Middle Class Shock: Good Quality Jobs Are Vanishing In IT, Finance And Telecom

The next couple of years wont be easy for HFC, NBFC, MFC, Consumption related theme.

Middle Class Shock: Good Quality Jobs Are Vanishing In IT, Finance And Telecom

The next couple of years wont be easy for HFC, NBFC, MFC, Consumption related theme.

Under housing for all initiative: If your loan amount is less than 6lacs EMI gets reduced by 45% and if it is less than 12lacs than by approx 22%… so that is a substantial number for housing push in affordable market.

This is the key trigger… for many cases this would result in rental=EMI and hence push more people towards buying their won house.

aef6047d-21c9-4f3e-810f-bb10029b1be4.pdf (986.0 KB)

Q4 & fy17 results

Seems like they are providing Zero % EMI scheme to attract the customers.

Isn’t it true that at the end of the day there must be some earnings?

How do they make money?

It looks like the 0% financing for Consumer durables is the price they pay for Customer acquisition. Once they have the customer they should be able to sell their other loan products like auto, housing, personal loan etc. which might be lucrative. Not bad actually since you would have the profile of the Customer with his spending habits and repayment capacity.

The business model is simple. They take money from the manufacturer/dealer.

If you purchased a TV from a dealer at 40k using Bajaj Finance 0% EMI, you would just be charged a nominal processing fee. The dealer on the other hand would be paying Bajaj an amount ( 1-2k) and still make decent profits (4-6k).

The beauty is that everyone wins in this scheme. Customer feels that he got a great deal, dealer gets his profit share and Bajaj get their due as well.

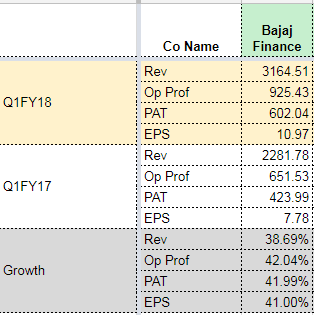

Q1FY18 Results - Splendid results again.

Highlights for the quarter

• Customer franchise as of 30 Jun 2017 up 26% to 21.69 million from 17.18 million as of 30 Jun 2016. During the quarter, the company acquired 1.56 MM new customers

• New loans booked during Q1 FY18 up 48% to 37,71,392 from 25,40,540 in Q1 FY17

• AUM as of 30 Jun 2017 was up 39% to ₹ 68,883 Crs from ₹ 49,608 Crs as of 30 Jun 2016. AUM as of 30 Jun 2017 Includes 2,021 Crore of IPO financing. Adjusted for this AUM would have grown by 35%

• Total income for Q1 FY18 up 39% to ₹ 3,165 Crs from ₹ 2,282 Crs in Q1 FY17

• Loan losses and provisions for Q1 FY18 were ₹ 286 Crs as against ₹ 180 Crs in Q1 FY17. During the quarter, the company took an additional charge of ₹ 42 Crs across its consumer and infrastructure finance businesses. Adjusted for this additional charge loan loss & provisions were ₹ 244 Crs, and have grown 36%.

• Profit after tax for Q1 FY18 up 42% to ₹ 602 Crs from ₹ 424 Crs in Q1 FY17

• Return on Assets and Return on Equity for Q1 FY18 were 1.0% and 6.1% respectively

• Gross NPA and Net NPA as of 30 Jun 2017 stood at 1.70% and 0.53% respectively. The provisioning coverage ratio stood at 69% as of 30 Jun 2017. During the quarter, as required by RBI guidelines, the company has moved its NPA recognition policy from 120 days overdue to 90 days overdue. The comparable GNPA and NNPA at 120 days overdue stood at 1.44% and NNPA of 0.42% as of 30 Jun 2017 vs GNPA 1.47% & NNPA of 0.41% as of 30th June 2016

• Capital adequacy ratio (including Tier II capital) as of 30 Jun 2017 stood at 20.15%. Tier I capital stood at 14.20%. During the quarter, the company raised ₹ 600 Crs by way of Tier II bonds to augment its capital base.

