The Bitcoin is a concept that was first introduced by Japan’s Satoshi Nakamoto as a decentralised global digital payment system designed to negate third party interference during the course of an online transaction. But today, Bitcoin is being seen as the future of currencies as we know them, and as an attractive investment opportunity. I however believe that the Bitcoin is not an effective currency because it neither has transaction value, because it can’t be used to buy or sell stuff, nor does it store any value because it has no purchasing power in the first place.

And at the same time it is dangerous to invest in Bitcoin right now because prices are being driven more by speculation than by the actual underlying fundamentals, which is why I personally feel that it is only a matter of time before the Bitcoin party ends, and that all those who stay invested in Bitcoin for too long are destined to meet a tragic end and lose a truckload of money. So it would be wise for anyone at the Bitcoin party to quit and come home before they end up with a nasty hangover.

And while I feel that a digital currency is definitely the future on a 10-15 year time period, and we may well have a better online currency at the end of the 10-15 year period, I am fairly confident that the Bitcoin in its current incarnation doesn’t quite fit that bill, and that therefore the Bitcoin is more likely to be just another ‘flavour of the month’ story and not a paradigm shift in the world of currencies and online transactions.

I wrote a blog about asset classes, taking into perspective the macro scenario. The prices and declines seem to be moving in tune with the liquidity inherent in the world’s financial system. There is more to the price rise than fundamentals, infact I feel there are no fundamentals. There is just liquidity.

