I agree - I think there’s something else going on here. I wonder if the couple of MFs (Reliance, ICICI) may be reducing their holdings - will be interesting to see their holdings at the end of this quarter. Value Research has this check called “Can creative accounting be detected through X’s financial numbers”? They use something called the Modified C-Score (https://www.valueresearchonline.com/story/h2_storyView.asp?str=29406). For Bodal, that’s a high score, a Modified C-score of 7. That’s an indicator of a ‘fail’ on 7 out of 9 checks, and a higher score indicating a higher probability of financial manipulations.

1 Like

SEBI ICDR (Chapter VII is on pricing) mandates the formula for pricing warrants. So, promoters can’t simply put any price ! Ofcourse, they issue warrants to themselves when the markets are weak - if the intentions of the promoters are right, then this is a good signal. But, the intentions is what is questionable - sintex plastics also issued warrants and the price has falled to 0.1 x of warrant issue price !

1 Like

Broader market is exceptionally weak. All dye chemical manufacturers Bhageria,Kiri,Bodal,Shree Pushkar are trading at high single digit at trailling PE band of 7 to 9.

Bodal Chemicals AR Key Points!

https://drive.google.com/open?id=1LhA6SUPu4PGGf4vsahAnPHxx-lzjux4j

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

1 Like

Bodal Chemicals Q2 Results!

https://drive.google.com/open?id=1ed_VQIZkibH4W3HyN-N7cjZhzlKhXVJ3

(Disclaimer: Not an Investment/Trading Recommendation)

All dye chemical stocks are moving up significantly with good volumes. Anyone has any idea if the prices have started increasing? Or any news related to China?

https://www.cnbctv18.com/market/stocks/market-expert-sp-tulsian-bullish-on-chemical-space-bearish-on-2-aviation-stocks-4962071.htm - Updates from SP Tulsian

1 Like

May be this?

Slowly the non compliant producers will face the heat and cost of compliance will make kosher producers on advantage footing.

1 Like

Thanks. CNBC interview of Bodal also mentioned this. More importantly they mentioned that there has been demand pickup in the last 20-25 days.

Resharing this 2017 article - Hubei Chuyuan was one of the main sufferers of China’s environmental strictness around 2016 due to which many chemical companies in India gained a lot - Bodal gained approx. 3X within a year

Coronavirus hit Wuhan is the capital of Hubei. Overall Hubei province seems to be impacted as well with much of it under lockdown.

While the impact may not be as much as 2015-16, there still would be some opportunity. We can study companies such as Bodal, Bhageria, Kiri, Navin Fluorine, Meghmani etc. to screen ideas and shortlist the good ones to be prepared for a similar opportunity. We may leave out some of the companies having corporate governance issues such as Meghmani but still we should have many to pick from.

Views/Counterviews?

One question . Are Indian companies you named here are all fully integrated producer of Dye and Dye Chemical. No dependence on procuring raw material from China?

Bodal Chemicals Q3 Results!

Q3 FY20 IP:

As per Standalone Financials:

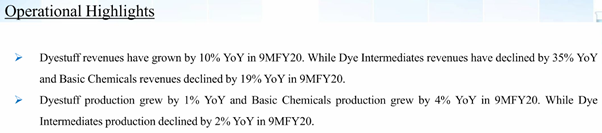

• Total production for Q3FY20 improved by 11 % to 52,084 MT Yo Y. During the quarter, Dyestuff production improved by 11 % Yo Y mainly due to increase in capacities and Basic Chemicals production improved by 13 % Yo Y due to addition of Thionyl Chloride plant. Total production during 9MFY20 improved by 3% YoY to 145,229 MT.

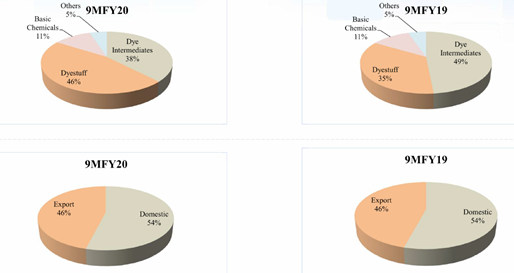

• Dyestuff revenues have increased by 10% YoY in 9MFY20 mainly due to capacity addition and higher utilization. This is inline with our strategy of higher integration and moving towards a global Dyestuff player.

• Finance cost in Q3FY20 was high Yo Y mainly due to increase in working capital limits utilization. While it has decreased by 12% QoQ.

