Here is a screenshot from a twitter share thanks to contrarianeps and krunalpatel111. Anyone invested should at-least sit down and think it through. A quarterly eps of 3 (annualize it) and price above 1200. Rationality seems to have taken a massive back seat in hopes of a bright future. My objective is only for anyone invested here to think this through very very hard.

To make the discussion little bit more objective, I ran a simple exit multiple model. Hopefully, this shall throw some light on how much growth is already built-in in the Dmart price already:

Using some broad numbers: CMP: 1200Rs, annualized EPS using latest quarterly results: 12Rs, so investment PE becomes 100.

Result:

In summary, an investor who wants to enter the script at CMP, should evaluate first whether Dmart can grow its EPS this high (26% plus CAGR), for next ten years? Or, the investor has to reduce his/her return expectations.

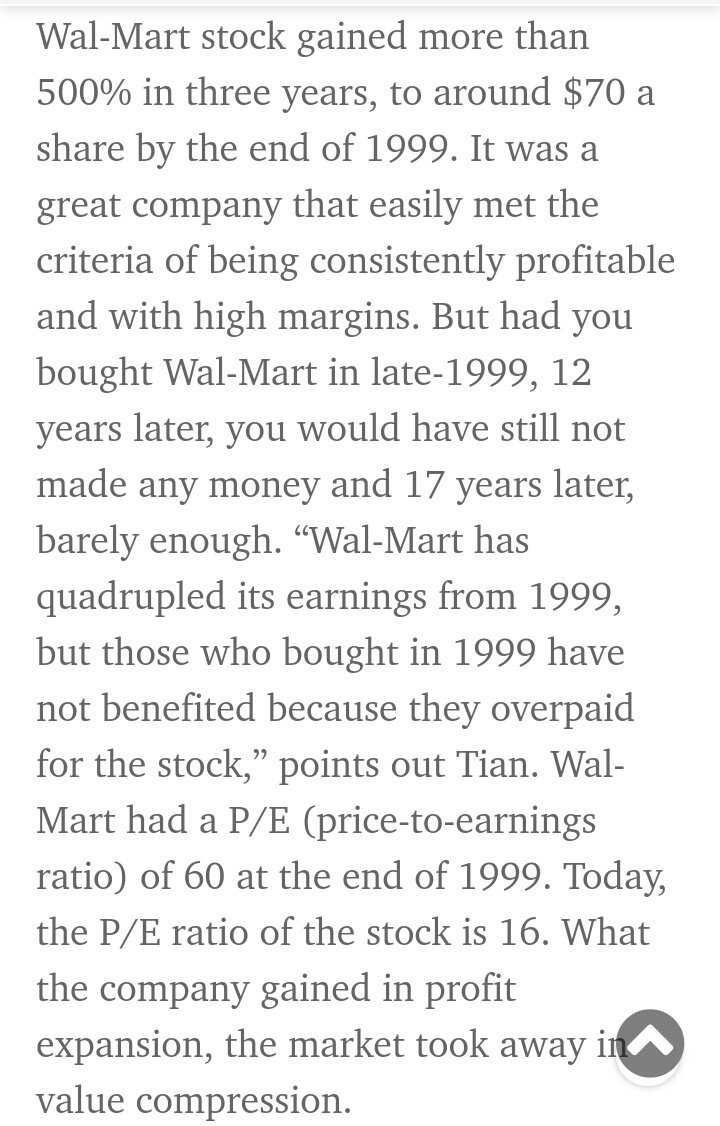

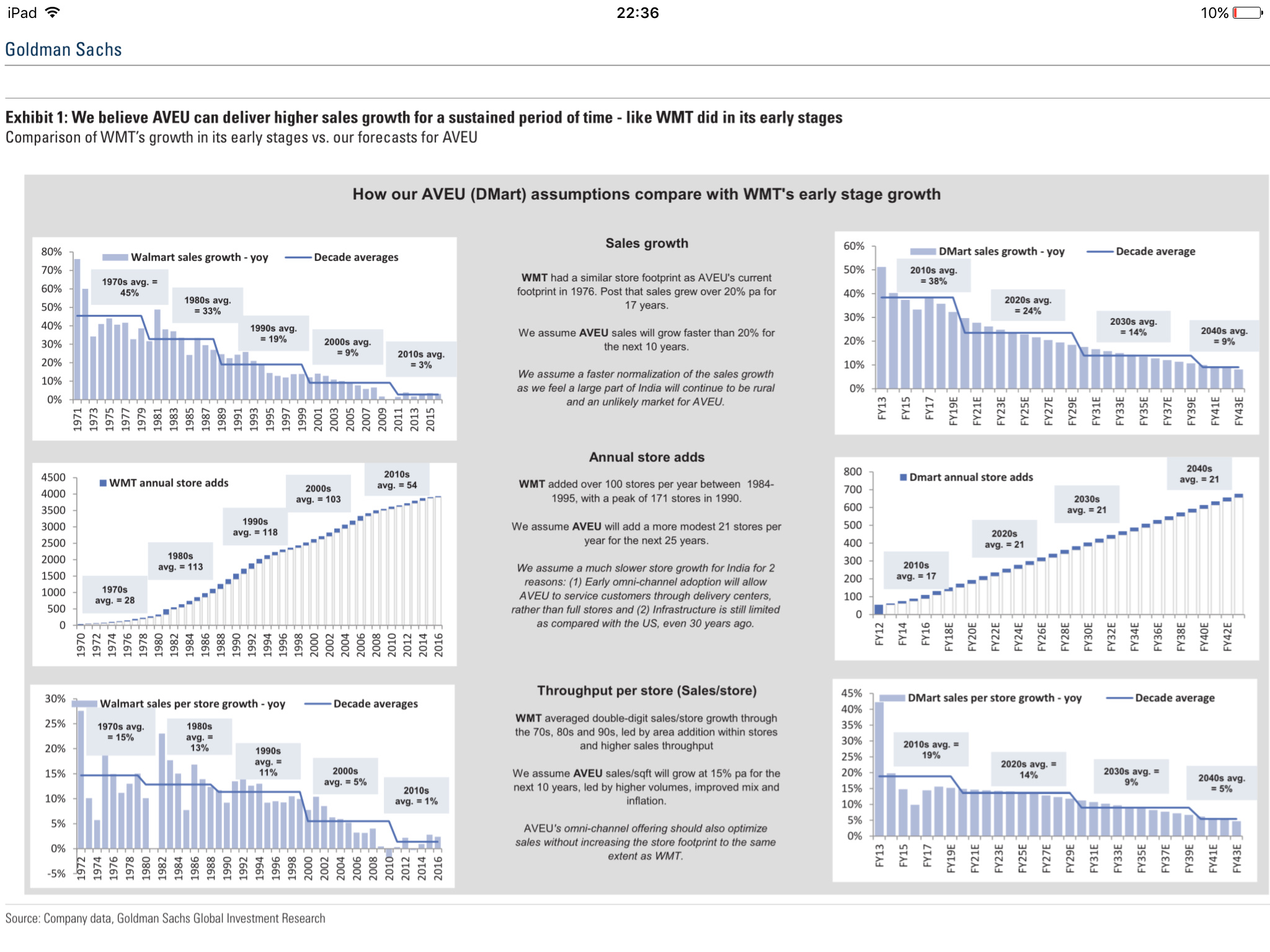

This is not a fair like to like comparison. Please see the attached pic which was extracted from the latest report published by GS. DMart today is in the same position as Walmart was in 1970s immediately after they got listed and had 136 stores in 1976. From 1976 till 1999 Walmart grew at an avg. rate of 22-25% CAGR in sales and also stock price. In fact this was the period which Mr. Buffet missed investing into in 1983 which he calls thumbsucking and the stock later grew 35 times from his purchase price of $ 23 per share.

As rightly said by you, if one analyses the article in detail para by para, one can easily figure out the lack of clarity and long term focus of Kishore Biyani especially when he says he is not sure how Big Bazzar will be positioned and they will decide in due course. No belief in online model whereas DMart is already present into online commerce and home delivery understanding the importance of Omni channel presence. Last but not the least as Peter Lynch says if your competitor praises your company go head and buy the stock. It is an indication that you are doing something right. Biyani knows that DMart’s positioning is such that it cannot compete with it head on in discount retailing.

Thanks Bheeshma. Enjoyed reading your views too especially on the correlation b/w surplus area and population density of each state. I never looked at it from this perspective. Another reason why I feel DMart has a hidden moat is their corporate culture. Culture is so fundamental to any company. Though it is not visible to external stakeholders, it’s presence or lack of it can make or break a company. ASL in my view has a culture of encouraging meritocracy, delegation of authority and extreme customer focus. It reminds as if I am reading one of the chapters from William Thorndike’s book ‘The Outsiders’ wherein RKD is the chief