ICICI MF has heavily invested in QIP. I sincerely hope they have done a significant due diligence of the same given S Naren at the help of affairs

1 Like

Few points that i noticed while reading the annual report -

How are margins going to get effected with rising crude prices? Crude being major RM for dyestuff manufacturing. Has anyone analyzed this?

Last year, volume for both dyestuff and intermediates have been same as that of 2015-16. So, improved topline/bottomline was due to improved realizations and supply shortage. From next year onwards, growth will be volume led in my opinion.

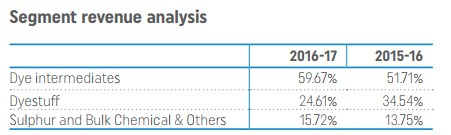

From the annual report -

Dyes intermediates

The Company produces upto about 25 variants of dye intermediates in this segment. The key products of this segment include Vinyl Sulphone Ester, H Acid, F C Acid, DASA, Gama Acid and 6 Nitro. The production for FY 17 was 23100 MT as compared to 23004 MT of the previous year with a change of 0.41%. The capacity utilization was 77% as against the capacity utilization of 77% of FY16.

Dyestuff

The Company produces up to about 150 variants of dyestuff products in this segment. The key products in the segment include Acid Black 210, Reactive Black BL/GR, Reactive Black B, Reactive Black 5 and Acid Black 194. The production for FY17 was 12503 MT as compared to 12764 MT in the previous year with a change of -2.05%. The capacity utilization was 74% as against the capacity utilization of 75% in FY16.

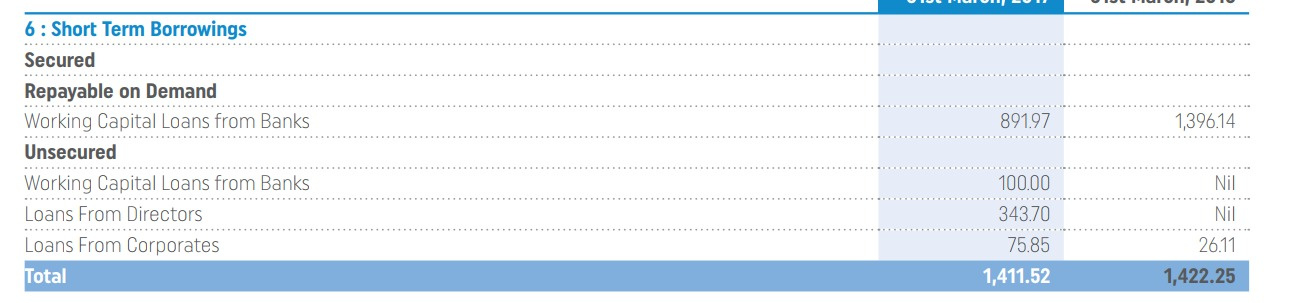

Company has taken working capital loan ~ 34 cr from promoters. Interest rate not mentioned.

3 Likes

@Mridul

Please refer to Page 110 of annual report FY17 for Bodal which provide information about related parties. Since there is no payment of interest being shown, we can assume that it was interest free. Further, amount of involved are not very material in my opinion. Total unsecured laon received from promoteras at end of year is around Rs 3.42 Cr as per disclousre.

On Crude price, while the raw material is linked to crude prices, it is industrywise factory. Given the present favouable demand supply situation in global market, I assume the company would be able to manage the Contribution margin in absolute term (Rs/kg). However, due to increase in crude price, sales realisation is expected to increase as compared with FY17. So with constant Contribution margin per tonne with higher Sales realisation per tonne, Contribution/EBITDA as a per cent of sales may be lower than FY17.

Hope this asnwer your queries.

2 Likes

Thanks for answering. So basically, crude will result in increased topline, some contraction in margins, and flattish bottomline? Most of the growth would be volume led starting q4 unless some drastic price changes.

