Main concern is whether they are able to pass on the price to customer or not… As far as I remember, Management has said in past that they are able to do it

Acrylonitrile price is varying this way ,Its an imported product so import price was 154 Rs/KG at june end and on Sept end it was 175/KG. currently the price is trading in Indian market around 162/Kg.this is the major Petrochem component of abs plastic. So any price variation in this component will hit the ABS price most.

Styrene Monomer(SM) was at june end 102 Rs/Kg and shoot upto 111 Rs/Kg in Sept end. Now trades at 107 Rs/Kg.

ABS and SAN price was trading higher till Sept end and cooled down now… ABS is trading around 150-165 Rs/Kg. Remember ABS has multiple grade and thousands of color very difficult to say price of different grade. Also this are spot price not sure about the contract price of Bhansali.

Idea is to display the variation in recent past. Product have different grade,ex-port price ,retail market price etc…

2 Likes

Two observations

1 Being a cost plus model, they should be able to pass the increased cost.

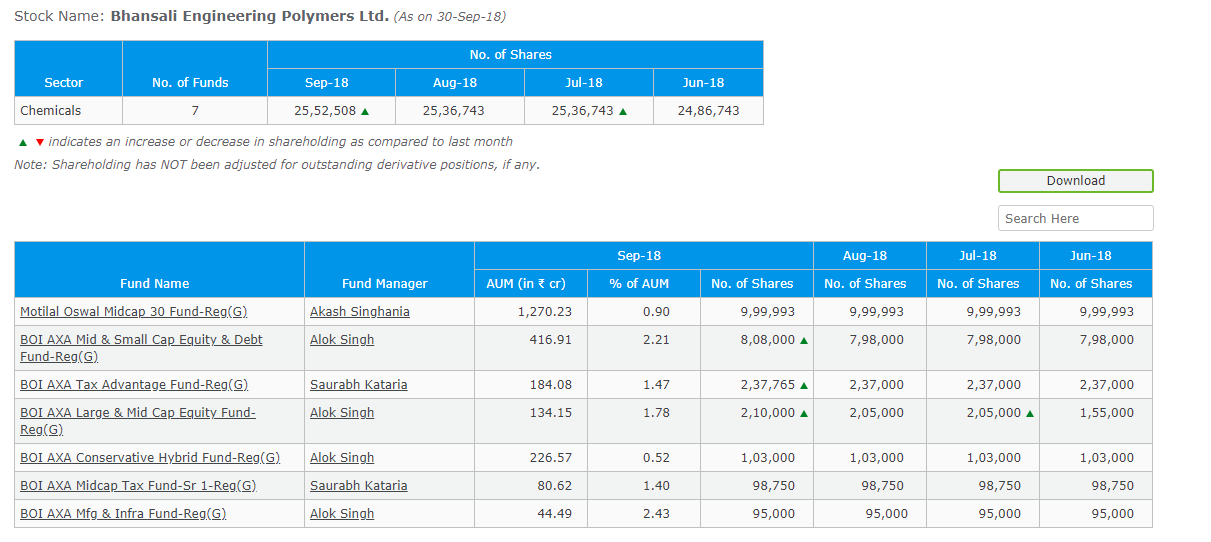

2 Motilal 35 Mutual Fund had made an entry in this a couple of months back. We need to see if they have sold off or are increasing their stake- making use of the price fall.

Where this came from? i have not seen it anywhere

mainly over the internet,india mart. You can register with Indianpetrochem.com…Paid service update the price daily basis.They have android app. Don’t know the subscription amount monthly.

Yesterday in the first 5 mins of trade around 1 million shares are sold that lead to 20% circuit. which matches to Motilal’s holding. I am guessing they might of sold their holding.

Disclosure: holding BEPL, 5% of portfolio, currently no plans to sell.

2 Likes

Can you please elaborate why you think it should happen in subsequent quarters and didn’t happen this quarter ?

10 new Mutual Fund has requested to arrange a investor analyst meet today. Also another 3 MF name submitted by mngmnt with same agenda in the evening,which is scheduled for tomorrow. I see this as a very positive development but somehow market reacted in a different way by putting the stock price in a lower circuit today. How to interpret this development,requesting fellow forum member view please.

Disc : Invested,added few today in lower circuit.

@S_Banerjee - Q2 results were bad as the gross margins deteriorated quite badly on both sequential basis and yoy. This is a commodity business and even now is probably trading at about 20 P/E based on FY19E earnings. A lot of distribution has happened here in the last two years if you see the retail holding which has doubled during the time. There were several warning signs and the deterioration in margins if annualised looked quite ominous. I don’t know if the price-action needs any more reasoning.

5 Likes

Okay, accept your point. But how can we justify the highest sales number reported this quarter. And how to explain this 11 cr PAT adjustment due to foreign exchange appreciation.

Anyone can give highlights of recent institutional meet?

https://www.plindia.com/ViewReport.aspx?rpt=2680

A sell-side report that tries to explain Q2 numbers.

"The company had to import HRG after the fire at the Satnoor plant to meet the deficit in their in house production. Due to the rupee depreciation, this cost shot up.

Gross profit/kg was up 0.8% YoY to Rs 40.7 but appeared significantly lower sequentially. This was because during Q1 the company sold majority of specialty grade due to the fire at the plant which resulted in superior margins (Rs 61.6) but was an aberration. "

Ignore the TP in such reports - they serve no purpose

forgive my novice question - Not sure why you find the above explanations not useful on import on HRG and gross profit per kg? Am I missing a link…?

ABS price is in new low. Weak demand from auto sector, new lower cost of raw material putting pressure on ABS price.

1 Like

Raw material prices are also in down trend so can’t say what will be impact on margins…

Can anyone elaborate whats the spread between its speciality grade and normal grade ABS?

Only organised Indian rival Ineos Styrolution’s partnership with TVS motor in some of its new popular 2w model. Posted to give better idea about ABS usage in auto industry. Vechicle weight to come down drastically starting from april 2020 with new emission norm BS VI,will encourage high grade ABS usage more in vechicle.

Rajiv Verma, Head of India Automotive, INEOS Styrolution, said:

“We have been working closely with TVS Motor for more than 10 years and we are very pleased to partner with such a strong local two-wheeler company in India to come up with the best solution and supporting them to stay at the top of the industry.”

I found this interesting in the link posted, it says INEOS has been working with TVS for 10 years but on the BEPL website, TVS Motors is listed as one of their automobile clients:

http://bhansaliabs.com/marketing-2/marketing/

I’m a little confused as to how companies tie up with ABS manufacturers. Are all of TVS’s needs met by either one of INEOS/BEPL or are different grades purchased from each company?

disc: invested

Hi, could you share the link from where you got this info, would love to track it myself.

Client company may go for multiple vendor to reduce raw material supply crunch situation. This is very common practice.

Another Analyst/Institutional Investor(s) Meeting scheduled on 10.12.2018.