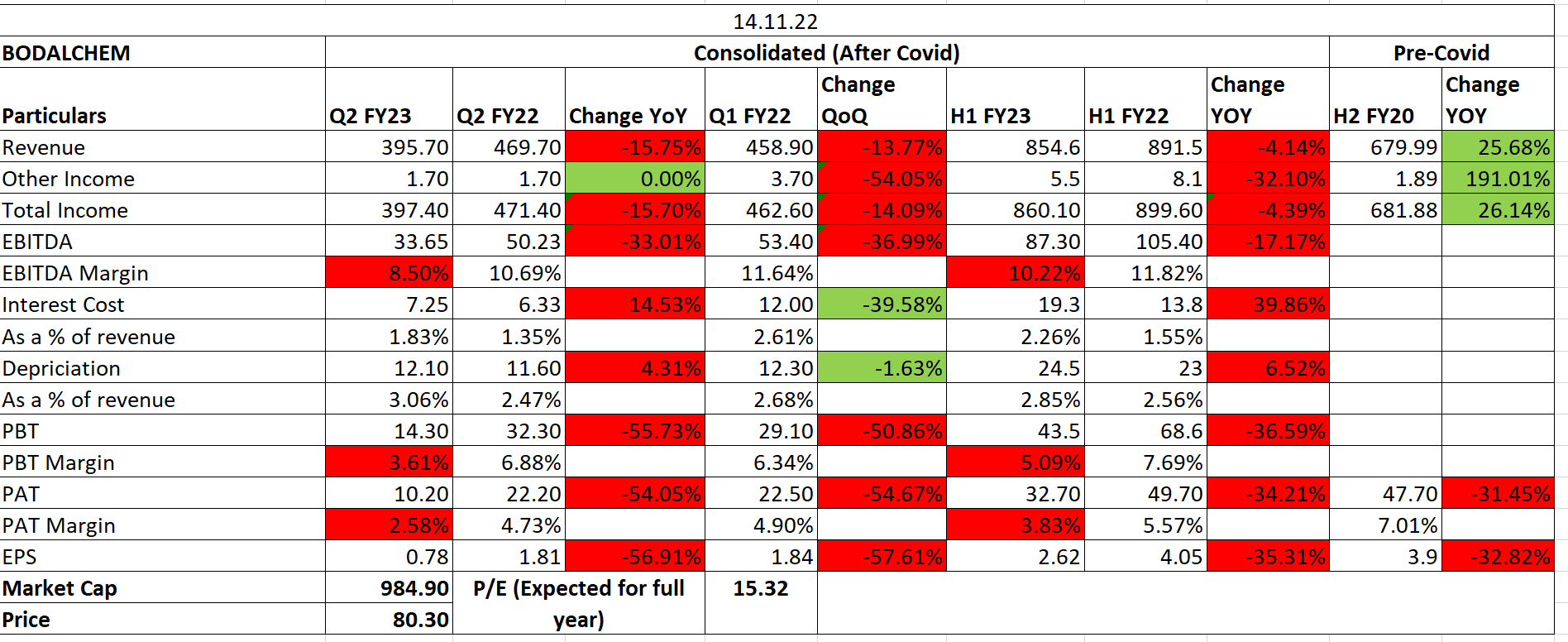

Great results for this Q

Anyone recently tracking and has any updates on this.

I have seen couple of post regarding bad management and governance, but fundamentally company has been doing all the good things. Seems weird things are not reflecting on price.