1 Like

Let us say FY17 Sales price was Rs 100 per kg and Input cost was Rs 50 per kg+ Other cost and overhead of Rs 30 per kg, So EBITDA was Rs 20/kg or 20%.

Assume 10% increase in cost, which is passed on by hike in sale price in FY18.

So revised Sale price Rs 105/kg, Input cost Rs 55/kg+ Other cost Rs 30/Kg. Hence, EBITDA is still Rs 20/kg, but EBITDA margin is now 20/105 i.e. 19%.

So the point I am making is that abolsure EBITDA is stable but EBITDA margin decline. The increase in sale price would be function of global demand supply situation which is currently appears to be favourable due to supply issue from China.

6 Likes

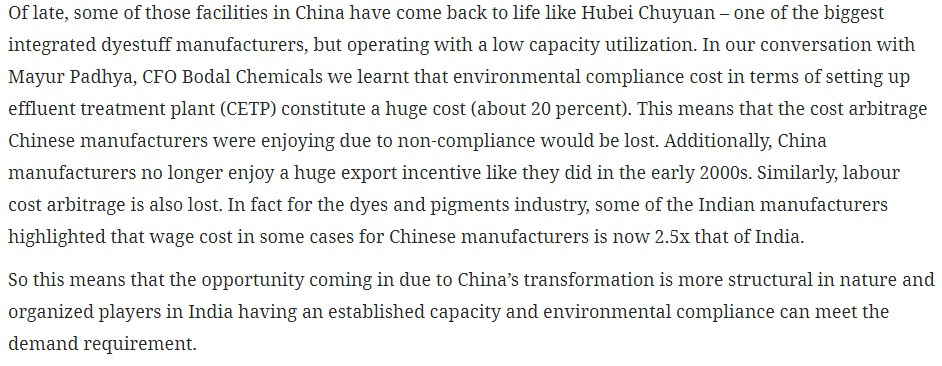

This article reflects how important it is to develop an integrated business model in order to survive RM price fluctuations and industry headwinds.

I think larger players like pushkar and bodal are at a big advantage here due to captive dye intermediates capacities. This gives better pricing power. Punit Makharia (Pushkar MD) has repeated said in concalls that chem prices is least of his worries (they will fluctuate as per demand supply). What he is focussed on is develpoing a good business model which can give the business an edge over its competitors. A sustainable model which can face industry headwinds robustly.

Diversifying higher up the value chain into dyestuffs (bodal and pushkar) and textile chemicals (pushkar) is helping these companies sustain ebitda margins around 17-18%.

3 Likes

Board Meeting on 13th Dec, 2017:

http://www.bseindia.com/xml-data/corpfiling/AttachHis/47e3aebd-1df0-43cb-b9fa-1cc4f4d74283.pdf

Management’s comment on result -

“During Q2 & H1FY2018, we have had to navigate our business through implementation of GST, particularly affecting the textiles sector – a major client. We have also had moderation of product prices on YoY basis. Lastly, we have carried significant upfront cost from our integration & expansion projects. We have, however, continued to focus on higher profitability which is reflected in Q2 & H1 of the year. We are also on course on implementation of our three new projects of dyestuff expansion, co-generation power plant & thionyl chloride, which will provide new avenues for growth of revenue and profitability in the coming future.”

I am curious why revenue has slumped by ~29%. Agreed GST could have impacted their textile clientele (domestic), but exports are down quite a bit as well. PBT margins are slightly better yoy so this is not about margins. PAT is down because revenue is down. They said prices have reduced this qtr for certain chemicals yoy, so revenue has taken a hit? Or this is about volumes?

My hunch is they may have more competition hence decline in prices. However this is a industry consumable product and as the secular demand across economies grows, demand and pricing will both improve.

This is a strong management company and has taken major investment decisions in recent past. It had an attractive valuation even before yesterday’s fall. Now its perhaps a more compelling buy, subject to your own research.

