

Okay. So it matches my number of 15cr/yr !

Considering if they show good growth in the coming years, as has been the case since INX’ inception, it could give decent growth boost to overall topline.

What would be the best way to value Stocks like BSE should we use DCF or DDM. What would be the fair value of BSE.

Anyone has historical DATA to see how market cycles affects BSE earning ? I want to see the numbers of previous bull market cycles 2002 - 2007.

Also, we need to calculate how bond portfolio (other income) of BSE going to get affected if interest rates move up, I feel it’s going be only M2M but still as they have no intention of cashing out their bond portfolio in future.

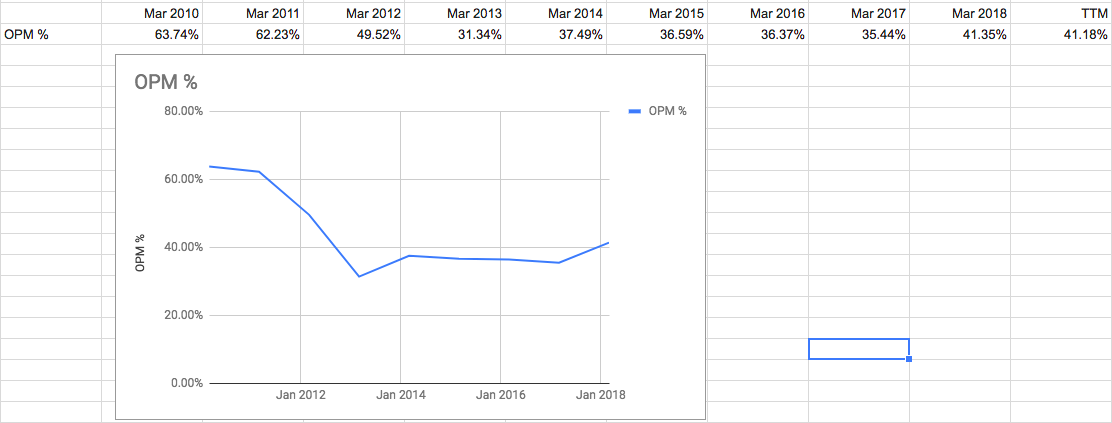

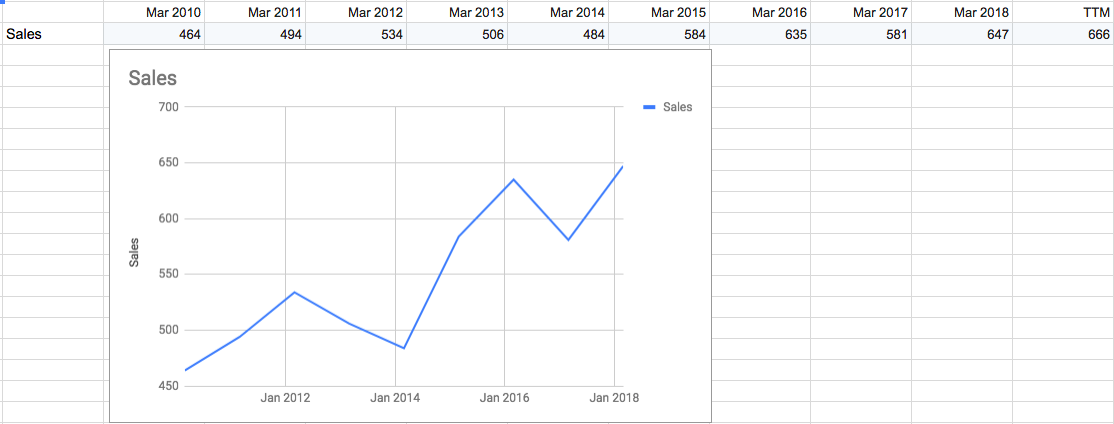

Although Revenue has gone up the Margins have declined from 63% to 40% … The revenue mix of BSE makes it very hard to estimate its future earnings.

Any idea why Margins have declined so much ?

