We all understand that this is a robust business. But, how do we justify the valuations?

On a P/B, and P/E basis it looks expensive, and a lot of growth has been factored in.

For me, the only reason to stay still with the stock is the NIMs and RoAs. Infact, that’s what they said at the AGM; that they focus on RoAs. Any thoughts?

2 Likes

BFL gets into payments through mobikwik. The co has entered into a Subscription Agreement with One MobiKwik Systems Private Limited (‘MobiKwik’) for acquisition of 10 Equity shares and 271,050 compulsory convertible preference shares (CCPS). Post conversion of CCPS, the Company would hold approximately 10.83% of equity in MobiKwik on a fully diluted basis. The value of the transaction envisaged is approximately 225 cr.

http://www.bseindia.com/corporates/ann.aspx?scrip=500034&dur=A&expandable=0

5 Likes

Basant Maheshwari discloses that he is invested into Bajaj Finance.

1 Like

Hi…when he discloses this…recently?

Last appearance on ET Now.

no i feel long back in April he disclosed it. check https://www.youtube.com/watch?v=MaIOuRvlcb0

1 Like

may be. what i am mentioning is not first but latest disclosure.

PAT growth cannot be more than ROE assuming constant leverage. If it is as in this case, they need to raise capital once they hit the leverage limits.

1 Like

They are already raising 4500 cr through QIP at 1690 per share

Two positive news from Bajaj Finance today :

The company is moving agressively ahead.

Disc : Invested.

2 Likes

Hi -

I have recently started understanding and valuing finance companies. One of the contender for me was Bajaj Finance Limited.

The key takeaway for me from the analysis was that BFL is running at ~11 times the book value. The RoNW is ~20%, which lefts me with ~2% return on my investment Y-o-Y.

However, I feel that my return would come from appreciation of share price in the future, which will be dependent on the BV it can achieve, and the P/BV it will command in the market.

Two Questions, if anyone can help with this:

-

Is 11 P/BV sustainable? Looking at other NBFCs, typically the range lies from 3-5 P/BV. So, is it fair to assume that 3-4 years down the line, BFL will also rationalize around the same value?

-

Growth in book value of 20% (as seen in last 5 years) seems sustainable, given the growth and diversification of products they are maintaining. Is my assessment correct?

If both of the points are taken together, the share price 5 years down the line is ~2200, which is not much upside?

Please suggest errors in my analysis, as it seems to be one of the best stocks in NBFC space.

Hi ,

wanted to understand the calculation behind ~2 % return on investment, if you can please elaborate the calculation

Regards

Hi,

The return on net worth is 20%, which translates to 33 Rs EPS on book value of 176.

However, when I buy BFL, I am buying the book of 176 Rs at Rs 1953. In its current form, without taking growth into account, I earn 33 Rs on Rs 1953, which is ~2%.

2 Likes

Hi Nikhil,

I think the latest BV is 275 and previous year BV is 175.

PBV is 7-8.

Definitely at a high premium.

Regards,

prasad.

1 Like

Sorry, I did my analysis from 2017 annual report.

Stand corrected.

1 Like

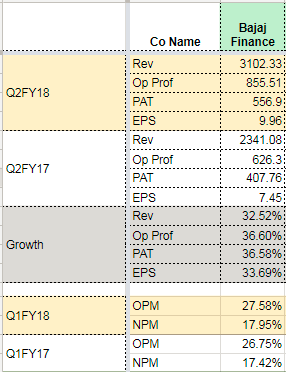

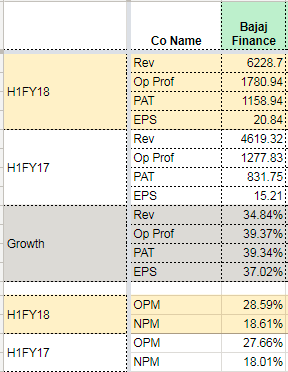

Q2 Results out. Strong results once again.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/fcb210ff-dda4-4b27-9e9e-65b8367fba2b.pdf

7 Likes

did we get answer for your question ?

not yet.

My basic contention is that although it is a rockstar company, current valuations offer 10-15% return over a 5 year period.

Will request to have a look at Q2 concall script before taking call on Growth. Only thing I can comment, this is on different league in terms of Process, People, Technology and finally execution and vision for the same

Important points from investor presentation:

• Customer franchise as of 30 Sep 2017 up 28% to 22.99 MM from 18.0 MM as of 30 Sep 2016. During the quarter, the company acquired 1.32 MM new customers

• New loans booked during Q2 FY18 up 48% to 3,231,078 from 2,176,798 in Q2 FY17

• AUM as of 30 Sep 2017 was up 38% to ₹ 72,139 crore from ₹ 52,332 crore as of 30 Sep 2016.

• Loan losses and provisions for Q2 FY18 up 38% were ₹ 228 crore as against ₹ 165 crore in Q2 FY17.

• Return on Assets and Return on Equity for Q2 FY18 were 0.8% and 4.4% respectively

• Gross NPA and Net NPA as of 30 Sep 2017 stood at 1.68% and 0.51% respectively. The provisioning coverage ratio stood at 70% as of 30 Sep 2017. The Company continues to provide for loan losses in excess of RBI requirements.

As required by RBI guidelines, the Company has moved its NPA recognition policy from 4 months overdue to 3 months overdue in this financial year. The comparable Gross and Net NPA at 4 months overdue stood at 1.44% and 0.40% respectively as against 1.58% and 0.43% respectively as of 30 Sep 2016.

• Capital adequacy ratio (including Tier-II capital) as of 30 Sep 2017 stood at 25.42%. The Tier-I capital stood at 19.86%. During the quarter, the Company has raised ₹ 4,500 crore by way of equity capital through Qualified Institutions Placement (QIP).

• Deposit book stood at ₹ 5,517 crore as of 30 Sep 2017 at 10% of overall borrowings book.

• The Company has entered into an agreement with One Mobikwik Systems Private Limited (“Mobikwik”) on 8 August 2017, and has invested an amount of ₹ 225 crore in the equity shares and cumulative compulsorily convertible preference shares of Mobikwik.

8 Likes