• Total exports for Q3FY20 stood at Rs 1,306mn and its share in total revenues stood at 44%. The company continues to further enhance presence in different geographies across the globe.

• The board has approved acquisition of remaining stake in Trion Chemicals (Trion) and it will be 100% subsidiary of Bodal Chemicals. We were facing several challenges to run the plant earlier due to partnership. Now, we are confident to start and run the operations smoothly from April-2020 at Trion. We are expanding the marketing presence of the Trion’s products in the US markets which should yield positive results.

• Subsidiaries performance: • SPS posted revenues of Rs 288mn with EBITDA of Rs 7mn in Q3FY20. • Trion plant was not operational during Q3FY20 due to safety related changes in the plant. It posted loss of Rs 39mn in Q3FY20

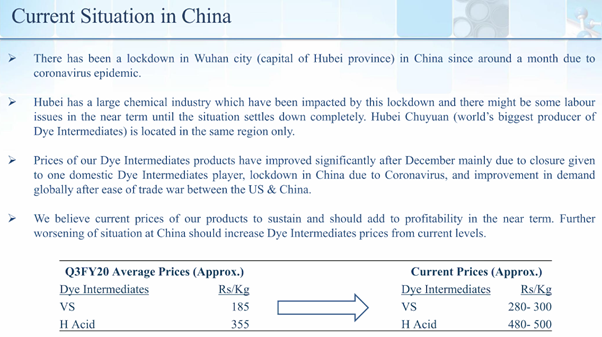

Yes. See, it is now almost more than a month. They are closed earlier because of their vacation and they could not restart after the vacation. We do have our subsidiary company over there, our employees, so we try to contact them, and they say they are at home only. There is a total kind of lockdown and nobody is moving out, at the same time the biggest producer at the world level that is Hubei’s Wuhan that is also located in this province and they are also closed. So, people are in fear very much, and according to them, it does not seem that in near future they can restart and we also come to know from several news that is coming up and some news clearly claim that whatever figure officially released are very much less than what actually is happening over there. So, it is very clear that within a month or 2 it is not possible for them to restart even if they come up for any solution within 10, 15 days.

Q3 FY20 CC:

Prices of our dye intermediate products have improved significantly after December due to these events along with closure given to one of the domestic dye intermediate player. Currently, the prices of Vinyl Sulphone is around in the range of Rs.280 to Rs.300 per kg, which was around Rs.185 in Q3 FY2020, and the prices of H-acid is around in the range of Rs.240 to Rs.500 per kg, which was around 350 in the Q3 FY2020. Along with the prices, the demand scenario has also improved globally after the ease of trade tension between the U.S, and China and end of holiday season in December. In the domestic market also, we believe consumption level should improve gradually from the current levels.

On the business strategy front, as you are aware we have opened several warehouses and marketing offices in India and overseas as well, which we will be adding further in near future as per requirement. In addition to that, we acquired 80% stake in Sener Boya, a Turkey-based company, and opened a subsidiary company in Bangladesh mainly for marketing of our dyestuff. We will be increasing the share of B2C in overall dyestuff business going ahead. All these efforts will increase dyestuff share in total revenue, further integrate our business leading to stable margin and increasing profitability in the coming years.

Our total production for Q3 FY2020 improved by 11% year-on-year to 52,084 metric ton. Our dyestuff production grew by 11% year-on-year mainly due to increase in capacities while basic chemical production grew by 13% year-on-year mainly due to higher utilization and additional of Thionyl Chloride. Production of dye intermediate was flat year-on-year. Thionyl Chloride production has picked up and reached to almost 50% utilization in Q3 FY2020 and it has further improved to almost 90% utilization in January 2020. Total production for 9-month FY2020 grew by 3% year-on-year.

The Board has approved acquisition of 100% stake in Trion Chemicals. Earlier, we were facing challenges to run the plant due to partnership nature of the business. Now we are confident to start the production at Trion from April 2020 and we will expand our efforts for marketing in U.S. market. With these changes, we believe it should be turned into profitable in near terms.

I am confident about the business outlook in the near term due to favorable industry scenario and increase in the prices of our finished products.

As far as sales to China is concerned, it has reached to second number as far as the list of our export countries after South Korea, but over there, some fluctuations are there, but we do have other destinations where we can make up if China is not working there are other 45 countries where we export, and as far as raw material is concerned, there are few raw materials for which we are dependent on China. That is like J-Acid, Tobias acid and Thionyl Chloride. These are some raw materials, which we source from China and we are happy to tell you that we already have about 3-month stock what we consume for these 3 raw materials.