(Discl: Invested)

12000 mtpa additional dyestuff capacity will bring in 220 cr of extra revenue on full utilisation. additional vinyl sulphone capacity of 4200 mtpa will bring close to 50-75 cr revenue. then 36000 mtpa thionyl chloride (35% captive usage) will add to revenues, along with labsa and trion chemical plant.

Coming on to operating margins - will improve with dyestuff contribution increasing, cogen plant reducing power expenses, and thionyl chloride captive usage. all in all one can expect 20% margins in 2018-19.

Assumption - 1. chem prices remaining stable!

2. Many players are doing capex. I am not sure if everything can be absorbed.

2 Likes

Snippet from an article on Dyechem industry. Although the article is 6 month old, still want to highlight the point emphasized. After GST supply pause, organised dyes and pigments players to emerge stronger

One other reason for this being a structural change is that buyers want to diversify their purchase.

@dd1474 bhai - Have you come across any industry report covering supply/demand scenario in India? The sector is growing well and the purchase is shifting from China to India, but many companies are doing large capex. For instance, Bodal is coming up with 12k MTPA dyestuff capacity in Mar 18. Pushkar came up with 3k MTPA capacity in Dec 17. Kiri is undergoing capex for Dispersive dyes (Bodal is not present in this segment) which will help doubling Kiri’s revenues in 3 years. As per mgmts, there is enough demand. For instance Bodal mgmt said they will be able to utilize 50% of the new capacity in first qtr itself. Shree Pushkar management was fairly confident of increasing utilization levels for the capex. One important thing to notice is that Bodal’s dyestuff capex is geared towards attaining manufacturing capacities for dyestuff with better margins.

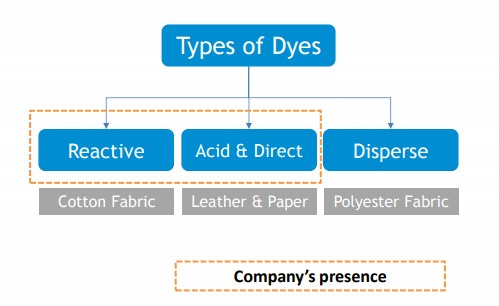

Three things worth mentioning in this supply demand dynamics - 1. Even if price deteriorates, it would be temporary, as demand is constantly on the rise. 2. Price deterioration will crumble already crumbling unorganized and smaller players, who are increasingly finding it difficult to compete with larger players post GST implementation and RM price increase. 3. There are different dyestuff variants (Bodal manufactures 150 variants) and companies’ capex are geared towards attaining capacities in those variants where it doesn’t have presence or doesn’t have significant capacities. As i pointed above, Kiri is going for Dispersive dyestuff, where Bodal is not even present.

1 Like

Bodal Chemicals has uploaded all the Analyst Concall transcripts on its website. Those who are interested can get the Q2 results concall from there now. I was following with the company for this.

I hold good amount of bodal chemicals in my portfolio.The prospects of the comapny looks great considering the managements ability in the past to successfully get out from cdr.However recently comany announced QIP.As per business standard report,qip was raised at a price less than the floor price.

what could be the impact of qip on my returns,further does it in anyway tells us about managements character,since the expansion plans were supposed to be funded by internal accruals and some debt earlier.

comments invited

Disclosure-Invested in bodal chemicals.

bodal chemicals has informed bse regarding grant of options at rs 50.How do you analyse the impact of issue of options?

Any update from the conference call on Feb 7th to discuss Q3 results? Promoter holding has gone down to 55% and I am not sure what to make of the results. Seems steady, but no clear highlights. Why are exports significantly down this year? Any inputs from those who are tracking/own this?

