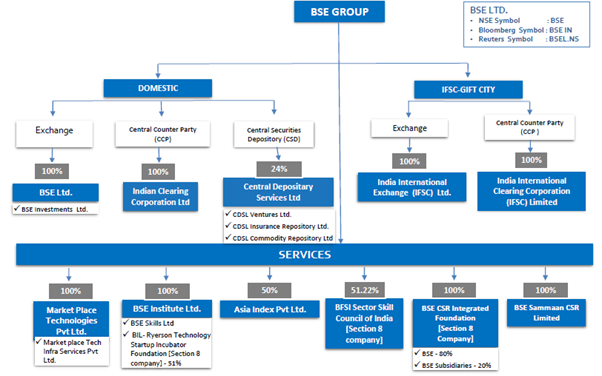

Established in 1875, BSE Ltd is the oldest stock exchange in Asia and operates the BSE exchange platform (formerly Bombay Stock Exchange). As of September 2017, the BSE is the world’s largest exchange by number of listed companies (5000 companies), and India’s largest and the world’s 9th largest exchange by market capitalization of listed companies at USD 2.1 trillion. With a trading speed of 6 micro seconds it is the fastest stock exchange in the world as established by the company.

Key Business Drivers:

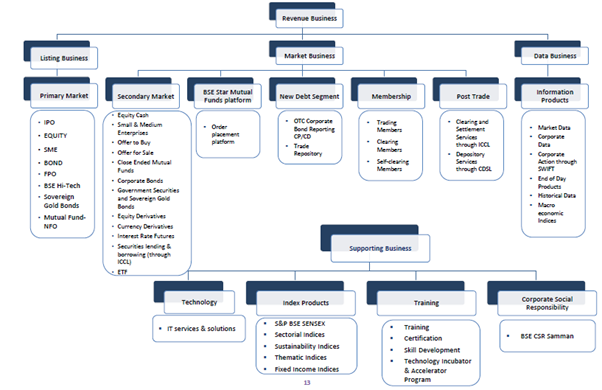

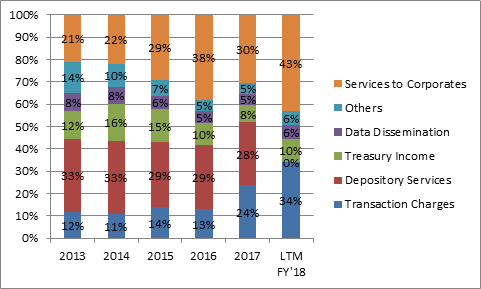

BSE through its standalone and subsidiaries derives its revenues from the following sources:

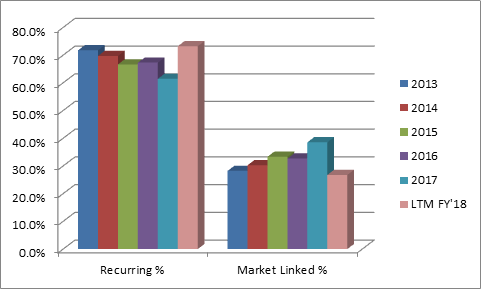

a) Market-Linked Revenue (~27% of FY17 Income)

- Transaction Charges, which relates to the income of purchase and sale of listed securities.

- Treasury Income on Clearing and Settlement Funds, Linked to interest rates and market activity since that would lead to more margin being deposited by members.

-

Income from Depository Services, Includes recurring annual charges as well as custodian services, which are to an extent linked to market activity (~this revenue is now shown as part of associate income due to decline in shareholding in CDSL to ~24%).

b) Recurring Revenues (~73% of Income) - Securities Services primarily consists of charges recovered from members for network connectivity.

- Listing Charges, derives listing income that is not impacted by market activity and Dependent on number of listed entities and hence is a recurring revenue stream. Potential for increase if amount charged is increased.

- Data Dissemination Fees, which consists of the sale and licensing of information products, Providing IT services and solutions, licensing index products such as the S&P BSE SENSEX and Providing financial and capital markets training through BSE Institute Ltd.

- Income From Investments and Deposits and rental income, Linked to investment yields.