In my limited understanding China is a major producer of dye intermediates,especially Hubei province for Vinyl Sulphone.So this Coronavirus situation can increase realisations for Bodal.

1)But China and South Korea are their top 2 export destinations for dye intermediates,incidentally they are also top 2 coronavirus affected countries.So would this dampen their export demand?

2)Textiles is a end use industry for dye stuffs.So if the situation extends a while longer,could a drop in textile production affect dyestuff sales?Would then Bodal be able to divert that capacity to cater to another end use industry?

Any views? @bargainHunter

1 Like

Such a free fall in this share. Management is more worried about warrants and expensive acquisitions rather focusing on business. They did everything to fool market with rosy expansion plans but could never execute them. Now they are talking about venturing into speciality chemicals. First i thought it will consolidate around 75 than 65 now way below 50. may be in this downturn it may touch 25. They keep posting terrible results YoY and AR talks about how they have been doing great business.

If they have been doing great business why isn’t share price reflecting same? If not for disruption in China this loss making company would have been history by now.

Management can pat their back because they managed to fool mutual fund houses not only retail investors.

Disclosure: Invested but reducing.

1 Like

Bodal Chemicals (BC) announced a capex of Rs 360 Crores (https://www.indianchemicalnews.com/chemical/bodal-chemicals-to-invest-rs-360-cr-for-expansion-7153). This news has excited me to consider investing in this company. After reading this entire thread, I am summing up the points for the benefit of investors who visit this thread.

- BC manufactures dyestuffs, dye intermediates, basic chemicals and its variants

- BC had an unusual growth in topline and bottom line due to the closure of factories in China due to environment concerns, H-acid a key dye intermediate price shot up the roof

3.BC felt the changes in Chinese environment laws are a structural change, that their topline will grow by 20% - Capacity expansion to achieve increased topline, mentioned “capacity expansion will take place with internal accrual” in earning calls till Mid 2017

- Took a U-turn and did QIP which is less than the prevailing floor price

6.ICICI MF has heavily invested in QIP

7.Stock price went up just before the QIP, company did not achieve this price ever after

8.Promoters grant options in Jan '18 - Some promoters sold their holding during Jan-Feb '18

10.Promotors bough chunks of shares in May '18 - Market did not react positively when BC gave stellar results in a quarter

- Stock price remained subdued till date

Conclusions:

1.Company went for an expansion at the peak of the cycle

2.Company did not walk the talk on 2 counts, QIP and 20% increase in topline

3.Looks like market has discounted this company

Seniors who invested earlier should share their lessons learnt.

Disclosures: Did not invest and don’t plant to invest in the near term

7 Likes

Bodal chemicals is into commodity chemicals which by nature there is lot of competition.Because china’s blue sky policy most of the Indian companies had dream run but then they are back now. Product prices varies dramatically depends on demand scenario. FYI, Icici MF completely exited bodal chemicals.

Hi

is any of you tracking Bodal. Bodals presentation looks very impressive.

They have made many acquisition, forward and backward integration.

It looks promising future. I am not from Chemical back round. I could not capture full potential/revenue visibility due to lack chemistry knowledge.

Anyone have idea about potentials of caustic soda, benzene products etc which are new additions. Any idea about competitors

I have sold my shares but let me state my understanding:

- Bodal is into commodity chemicals where the competition is pierce and margins are very thin. prices vary based on demand.

- very dishonest promoters. They did QIP around 170 last time as well so we did see similar presentations just on time for QIP and nothing there after

- Never seen promoters engaging with minority share holders.

4 . They were trying to venture into speciality chemicals but not sure

In all honesty, Promoters are not minority share holder friendly so tread with caution.

5 Likes

Thanks for your insight and clarifications.

Fully agree with @lokeshreddy2007. Best avoided. I sold out at a loss because I came to the same conclusion. The only thing I would add is they also haven’t been successful in running their business. Failed to turnaround two businesses they acquired and just trying to ride the Specialty wave with announcements.

Bodal experience taught me a few things 1) Come to terms with booking losses and to book early when you are not comfortable with management quality 2) Firm up my conviction not to invest in suspect companies even if that means foregoing a potentially lucrative ride 3) Take note when a marquee investor hastily exits soon after entering (Ashish Kacholia here and Mohnish Pabrai in Care). A good sign something’s wrong.

1 Like