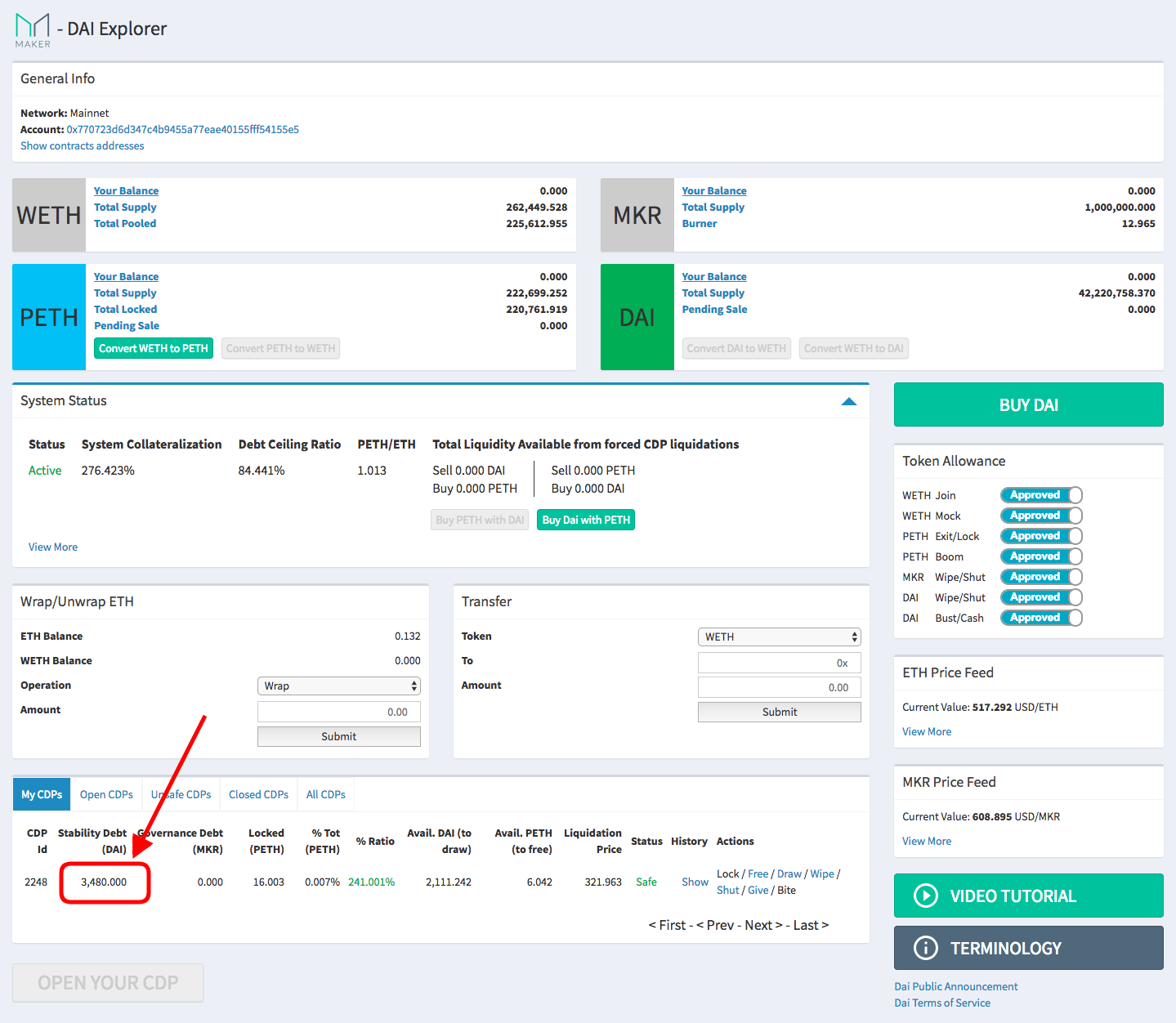

Blockchain based decentralised loan. 0.5% charged at the time of payback with no time limit. Only defaults if the collateralized asset (ether) plunge below certain level. Yesterday, we loaned ourself $3480 within few minutes (that what it tooks to get the transaction added to blockchain).

Gangtok-based State Bank of Sikkim (SBS) is a lender that is not regulated by RBI and therefore is not affected by the ban. However, the bank has made a strict internal policy that they do not want to support any crypto assets businesses.

Bitcoin is a libertarian experiment to create a sound digital money. Sound money is a prerequisite for capitalism, hence I want to see this experiment succeed. With that aim, I purchased very small amount of bitcoin, in early 2017. After riding one boom and bust cycle, I have become convinced of its robustness, enough to suggest upto 5% allocation to this emerging asset. It has successfully become a global speculative commodity, with a key advantage over other commodities for speculation purpose - its supply is rigidly finite. Not only has it become the most widely adopted blockchain, its critical governing rules have become immutable, as demonstrated by the recent failure of miners to increase block size so that they can have more transactions, and hence more fees for them, at the expense of increasing data space requirements for Bitcoin nodes. Therefore we can confidently say that it is now beyond the control of any single authority and its monetary policy is now set in stone, unlike other cryptocurrencies which are decentralised only in theory, but are controlled by a small team of developers and miners working on them.

But it is not a sound money yet. The most important property of money is its salability, it must be a commodity which everyone is willing to accept in exchange for their good or service. But due to its volatile nature, not many would want to hold bitcoin. Even if they are made to exchange their product for bitcoin, they will immediately dump it for fiat money. As such, there is no monetary demand for bitcoin, there is only speculative demand, and hence my rationale to limit the initial allocation to 5%. Rather, Bitcoin is a bet on the hope that as its value increases, as more and more people learn about it and purchase it for speculative interests, its value will become more stable, and being a conveniently tradable digital asset, it could become a unit of accounting for global trade, and a store of value, a reserve commodity, like gold. That is when its monetary demand will emerge and replace its speculative demand.

Decentralisation and fixed monetary policy are its most important features, which make it possible candidate for sound money. Since fiat currencies supply is determined by central banks, who eventually end up abusing their power and pump its supply to meet politicians promises, therefore debasing the currencies value and eroding the wealth of savers. If such a sound money alternative is available to savers, they will dump their currencies for bitcoin, and unlike gold, bitcoin cannot be forcefully seized.

But decentralisation also has its costs. Blockchain requires every node to maintain a copy of transaction ledger, which makes it very inefficient to scale. This inefficiency of blockchain technology makes it unsuitable for any application which requires a trusted third party, for example someone to enforce smart contracts in real world, because such application can be run more efficiently with a centralised solution by the trusted party. It also makes it nonsensical to have corporate or nation backed cryptocurrency, because if it is based on the trust in some corporate or nation, they might as well run a centralised payment processing system, as it will be much faster and cheaper. The only application of blockchain is to create a decentralised digital asset, whose value is not tied to any physical asset or institution, but is derived from its blockchain network, and at present bitcoin is the only truly decentralised blockchain.

With limited transaction capacity and high transaction time, blockchain will be suitable only for recording high value transactions. It will never be suitable for small transactions like buying coffee. We will still need trusted institutions to process such transactions instantaneously, however it is possible for these institutions to club these small transactions and use bitcoin blockchain for settlements and maintaining their overall balances. At present that seems to be the direction Bitcoin is taking with the development of lightning network to process payments off chain backed by the balance maintained on chain. With time, we can expect more such second layer applications built around using the first layer of bitcoin blockchain.

