That person doesn’t have any managerial or key positions. I think it shouldn’t matter much.

Containing Effluents bodes well for Bodal, who has gained an edge ove local and chinese players,

4 Likes

Sir ji - As per the FY16 AR, he is President Tech & Production.

I think he is one of the key personnel. Plus he has sold almost all of his holding.

my 2 cents.

Regards,

Django

Disc: Holding from 138-139 level.

My bad! thanks for the info though

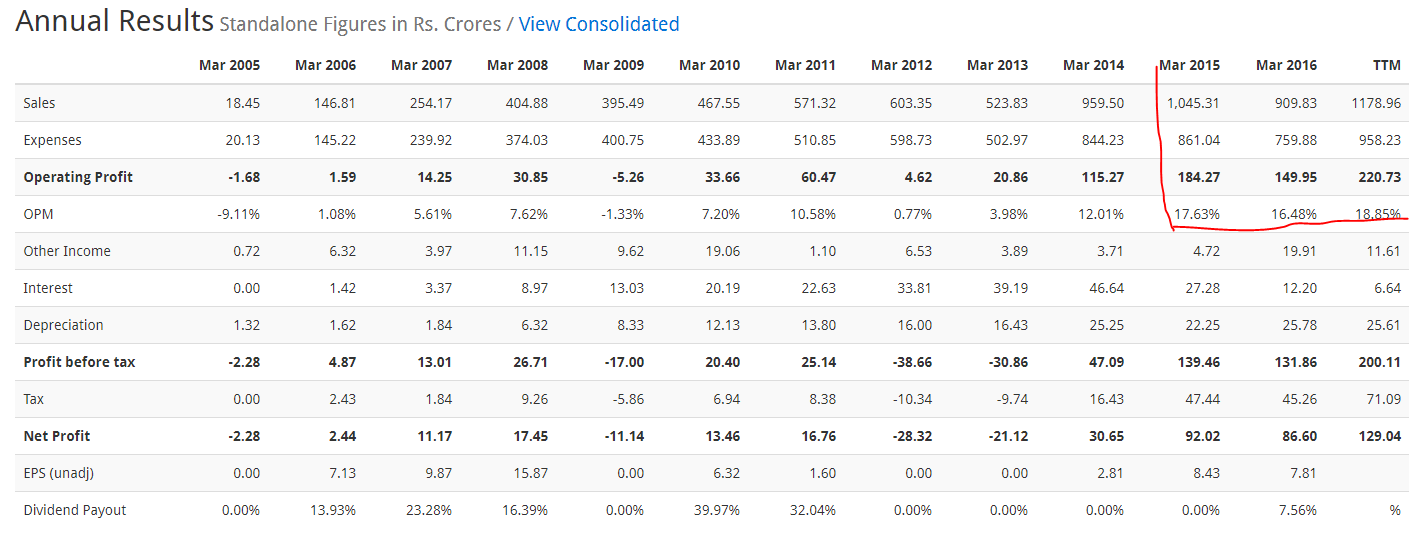

Want to understand the impact of China chemical plant shutdown on margins. Bodal EBITA was 17.63%, 16.48% and 18.85% in FY15, FY16 & FY17.

China chemical factories were closed somewhere in FY16. So for Bodal, EBITA was 17.6% before China event.

Is it safe to assume that Bodal should maintain atleast 16% margins going forward even with China plant resuming production? I see lot of fluctuation in margin and want to make sure what can be expected going forward.

Please share your thoughts.

Please refer to the investor presentation on Bodal chemicals which gives you a fair idea about the prospects of this company

http://www.bseindia.com/xml-data/corpfiling/AttachHis/551f41ab-8e17-4e6b-829b-4e81375b5c09.pdf

1 Like

Bodal Chemicals earnings release -

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a773facb-3707-4177-8847-94d4c1b0b7b3.pdf

New presentation -

http://www.bseindia.com/xml-data/corpfiling/AttachLive/45d80be0-41d8-4a97-8980-e33ee7c55238.pdf

(outlook updated - see presentation slide 17 onwards)

Conference call replay can be accessed on researchbytes.

Bodal Q1 Concall- My take - 2017-18 likely to be muted as host of Capex stuff are happening and Org in a consolidation mode including in the new acquired UP one where there is no profit at all and they are setting up VS plant now. Good results are expected to flow early next year onwards

We need to be patient this year

2 Likes

Why are sales flat/down YOY and QOQ ? The capacity expansion etc should not have impact on sales isn’t it as it is still not 100% capacity utilization. Is because of less demand or china companies getting traction back ?

As per mgmt concal,there are below things affected sales

- Lower price realization

- Gst restocking

- There was renovation work happened in a lake behind unit-7 . so pollution control board requested to reduce the production for 15 days from that plant. Now that unit started full production

All 3 forced reduced top line.

Regards,

Sathish

6 Likes

Why is Bodal raising Rs. 225 Cr? This is substantial amount (~12% of market cap)

Such fund raising should be viewed negatively IMHO.

Any breakup of requirement given?

ICICI Pru AMC taking around addtional 2% of stake In Bodal, taking total holding to 6%.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/11899FA7_72E0_43B8_81D1_E8DD320FD45C_102917.pdf

5 Likes

Any idea about this ? What made them go for funding ?

Raising QIP is something I also do not like specially when the management indicate in conference call that they would be able to fund the capex with internal accrual/debt. Need to see utilisation of funds to evaluate my investment.

Discl: Holding and not recommeding any investment. Partially booked profit in last month in 5% of position.

QIP is done, raised Rs225 crs

I have been studying Bodal Chemicals since last 3/4 quarters and have attended their conference calls. Although the business is doing well, I have observed that the management says one thing and does another thing. Two recent examples.

- They said capacity expansion will take place with internal accrual till as recently as Q1FY18 con call; now raised equity via QIP

- They said in Q4 con call that their topline will grow by 20% in FY18; with flattish Q1FY18 they said entire year will be flat.

I read their previous annual reports and compared what they said to what actually happened and I noticed many such contradictions.

This might mean one of the following:

- Management lacks ability to confidently predict business environment even in near future.

- Business is unpredictable and no player has any control.

- Management makes quick decisions without worrying too much about what they have recently guided.

Such contradictions make financial forecasting difficult for this company.

Disclosure: Invested 8% of PF @ 130.

2 Likes

While I agree with your observation, I find Bodal management being one of few which paid Rs 100 Cr debt during one quarter when exepctional price hike in end product assisted the company performance and came out of CDR. Further, I generally look at broad trends and correct strategic actions from the management rather then perfect future forecast. It would be very difficult,and most probably a fraud, when future predicted by the management exactly turn out correctly time and again.

Having said that, I completely agree with your concern about recent QIP.

4 Likes

Management had spoken about a host of projects totaling Rs.342 crores in their Q1 presentation. Assuming cash in hand of around Rs.50 crores currently and annual cash generation of around Rs.100 crore, raising Rs.225 crores more to fill the gap seems natural. In the past, capex has never exceeded Rs.60 crore in a year. By that measure, the company seems to be going for a quantum leap now. Besides what has been stated in the QIP issue, a greenfield project at Dahej is also on the cards. Company is also looking for inorganic opportunities, they have said. Raising money when money is cheap is not necessarily a negative, provided it is used judiciously. Only time will tell.

3 Likes