• Deposit book crossed a milestone of ₹ 5,000 crore and stood at ₹ 5,095 crore as of 30 June 2017 – at 10% of BFL’s overall borrowings book. Retail deposit average size is at 2.93 lacs with weighted tenor of 33 months

• During the quarter, the Company received AAA rating from ICRA. The company has now AAA rating from CRISIL, ICRA, CARE & India Ratings

• During the quarter, the Company’s operations have been certified with CMMi SVC Level 3 (CMMi for Services). Capability Maturity Model Integration (CMMi) is best practice model for operations which has been developed by Carnegie Mellon University (USA) and administered by CMMi institute (USA)

• The Company has been ranked as one of the “Best Company to Work for” in India, for the fifth year in a row by Great Places to Work Institute.

• The Board of Directors has approved, subject to the approval of shareholders, issue of securities for an aggregate amount up to ₹ 4,500 crore through Qualified Institutional Placement to Qualified Institutional Buyers in accordance with SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009

Sadly these guys are also now issuing equity to raise money. Everyone can’t be Gruh

Kanv

All finance companies need to raise money from time to time, specially those who are growing fast. Raising money at high P/B (>8.5) is actually helpful from the companies perspective where they get the raw material (cash) cheaply from the market.

But if PAT growth is equal to or more than loan book growth then why would you need it if the leverage remains the same?

(PAT+Accumulated Earnings-Dividend)*(Leverage) == loan Book

I am assuming ROE to remain same.

Correct me if I am wrong.

This is surprising as Sanjiv Bajaj recently said they may not need capital until 2018.

They probably grew faster than their estimates so raising capital sooner than estimated.

Please listen to today’s call. Also it will be good if you somebody can throw light on BFL 2.0. It seems, it was discussed in AGM. It is about 15 areas and 7 themes

Some big but honest statements from Rajiv Jain, CEO, Bajaj Finance during concall on 19-Jul, just reveal how significant is the business momentum on the ground that it is taking the management itself by surprise:

“What we are learning is that consumer businesses are very difficult to build but once they are built they reach an inflection point from where they get into a very different orbit. That really is my assessment in hindsight and I must be honest about it.”

“Retail EMI & Ecommerce is the biggest opportunity that we see. It’s now beginning to gain momentum. I foresee that Diwali qtr will be a big qtr for this biz. It will break even in 3rd qtr and as I was saying earlier that once these things breakeven they just hit a very different orbit. So that’s really what we are banking on.”

There were many other statements but listening is more delightful Go listen.

Cheers

RR

For an NBFC, it’s better to raise capital when market is offering it to you at high PBV. When you need it, market conditions may not be favorable.

This happened with Yes Bank in 2012-14 period. It needed capital to sustain growth but market conditions did not allow it to raise equity at high PBV. Growth eventually slowed down from 30+ to 10-12%. It finally managed to do a QIP in 2014 and growth rate has been back to 30%.

It’s rival IndusInd Bank on the other hand raised funds on time and 25% growth rate never faltered in 2010-2017 period.

better than gruh for last few years, lot of products, versatile

ICICI to offer loans up-to 15lakhs via ATM. Stocks are costly, market is up, loans are on platter. Start of bubble. My 2 cents.

Disc; Not invested

I am not sure at all. ICICI has become much more circumspect about their lending these days. Gone are the Kamath days of mindless lending. I am sure not every customer will get the loan from the ATM. Only qualified ones can apply from loans through an ATM. It is just another channel to reach the target client. Today when a client logs into netbanking, they are offered loans based on their profile, same would be the case here.

What I got from concall, NBFC financing is not an easy business, it took BFIN 10 years to perfect the model of Auto Financing and 4 years for e-Commerce and digital financing.

Also to them there is nothing called Secured and Non-Secured. This kind of confidence can be achieved provided you know, your technological model and internal regulatory model are robust enough to minimize the human factors

Hello Ashu

Just to look at it from a different angle and to add to Abhishek’s point.

Banks give loans to customers if they are credit worthy, that’s the tenet. Servicing a customer is costliest at the branch, cheaper at the ATM and the cheapest on his mobile phone.

Every bank’s intent or rather a utopian goal is to shut down branches and have everything done via phone. This if it actually works out is better for the company as it reduces considerable costs.

Rgds

DV

Friends I said start of bubble, not a bubble yet. Even in USA they have safeguards, but still housing bubble burst. Problem is easy availability of money.