For more on understanding the need of sound money and economics of bitcoin, I would recommend reading “The Bitcoin Standard”.

Agree, there is a long way to go for bitcoin before it becomes a critical component of the world economy. Progress will also depend upon how governments around the world react to it; while no government can stop it, they can certainly make the convertibility of bitcoin to their fiat difficult, and they can also discourage the institutional adoption in their country.

So far, progress has been good, its adoption is increasing and both, the financial and technological, ecosystems are developing around it.

I think bitcoin is the very first experiment for sound money but at the tech level, the codebase which governs the bitcoin is fundamentally not that sound to adopt the global financial system - Open Finance.

My bet is more on smart contract blockchain platforms like ethereum (2nd crypto by market cap). Instead of just a medium of exchange, it’s more about financial activity that you can do on the blockchain.

+$600M has already been locked up as loans on the ethereum blockchain (source). And there are tons of projects being built for derivatives, insurance, synthetic assets, stable coins, etc.

I personally leading a project instadapp[dot]io where we managed to issue around +$1.5M with over $4.5M worth collateral on our platform with utmost security & privacy.

The overall Open Finance is at a very early stage but this should be future that blockchain is meant to bring. You can be your own bank. Distributed and no central custody yet fully secured and efficient. Publicly trackable & verifiable.

I am trying to understand whether there are other applications of blockchain where not having a trusted third party is actually desirable.

For money, you do not want any third party to control its supply, and an immutable monetary policy is desirable. Hence Bitcoin.

But can the same be said for banking? What if someone borrows without any intention to pay back? You can’t take any legal action without any government backing your blockchain.

And what about credit appraisal? I don’t believe it to be as simple as fixing a monetary policy. Someone will have to develop and maintain codebase for performing credit appraisal, and most of the lenders will put blind faith in rules programmed by the developer. But in that case, would it not be better to have a non-blockchain based solution by the same developer as that will be much more efficient and scalable, and the lenders already seem to trust the developer?

Linking my comment from other thread as that is relevant.

Depends how you distinguish investment from speculation. If you define investment as risking your present purchasing power to possibly have more future purchasing power, then you cannot distinguish the two. As it happens, I do have additional criteria for considering something as investment. For me investment is an activity where money is allocated towards creating something of social utility, that is, it must do something good for the society. If the value that is created is more than the value invested, then that makes a profitable investment.

By that definition, money betting on cricket matches is just speculation, but money going into stock market is investment. Because stock market is a means for business to raise capital, with the purpose of serving its customers better, that is to do something of value to the society.

Good thing is I don’t have to convince you of bitcoin’s utility, you have experienced it first hand. Bitcoin is not like other currencies which require dependence on banking infrastructure. The only question is whether you consider this unrestricted movement of capital across borders, that bitcoin offers, socially good? I do.

Bitcoin is an experiment to put the global economy on sound money - money whose supply is mathematically fixed, limited, and cannot be regulated. If you believe in the Keynesian principles - that money supply must be regulated for stability, it must be increased during recession and gradually decreased as growth returns, then you wouldn’t see any social value in Bitcoin - it is not just another currency but the worst kind of currency which cannot be regulated.

But if you agree with Austrian economics, then Bitcoin may have enormous social value in future, and you see it as an undervalued investment. By buying bitcoin, you are furthering the goal of putting global economy on sound money.

Sound money is a prerequisite for capitalism. Capitalism requires individual to have complete authority over his wealth. It is not the case if government can dilute his savings or even revoke access (think demonetisation). But the governments do want that power, and hence, they have adopted keynesian economics worldwide. Only keynesian economics promises to achieve all - economic growth, stability, welfare state. The politicians don’t have to make hard choices, of cutting government expenditure by making unpopular moves, say cutting unproductive government jobs, in order to fund their promises. The result is swelling government machinery, with its unsustainable expenditure and debt. A sound money will make government unable to do that. Do you consider that socially valuable? I do.