My notes from 3q18 concall

Dye stuff - yoy revenue increased by 28% (volume increased by 38%, realizations decreased)

Though exports decreased, margins were maintained as domestic realizations were at par

dye stuff - 3956 mt vs 2863 mt in 3q17 (38%) - 230-240/kg

intermediate - 5917 mt vs 4720 mt in 3q17 (25%)

Base chemicals - 37758 mt vs 40284 mt in 3q17 (-6%)

LABSA - 517 mt vs 1568 mt in 3q17 (-67%)

Promoter holding reduced by 6% this quarter

SPS - 46 cr for 9months

VS capex to take a few more months to be commissioned - by 2q19. Due to safety guidelines changed by Reliance

Trion Chemicals problems sorted out - 25-30% utilization by 4q18. Stabilization by 1q19

9 month loss is 5.5 cr in Trion… to go up to 7 cr for the year. To be profitable next year. Bodal share will be lower

SPS also posted a loss of 2.5 cr?. Stake is about 70%

Long term operating margins at 15-16%. (Being able to get 18-20% for a while)

Targeting a 100 acre land in Dahej - to cost 90-100 cr

15+ projects are being considered to created an integrated project. Game plan to be revealed shortly.

This will be unrelated to dyestuff and intermediate as those are already manufactured in Baroda

Dahej to be commissioned in 4-5 years

Growth expected next year due to Trion, Dyestuff, VS and co-generation power plant

One of the larger competitions in China had been shut down for 6 months and then restarted with only 50-60% utilization as opposed to 85% earlier. From april 2019, extra tax will be charged to companies that pollute air/water in China.

60% revenues exposed to textiles

Aim to grow in the domestic market. Should get better after GST implementation eases.

Better integrated than a couple of older competitors who focus only on dyestuff

Competitions’ brand is better but Bodal is picking up fast

Biggest competitor produces about 5000 mt per month. Bodal is poised to produce 2500 mt with current capex plan

Aims to be the biggest in 5 years (cross 5000 mt per month)

Thionile Chloride market is about 15000 mt, Bodal will make 3000 mt. Major market is near Surat so they have a location advantage. Low priced item. Recently price increased from 14 to 18 rupees.

Major application is agrochemicals and VS… both sectors are doing well in last 5 years. Hence demand increasing. But no new capacity coming up.

Very hazardous product and low value which discourages import/export

Intermediate is mostly direct sales. Dyestuff is sold to traders, dealers and also directly. (even for export)

Capex - 130 cr so far, 80-100 cr for the land whenever bought, 60 cr next year

All capex from internal accruals going forward

Dyestuff companies in far east countries grew dramatically despite having no intermediate production

This is because there was tremendous competition between India and China and so they got their RM very cheap

After crackdown in China, supply in intermediate has become tight. Hence these companies are losing their intl market share

After a few years, these companies will become unviable and will be taken over by Indian and chinese companies

Hence, potential of export of dyestuff to continue to grow

5 Likes

Thank you for the update, ‘barasia’. I don’t quite understand why exports are down given the restrictions in China. Also, for all the stated ambitions, it looks like they aren’t really tracking to original growth plans and seem to be hoping rather than executing. That’s disappointing. The only positive seems to be that MFs have increased their shareholding - so maybe there’s reason to believe exports and overall growth will pick up.

Why promoter holding has decreased so significantly, what was the reason for sudden decrease, any clue?

Nothing new in the article. Assumption is that the growth will be volume led rather than margin led for next year as well. Crude rising supports this stmt as well. Captive consumption may result in somewhat better margins. So, this in tandem may normalize things.

Delay in SPS VS capacity due to external factors, failure to make TRION profitable, failure to increase capacity utilization of liquid dyestuff, along with lower price realization is weighing on the stock.

I am hopeful that SPS problems will be resolved in next few qtrs, liquid dyestuff will contribute more this year as and when paper companies approve the product.

This is the reply I received from the CFO when I asked him about promoter holding decreasing

"The reduction in the promoters holding is due to the selling of some shares by 2 promoters group persons. They are of professional category. Whereas the Suresh Patel and family, who are the main promoters, has actually increased the holding in last 2 years.

Suresh Patel and family may consider to increase the holding further."

Also, there was no sale of promoter shares in 3q18. I believe that the stake has reduced due to dilution via QIP to ICICI mutual fund.

3 Likes