Revenue lesser yoy/qoq.

Proflt lesser yoy/qoq

135 kpta expansion put on hold.

Aims at 75% capacity utilization.

EPS of 1.01

The following has happened to the company in Q1

- Sales have declined sharply from Q4 18

- profit and allied returns have all declined

3)n The company has put on hold immediate brownfield expansion - the company talks of achieving 75% capacity utilisation

A)the company has not clarified whether sales loss was due to the fire.

b) It is unclear whether sales have crashed due to reduction in demand

c) Why has the company cancelled expansion plans

d) Are there pricing issues due to cheap imports from China

Can someone call the company. I am abroad and currently unable to reach the company.

I am not interested in the talk about Greenfield but need information a -c

could anybody shed some more light on the Greenfield project which company mentioned in its latest statement released to the public?

As per my info, green field project was dropped long back and they had proposed brown field expansion which now has been put on hold as per the latest news

If the results are viewed in the backdrop of the fire where production was down for approx 5 weeks (35% of the time of a quarter), they are not bad.

- Net of GST (last year there was no GST in Q1), sales have declined only 10% yoy and PAT is still flat i.e no decline there.

- EBITDA and PAT margins have gone up yoy.

- Due to the loan repayment in Mar '18 to Allahabad Bank, and the subsequent release of pledged shares, interest cost has come down to 1/3rd of Q4 FY18.

Need more clarification though on the hold up for capacity expansion from 100 to 137 ktpa. Have written to the company seeking clarification.

All said and done, do not think the fundamentals of the company have gone bad. One fire incident does not a bad company make!

Besides, share purchases by the mgmt (Jayesh Bhansali and DN Mishra, company secretary) in Feb and May 2018 were reassuring.

I am in total agreement with the report that it is a one off decline due to fire incident. The demand from cars and other white goods , for its products, continues to robust.

I think it is a golden opportunity to accumulate.

Disc: invested and plan to add more to take advantage of decline

I have a slightly skeptical view about next few quarters of the company. I am looking at the broader picture as below.

Initially company wanted to increase the capacity of both Satnoor plant and Abu Road plant. Plan to increase HRG capacity at Satnoor was dropped first, while the capacity of polymer plant of Abu Road was increased from 80 to 100. This created the need for importing HRG. The cost of importing HRG is very high that was further fueled by rupee depreciation. Fire at Satnoor plant may be related to efforts at maximizing production of HRG at Satnoor. This is however purely speculative.

Now company has dropped its plan to further increased polymer capacity at Abu Road plant (100 to 137). This is because importing HRG for increase ABS polymer capacity at Abu Road is not economical. HRG is to be produced in house for the sake of economics. The company therefore took a rational decision of dropping the plan of increasing capacity at Abu Road plant.

With increase crude prices and weak rupee, the raw material costs of the company may remain high, while the topline will stagnate. In all probability the company will remain profitable, but the growth will occur only after the production starts at the new greenfield plant. That is 2 to 3 years from now. The ABS scenario may change in future. Investment in company at this point will be totally speculative.

Disclosure - Not invested and not thinking of investing during this FY.

1 Like

“Fire at Satnoor plant may be related to efforts at maximizing production of HRG at Satnoor.”

Do you have any concrete evidence on your comment? If not please refrain from speculation. Not up to the mark of this forum.

@S_Banerjee

My comment fits with the overall view that I have given. Do you disagree with the overall view also. Please comment.

1 Like

In the absence of any explanation from the management for dropping the expansion plans, these kind of possible reasons will emerge.We need not be harsh on the members who try to debate possible reasons

2 Likes

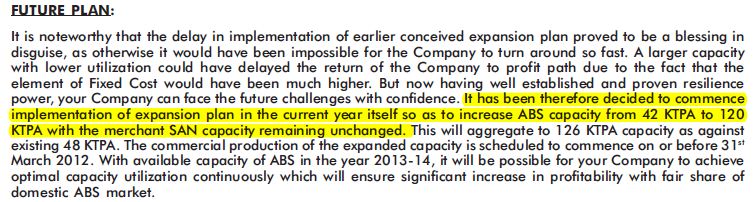

Company has a history of going back and forth on its expansion plans.

- They initially planned expansion in 2010

Source Annual report 2009-10

- It remained a plan in 2011

Source Annual report 2010-11

- And then they shelved it in 2012.

Source Annual report 2011-12

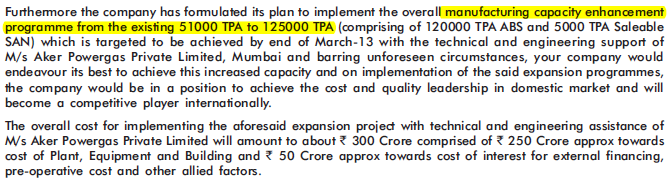

- More reasons in 2013 why expansions could not be done.

Source Annual report 2012-13

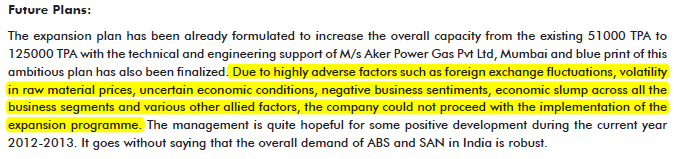

- Expansion chatter came back in 2014

Source Annual report 2013-14

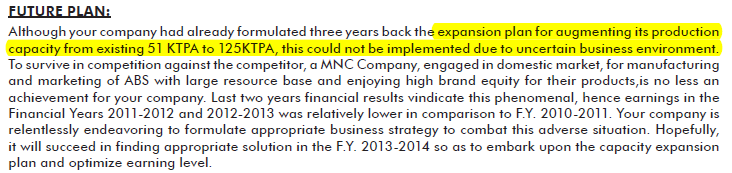

- Big expansion plans came back in 2015

Source Annual report 2014-15

- Finally some real expansion in 2016 !