Investment thesis:

a) With NSE Listing still far away (and also NSE being plagued with its own set of problems), BSE benefits from being the only listed stock exchange in India.

b) Price hikes to result in improvement in transaction charges: Considering that ~2500 stocks are listed exclusively on BSE, in January 2016 the exchange increased transaction charges in this segment from Rs 27.5/mn to Rs 1000/mn which led to steep increase of 122.7% in transaction charges revenue. Besides this in order to attract bulk deals from NSE it changed pricing structure in non-exclusive segment from ad-valorem basis (Rs 27.5/mn) to a flat fee structure that was Rs 0.3-1 per trade w.e.f April 3, 2017, which was increased to Rs 0.5-1.5 per trade w.e.f August 1, 2017.

c) SME Platform – Next Engine of Growth BSE launched SME platform in December 2012 to facilitate capital raising by SMEs and startup companies and provide easy exit options for angel investors, VC, PEs etc. At present the current tariff is Rs 27.5/mn turnover for trading on SME platform. Besides, this platform also contributes to listing revenues. At present 158 companies are listed on SME index which have a total market capitalization of Rs 105.7bn.

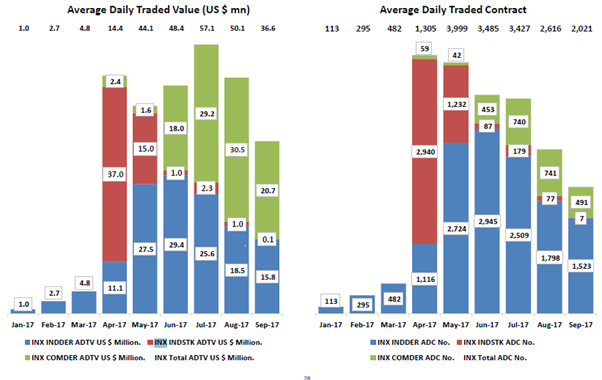

d) Recently commenced trading operations in INX to provide improvement in valuations: With an aim to attract derivative volumes from much bigger global markets and exchanges, BSE launched India’s first international exchange (INX) in GIFT city, Gujarat on January 16, 2017, through its wholly owned subsidiaries – India International Exchange (IFSC) Ltd and India International Clearing Corporation (IFSC) Ltd.

Following are key competitive advantages vis-à-vis NSE or other domestic/global exchanges –

(1) All asset classes i.e index/stock/commodity/currency derivatives will be available on a single platform.

(2) Tax free status for first 5 years i.e no STT, CTT, long term capital gain tax and income tax will keep transaction costs lower.

(3) 22 hours of trading.

(4) Trading speed of 4 microseconds.

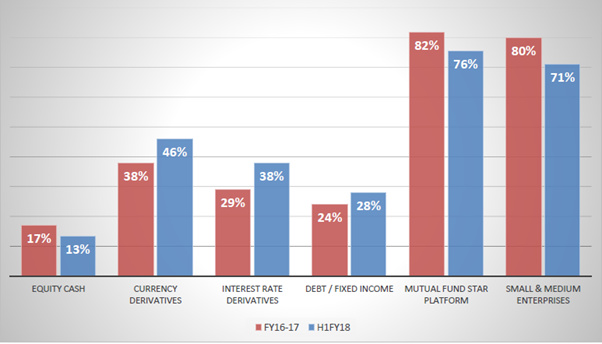

INX’s turnover has improved from $ 11mn in January 2017 to $3422mn in Sep 2017. Index, stock and commodity futures constitute ~44%/70%, 4%/5% and 50%/25% in value/volume terms respectively. Within commodities, gold futures contribute maximum. At present 5000 contracts are traded daily on an average and it will reach breakeven on reaching 50000 contracts per day. BSE is expected to monetize this platform in FY19E. BSE has set aside Rs 4bn for capital infusion in this venture over a period of 3 years, of which Rs 3bn is for international Clearing Corporation. Out of this, Rs1.15bn investment has already been made.

e) Improving Return Ratios:

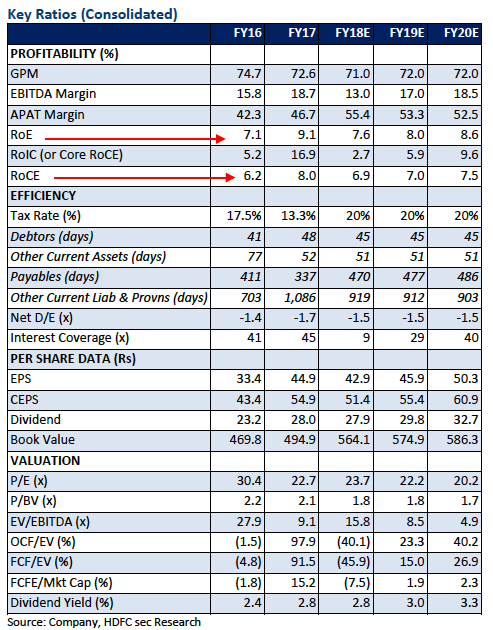

Due to recent regulatory changes, As per sec. 33 of SECC regulations 2012, earlier BSE had to contribute 25% of its annual profits to Settlement Guarantee Fund (SGF) of ICCL which resulted in lower Net income. In Aug-16, SEBI amended Regulation 33 of SECC Regulations, 2012 to remove the provision that required a recognized stock exchange to transfer 25% of its profits to a SGF. As a result in FY17 financial statements, only the contribution of Rs 207.9mn that was made upto August 2016 and was deducted from profits which resulted in PBT growth of 43.7% YoY to Rs 3.1bn. Besides this earlier in FY16, BSE also discontinued Liquidity Enhancement Incentive Program Scheme (LEIPS) w.e.f April 1, 2016 which was deducted from its profits earlier. As a result of increased business, margins, recent regulatory changes and discontinuation of LEIPS, BSE’s RoAE (Return on Average Equity) improved from 5.4% in FY16 to 8.5% in FY17.

f) Improving Demography and Under penetration of equity as an Investment:

• The long term outlook for India remains strong and as per multiple international agencies including USDA, IMF and World Bank, India is expected to emerge as the 3rd largest economy by 2030 with a GDP of $ 7 trillion.

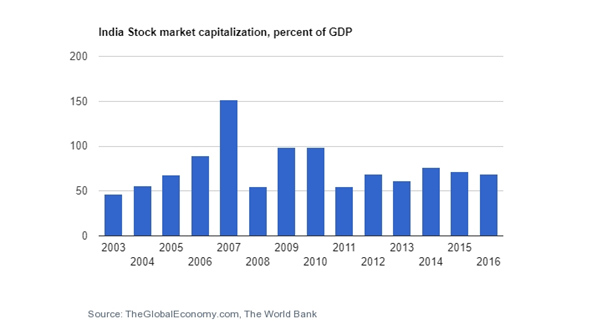

• As compared to world and BRICS average Market Capitalization to GDP ratio of 99% and 88% respectively, India’s ratio is lower at ~73%, which signifies the potential for growth ahead.

• Unlike globally where free float is as high as 89% in Brazil and 90% in NASDAQ, in India its lower at 54%. So as promoters dilute some stake, it will increase free float thus leading to depth in markets and increased business opportunities for stock exchanges and other market participants.

• Indians comprise 17% of the global population and yet only 3% of the population is invested into capital markets.

• Equity as a percentage of total savings (financial + physical) is only at 5% as against 14% in China, 15% in Brazil, 20% in Indonesia and 42% in USA.

• 60% of India’s population is in working age category.

• Post demonetization the cash that has entered into formal system, is being invested in markets especially in mutual funds and ULIP products. Besides EPFO increasing equity % of its investments is also bound to improve transaction volumes.

Arguments against Investment:

a) Loss of Market Share to NSE which is a key competitor and BSE always playing second fiddle in equity cash segments:

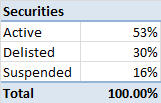

b) Risk of non-compliance by listed corporates leading to suspension/delisting of the stock. This impacts annual listing fees of stock exchanges. On BSE a stock gets suspended / delisted after 2 quarter / 7 years of non-compliance.

c) Regulatory risk due to non-compliance with legal/regulatory obligations or change in regulations due to changing macro / sector specific environment.

d) Credit/liquidity/settlement/collateral risk in clearing and settlement business.

Conclusion:

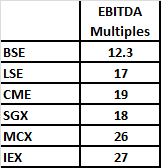

With cash per share of nearly ~Rs.700 (includes restricted cash ~25%), there is adequate margin of safety. In addition, BSE is trading at lower multiples with respect to other listed peers:

Views Invited…

Disclosure: Invested.