1 Like

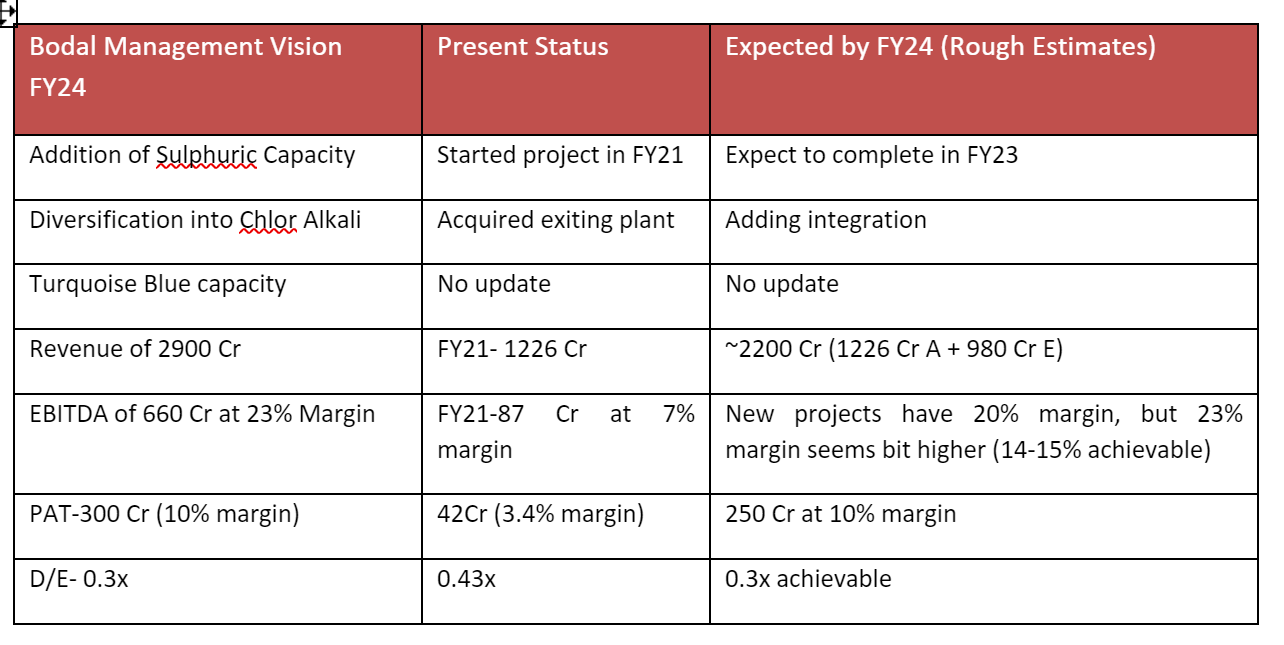

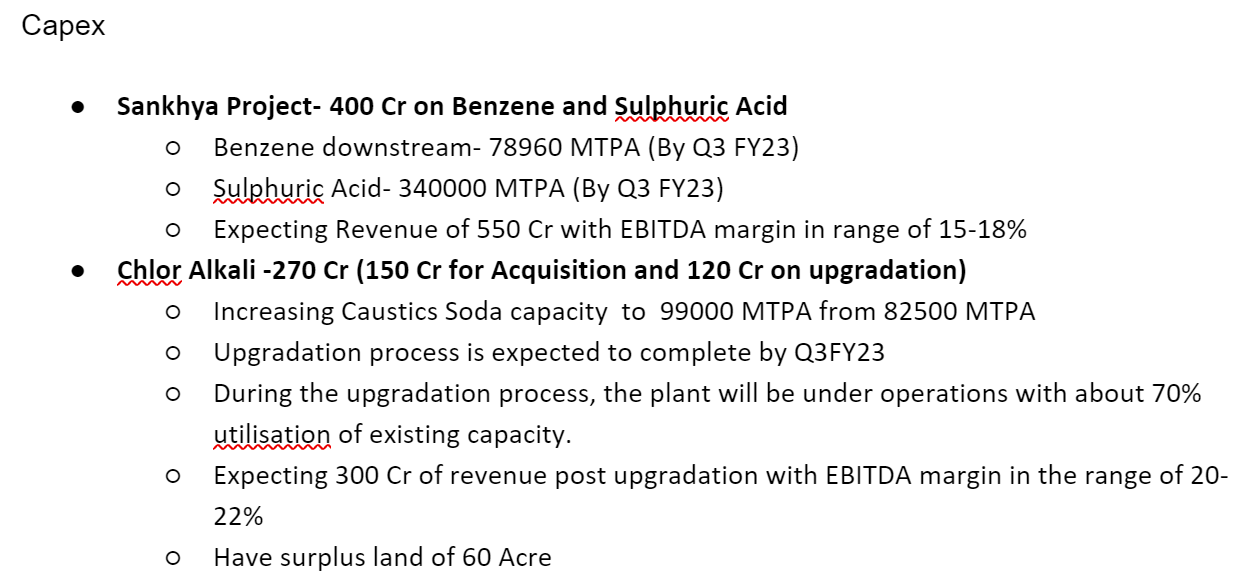

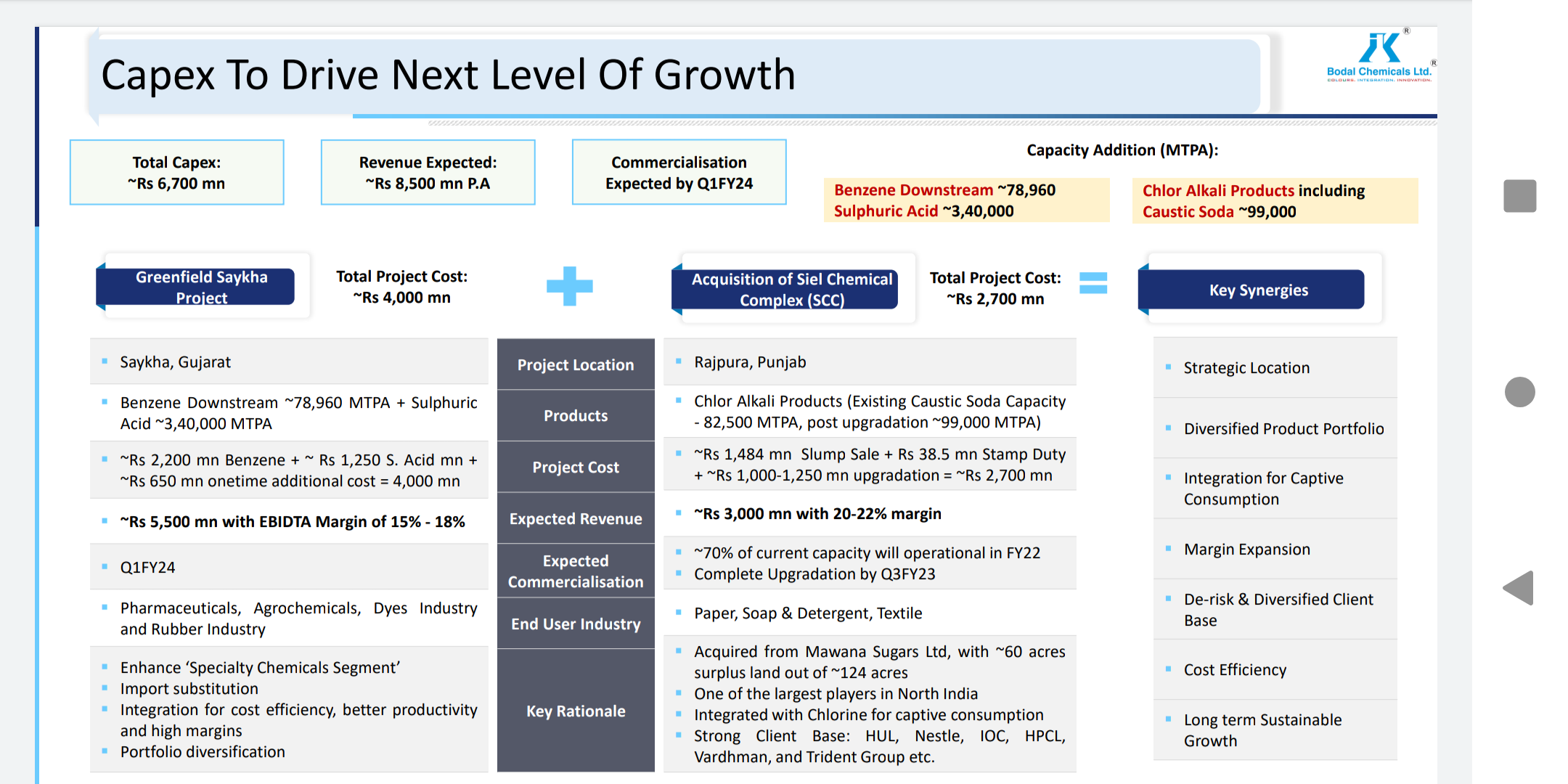

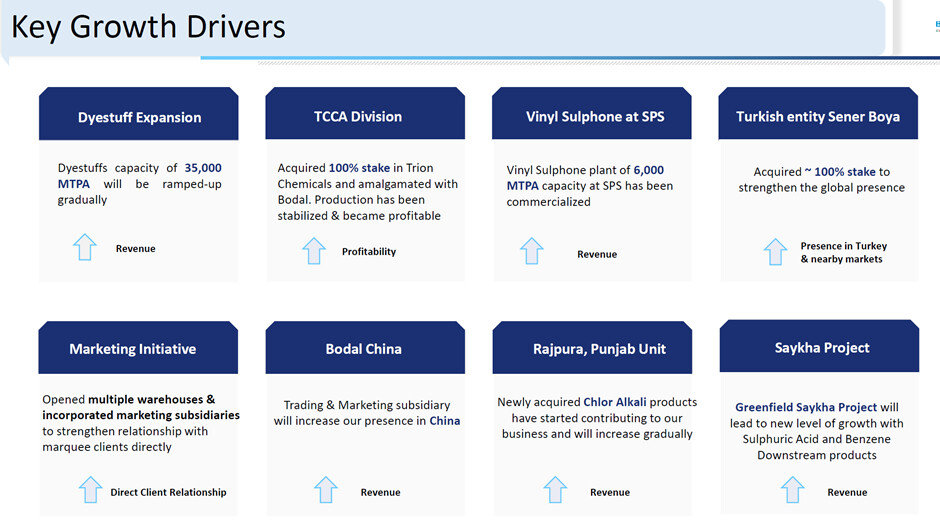

Everything material to this company going forward is summarised in the below pic. If everything turned out the way it is mentioned below, I think it will be an exciting opportunity looking at the growth triggers, current valuations and prospects. However, I would say that I am not a big fan of this company’s capital allocation decisions, business operations related decisions in the past.

Disc. Invested with a tracking position and adding gradually.

1 Like

| - | Dye intermediates have seen a subdued performance because of volatile consumption of end-user industries. Destocking of inventories is also going on. They are being imported to India from China. |