1 Like

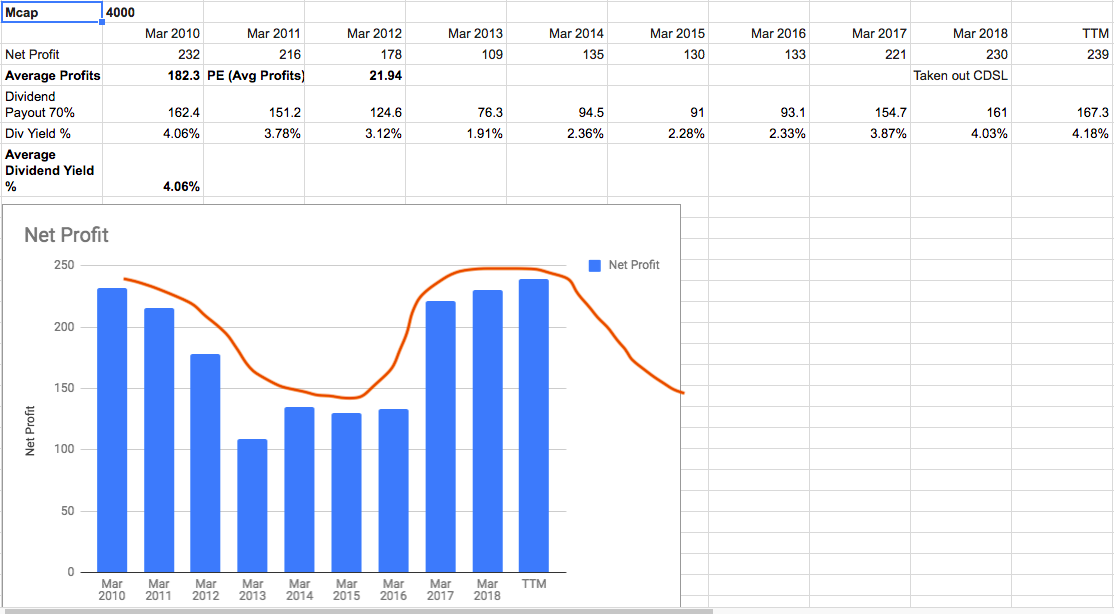

If we just take average profit over the cycle it will come around 160 - 180 Cr. Average PE = 22.

If hope dividend payout should remain 70 % then Average dividend yield going to be 3.5- 4%

As you can see below - In down cycles at current Mcap the dividend yield has fallen as low as 2% and at boom today dividend yield is 4.8%.

Considering all that looks like its trading fairly or rather expensive ( 3.5% div + 4.5% earning yield ) = 8% yield on an average.

Some of the questions i have -

Is it always going to be range bound between 120 Cr - 230 Cr or there will be some growth due to more flow towards equity market i.e, range will keep shifting upwards ? Is the incremental gain in the market completely going to NSE ? We need to see previous 2002 -2008 bull market data to be able to understand that .

Even if adjusting cycles BSE on an average grows 7% CAGR then its a great buy today, As yield goes to 15% risk free.

Is it okay to expect that ?

One sure thing is its ownership in CDSL should grow in value over time and hence the dividend from CDSL over long long time.

BSE STAR M.F platform should grow over time at moderate rate like at least 7% .

Currency trading , bond trading etc should grow over time.

The EBIX and INX nobody know if they going to click or not.

Overall i don’t see it screaming buy. Lets hope INX turns out to be good in coming years.

1 Like

i dont understand ur logic behind calculating total yield using earning yield. Is that the way stocks are valued using these yield parameters?

Also I think u totally missed one point - RISK. There is almost no risk at current price and u can assume it equivalent to bond investment but if 7% growth is realized, it will reward substantially.

I dont think adding dividend yield to earning yield makes sense. It’s like counting dividends twice as profit after tax already includes dividends. Dividends are below the line adjustment…

3 Likes

Correct , my bad.

Then only hope is with current valuations at what rate earnings going to grow ? if it’s not going to grow then at current valuations it just looks like very low yielding asset with lots of cash in balance sheet.

No one knows if at all this cash going to be returned to shareholders.

1 Like

The current dividend yield is 4% and the past dividend yields were also good if not spectacular. With huge cash holding, the trend will continue and not to forget the recent buyback which is EPS accretive. BSE neither have a major promoter nor have a major capex.

So what makes u so skeptical about BSE becoming non-investor friendly in future ? And does anyone guarantee even for bonds in case of a financial turmoil ? If no one knows, it applies for any stock and in that case, on what basis one will invest?