Company’s responses to my queries:

- The company has put on hold the expansion plan to 137 ktpa. Does the company foresee reduced demand going forward?

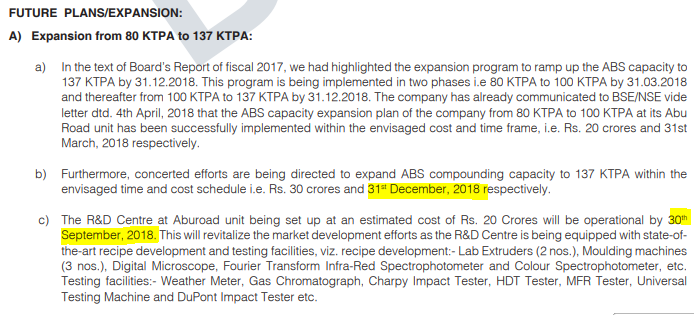

Capacity expansion from 80,000 Ton to 1,00,000 Ton was completed by 31-03-2018 at a Capex of Rs. 20 Crore which had to be expanded to 137 KTPA by 31-12-2018 with a capex of Rs. 30 Crore. The Board of Directors in their meeting held on 14-07-2018 deemed it prudent to keep the further expansion in abeyance on account of the companies plan to re-orient it product management strategy so as to position highly remunerative grades of ABS in automotive market segment.

In order to achieve this goal what is required, is strong R&D back up. The companies state of the Art R&D center will be commissioned within the current year and product diversification strategy, as aforesaid, will be achieved. Therefore capacity utilization enhancement to be achieved through increasing sales of low profitable GP-ABS grade was not a chosen path. There is no loss of opportunity cost as efforts are being directed to optimise the profitability through the concept of niche marketing.

My response to that:

Regarding the capacity expansion from 100 kTPA to 137 kTPA, you have mentioned in your email that, “Therefore capacity utilization enhancement to be achieved through increasing sales of low profitable GP-ABS grade was not a chosen path. There is no loss of opportunity cost as efforts are being directed to optimise the profitability through the concept of niche marketing.”

However, the company’s financial results for the quarter ended Dec 31, 2017 had the following mention

Hence, I’m unable to understand how the expansion which was a “cost effective expansion strategy” until Dec 2017 is no longer a “chosen path” in July 2018. Why this 180 degree turn in strategy? What went wrong in decision making - did the company not gauge the market accurately?

Besides, it is unclear to me what you mean by “optimise the profitability through the concept of niche marketing." Please elaborate on this.

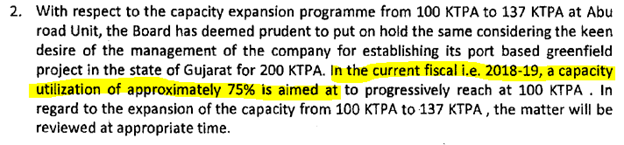

- The company aims to achieve 75% capacity utilisation of the 100 ktpa current capacity. Why is the capacity utilisation capped at 75% only? Has the demand for ABS polymer come down? Is this due to cheap imports from China?

Capacity utilization for F.Y 2017-18 was around 66000 TPA out of total available capacity of 80000 TPA during the said period.

100000 TPA is the aggregate ABS & SAN manufacturing capacity at ABU Road as of 31-03-2018. HRG is manufactured at Satnoor, M.P. with the capacity of 15000 TPA exclusively for captive consumption at Abu Road plant for manufacture of ABS only.

My response to that:

This means that capacity utilization was approximately 83% in FY18 (66000/80000 = ~83%). However, the company is targeting only 75% capacity utilization in FY19 according to the company’s Q1 FY19 results below.

Why is the company aiming for lower capacity utilization in FY19 compared to FY18? Has demand for the product come down? Or has competition intensified?

Let’s see what they come back with.

Somehow, the fact that the mgmt. acquired large number of shares in this year’s correction, gives me comfort about them having lot of skin in the game.