BEPL 34th Annual General Meeting

Financial guidance and Strong growth story

http://totalinvestments.blogspot.com

Any thoughts if this method is better than hedging?

I think management is over promising and we should take it with a pinch of salt.

1 Like

At the AGM, these numbers were already provided with a word of caution. Mr Bhansali said “projections are after all projections”.

However, he also said that this will be the first quarter when the company will cross 400cr in revenue. He was then asked if this run rate will continue for the upcoming qtrs and the will the company achieve 1600cr for the fiscal. To which he pulled up a sheet of paper and said that they expect to cross 1800cr in revenue, if things go as per plan.

Last quarter was 201 Cr (due to fire incident), before that 301 Cr. I would be happy if they can achieve 350 Cr this quarter and 1400+ at the end of the Year. Promising above that is being over ambitious.

I already know that. Putting my assumptions on this platform is for a reason, to get counter views of different folks having different thinking but looking at same stock.

So let me summarise your assumption - even though the company is halfway through the fiscal they could be off by 450cr on a base of 1800cr?

Yes, as last quarter they did 200cr plus ~350 Cr for next 3 quarters gives 1250 Cr. adding 100 Cr assuming performance could be bettered by mgmt we can come up with 1350.

Last qtr they worked for 1.5months only and did 200cr. So if they work for a full qtr, how much would that be? That is simple mathematics.

Besides, do you know that Q3 is the festive qtr?

There should be some logic to assumptions too. Just being conservative for the sake of it doesn’t give a realistic picture.

Jointly owned by renowned chemical manufacturers Sumitomo Chemical and Mitsui Chemicals, Nippon A&L is strengthening its supply chain network that spans Asia and North America. It has factories in Japan and a joint venture for plastic compounding and sales offices in mainland China and Hong Kong. Nippon A&L operates in Thailand and other Asean markets through a joint venture with IRPC, and has built a solid client base in India via a joint venture with Bhansali Engineering Polymers.

Bhansali has reported Q2 number. Sales growth in value term is encouraging 350 cr vs Q1 of 201 cr. EPS IS flat qoq at 1.02. Company has 11cr of forex loss due to strenthening of dollar against rupee.

Revenue growth is remarkable, I guess it touched record high this quarter in company history(correct me if I am wrong please). Want to understsnd this 11cr forex loss you mentioned. Where to look at the result for this? Could you please explian, I did not find it.

Disc : Invested

Looks like company paid too much in order to save 1.5-2% cost to bank!

1 Like

The gross margins are down to 20% from 28% YoY and 27.5% QoQ. It looks like they are not able to pass on the increase in RM costs due to rise in crude.

Increase in crude as well as depreciation of Rupee - both have hit in this qtr. But they have very well survived such severe onslaught. They work on cost plus model and therefore should be able to recover increased cost in subsequent qtrs.

Disc : invested since long.

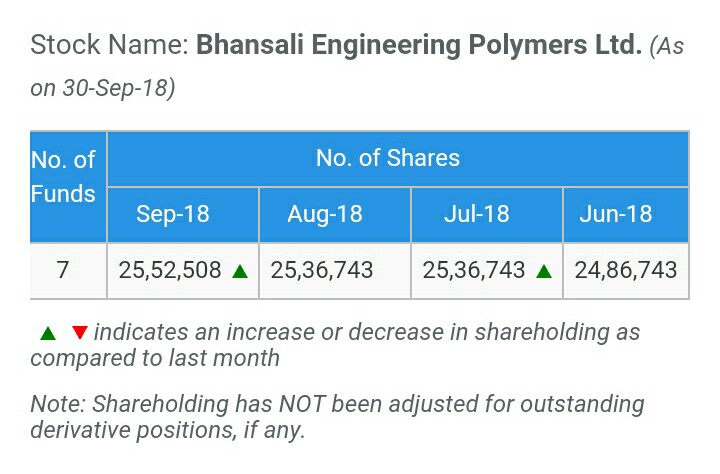

Continuous increase of shareholding by Mutual funds are a good sign and showing trust on Management and business pattern. Which clearly showing in topline growth. How mngmnt will tackle the bottomline due to crude price and dollar strength that is a vital thing to look forward.

Crude and dollar loss will be passed on to the customer and will be seen from the next quarter…on top of that management already said that revenue will be 400 cr plus in this qtr so drastc rise in bottomline can be seen from next quarter…

Incidentally- one of the biggest strength of Bhansali is that it is debt free. So no interest rate hike risk and no possibility of default like ILFS and many others.

1 Like

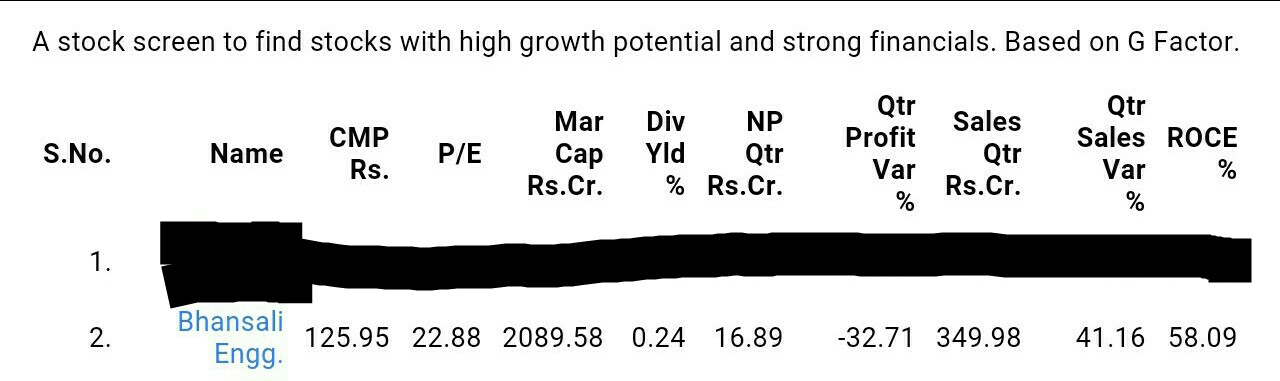

BEPL is coming under high growth potential stock based on recent quarter result and financial status.

Total income up 40% from Rs.250 cr in Q-Sep-17 to Rs.350 cr in Q-Sep-18.

PAT down from Rs.24.77 cr in Q-Sep-17 to Rs.16.76 cr in Q-Sep-18

Rs.11 cr forex losses in the Q-Sep-18.

Huge jump in material costs (Cost of Materials, Stock in trade and change in inventory) from Rs.178 cr in Q-Sep-17 to Rs.280 cr in Q-Sep-18