Source Annual report 2015-16

- again planing for major expansion even though last one took years

Source Annual report 2015-16

-

In 2017, focusing on short term goals

Source Annual report 2016-17 -

while dreaming big…

Source Annual report 2016-17 -

And now in 2018, putting even the short term plans on hold.

There was a inventory drawdown in each of the last 3 quarters of FY 18. If the sales is rising, I would expect inventory to rise as they would ramp up production. In Q1 of FY 19, there is a huge build up of inventory probably because the fire at the plant must have stopped production while RM deliveries started piling up. Since company maintains only a small finished goods inventory, they were not able to fulfill the orders, hence drop in sales.

It will be important to watch next quarter sales to see if they make up lost sales or this is turning out be a slowing demand scenario.

14 Likes

Good compilation. However, you have missed out on two important recent updates

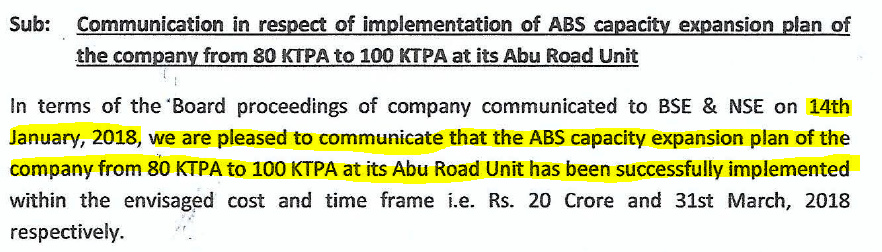

- After the expansion from 51 to 80 KTPA in 2016, it did another one from 80 to 100 KTPA in FY18.

Source: Exchange filing dated 13 Apr 2018

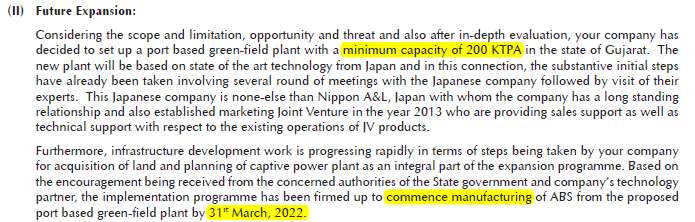

- Also, the port based based facility is likely to be advanced from Mar 2022 to Mar 2021

Source: Q3 FY18 Results

2 Likes

Also, there hasn’t been a consistent inventory draw down in the last 3 quarters as you have pointed out. The change in inventory (ending period inventory - beginning period inventory) has been fluctuating:

Q1 FY19: -75.4cr (inventory draw down)

Q4 FY18: 18.7cr (inventory build up)

Q3 FY18: -0.1cr (inventory flat)

Q2 FY18: 22.1cr (inventory build up)

Company replied to my following mail after 2 months !

Reply : The net fixed assets of the company have never reduced in any year since 2008 due to the expansion and continuous improvement policy being followed by the company.

The decline in Gross Block was only during the year 2016-17 wherein also the revaluation reserve of Rs 7270.75 lacs were reversed. Pl go through note no 35 of the Notes to Account of the Balance Sheet for F.Y. 2016-17

The answer to query No. 1 should resolve your query herein.

Whenever there is MAT (Minimum Alternate Tax ), % is low. Further whenever there is huge expansion in any one year the tax percent goes low due to benefit of additional depreciation.

The company has entered into a Joint Venture in 2015 with Nippon A & L of Japan, to develop products which are used in the Automobile sector and where the margins are high. The product development and approval process takes around 1 year on an average in the industry. Due to development of high remunerative grades for the Automobile sector with the help of JV partner; the margins improved during the last 3 years. The margins are expected to continue at the same levels. Due to a strong demand of the company’s product in the market; the pricing power of the company is strong.

There is no sales made by the JV company . It is only entitled for Royalty & commission on the products developed by them. Their role is well explained in reply to your query no 5.

The answers are hard to accept and does not fit well. As they said that Lower Tax percent is due to some additional Depreciation on new capacity but in the last 10 years , there is a negative Capex of 62 Cr.

Also Net Fixed assets have declined while intangibles assets have increased.

Investment will Bhansali Nippon and such high commission does not look well which will be continued

8 Likes

Thanks for sharing all these.

I could not understand Net Fixed Asset part in their reply.

Reply to Tax part looks ok.

From the post about expansion, I concluded that management takes benefits from bull market to push stock using expansion story. One post says that mgmt talk about big expansion plan and talk about that for years but later dump it.

Disc: invested in small qty recently.

2 Likes

Hi, I could not understand your cumulative capex part. I went through all the AR’s since 2008 and looked for the cash flow statement, I found capex to be positive only every year. Could you please let me know how you arrived at negative figure, I might be doing something wrong to arrive at that figure, hence asking. Thanks

Hi Bharat19

First of all thanks for sharing your communication with BEPL investor cell.

I understand, the explanation on margin expansion makes sense. The JV has been made as a channel to pay royalty to NIPPON.The work of JV is only to develop some high margin polymers, which can be made with some slight tweaking in polymerization process. Rather than developing on it’s own, the company took help of NIPPON.

NIPPON in turn is getting royalty by sharing the process and that too in a market where it’s not present and doesn’t wish to come in near future.

Disc: Invested

The issue is that the company’s Net Profit in 2017 was 34 Cr while it paid 4.26 Cr as Royalty which comes out as 12.5% ! Promoter’s take salary at 11% (Ceiling).

Quite uncomfortable with these numbers.

Kept it in watch list. Will look for upcoming 1-2 quarter results to see whether margins can sustain or not !

3 Likes