Sound money will have great implications for how individuals manage their finances. Since bitcoin is limited in quantity, it guarantees its holder a constant fraction of authority over entire economy’s resources. If economy grows, his purchasing power also grows at the same rate, to maintain that constant fraction. You no longer have to do index investing just to get market returns. It also changes people’s behaviour, from high time preference, where people prefer to take debt and consume as much as they can in the present, to low time preference, where people prefer to save and accumulate wealth for long term goals. The reason is simple. With unsound money, most people have bitter experience of saving, as they don’t find themselves much better off in terms of their purchasing power. Humanity’s progress rest on the low time preference behaviour, as humans tend to postpone some of their present needs, invest capital and effort in developing better technology, so that they can have more in the future. If Bitcoin’s adoption can increase the low time preference behaviour, then that certainly has great social value, isn’t it?

Lastly if you trust Austrian economist’s theory of business cycles, then you would agree that sound money will make the problems like recession go away. According to them, cycles are a consequence of drastically increasing money supply through fractional banking. When interest rates are cut, it does not immediately raise the cost of economic resources. It makes many business managers, who have access to these low cost funds, see profitable opportunities at present prices. So they go after them. But the actual resources haven’t increased, only the money supply has, and as these businesses compete for these common resources with their fresh supply of money, they find their costs rising until their projects become unprofitable again - as they were before this money was injected. The result is a mass failure of businesses leading to recession. This logic of business cycles does makes sense. The evidence also stands against the keynesian economics, the efforts to stimulate growth by lowering interest rates seems only to keep the world on lowering interest rates trajectory while the business cycles become more extreme, and that cannot go on forever. This problem of misplaning will go away with sound money. That again is a very valuable. The only question is whether you agree with this viewpoint, and what chances you see of bitcoin achieving it?

Unfortunately it looks like bitcoin may be banned in India.

If ability to convert bitcoin to INR is important to you, it may be good to get out now, instead of selling in a rush, with possible loss, when the ban becomes law. Hold bitcoin only if you are okay with not being able to convert it to INR.

Government policies around the world will certainly determine the pace of bitcoin adoption, but it cannot be killed. If it succeeds, the early adopters would be rewarded, and eventually countries’like India will come to accept it.

if i have to give a crude analogy, Bitcoin is something like the concept of a “global citizen”

while theoretically it looks so great, i wonder if central bank of any country would allow such currency to have a hold in their country.

what then happens to their own currency ?

will they easily give up their authoritative power ?

alternatively, i find things like XRP or stellar a bit useful because they are solving so real world problem like the cross border money transmission issue. but again, unless govts allow the conversion to fiat, i donot see any hope.

Ofcourse most central banks will prefer to maintain the status-quo, however some economically free, likely smaller, countries will see more benefit in attracting bitcoin capital, the employment it generates through its ecosystem, and possibly have added incentive if they hold bitcoin reserves. Other countries may be forced to follow as bitcoin gains in popularity and the wealth loss from banning bitcoin becomes more than the supposed gains from currency control.

The above statement is a speculation and things may not happen that way. It is possible that bitcoin experiment will fail as institutional investors stay clear of it and all governments ban it. At any rate, bitcoin is our greatest chance to free money supply from government control, which would be a huge positive for global economy as business cycles may go away and there will be less human effort devoted to speculative activities. For me, it is a philosophy driven investment, and I will take that risk irrespective of outcome.

Ripple, as you yourself admit, doesn’t threaten the status-quo. As far as I understand, it is a trust based (you need trusted validators) payment system, introducing yet another controlled currency. It is easy to create a trust based payment system with government backed currencies, as Facebook is doing. They may improve the existing payment infrastructure, but they don’t have the far reaching consequences, and hence value, that the adoption of sound digital money with immutable monetary policy offers.

Reading Grokking Bitcoin, an excellent book to understand the technological aspects of Bitcoin. It starts from a simple spreadsheet based payment system, and keeps adding new features to it, explaining their rationale, until you have Bitcoin network in the end. As the video mentions, it is an incredible invention, putting together so many key ideas from economics, computer science, cryptography, and psychology. It’s hard to imagine how Satoshi got so many things right, given how complex this system is, yet it has run exactly as intended for ten years. Clearly the work of a genius!

Of course one need not understand all the technological aspects to appreciate Bitcoin’s economic value. The Bitcoin Standard gives a good explanation of economics of bitcoin.

PS: both the authors have made their book freely available online.

Whether Bitcoin is risky or not is for investor to decide, not the regulator. This is a positive development and will help the adoption of Bitcoin in the country.