|---|---|

| - | Caustic Soda business has done very well. Technology upgradation at Rajpura Unit has been completed so demand for Caustic Soda will be addressed at better efficiency with lower costs. |

| - | Power, fuel & Logistics costs have increased. |

| - | Part of the construction activity has been delayed due to prolong monsoon and labor shortage in the previous two quarter. Our Saykha Greenfield Project is expected to start trial run of Benzene Derivatives in Q2FY24. Once this new site is stabilized, we will start the trial run of Sulphuric Acid by Q4FY24. As a part of the project review, product MPDSA, PNA, 2,4 DNCB is kept on hold. |

| - | Subsidiaries have not been performing well due to weak macroeconomic environment. |

| - | Global MNCs have started sourcing from India to de-risk their supply chain. Power crisis in Europe has started to give immense opportunity to India to gain wallet share in the market. |

| - | 3 strategic objectives: grow existing capacity, increase export business & finish Saykha project. |

1 Like

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/11c9ab50-5534-49b0-a134-04d15df224cd.pdf

New Projects of Specialty Benzene downstream products having capacity of 63,000 MTPA at Village

Saykha, Near Dahej, Gujarat. ( Company did 400 Cr capex for this Green field plant )

Company Expect 320 cr Revenue with EBITDA MARGIN 12 - 15%

Disclosure: Not invested

2 Likes