capital allocator and Neville is that hands on CEO which focuses on generating CFO profitably and sustainably. In the near term, all the CFO will be deployed for internal capex and once the company starts generating FCF, then the role of RKD will come into play. And given the management pedigree, I am convinced that if they do not find attractive ROIC opportunities, they will not shy away in distributing cash to minority shareholders. In short, for the next 7-10 years, one can expect a stable 18-20% CAGR from IPO Day 1 listing levels and once growth slows down, it will become a Dividend Aristocrat.

At what time does one reckon that Avenue will become a 50 PE stock? Till when does one expect it to trade at a multiple of 100? Is there any 1 other stock that has stayed for 4-5 years at a multiple of 100?

Reson for the question is: Lets say in 3-4 years the annual EPS goes to 24 (growing at 4 Rs per year).

2017-2018 EPS run rate: 12-13

2018-2019 EPS run rate: 16-17

2019-2020 EPS run rate: 20-22

2020-2021 EPS run rate: 24-26

So within 4 years the profit would have doubled. What is the possibility that the PE towards this time would contract to at-least 50 if not 20-30-40. Then the stock price would still be around the same levels as it is today. Maybe 100-200 Rs here and there.

It is none of my business but are some members here not overly bullish? I am simple playing devils advocate for some of you to think about it. Nothing in it for me.

Also, lets think about the market cap. Today the market cap of Avenue is at 77,027 Crores. For the stock price to just double would need the market cap to go to 150K crores. How many companies in India at over 150K mcap? How many employees in those companies and how irreplaceable are they compared to a supermarket?

If these seem viable, you are on the right track else, some bias may be in play. If you sold the stock tomorrow, would you buy it day after?

This is a great company, but looks like currently at a great price as well. Also, Avenue is no Walmart. I am sure many of you have seen Walmart. This is a pure play supermarket. Is it not India’s Walmart or something.

I think due to good results there may be a spike for the short term. Don’t know if they beat the consensus.

Everyone should have a view on valuation and here are my views -

I have taken a PE exit multiple of 20 after 30 years and assumed an average growth of 15% over a 30 year period. I think one can take a 30 yr time horizon in this case but such long horizons are not suitable for a majority of investments. These views are based on my subjective assessment of the sustainability of the supermarket format in India where D-mart has a clear headstart.

This is also a winner-take-all situation where a product or service which is only slightly (1%) better then the competitors gets a disproptionately large (90%-100%) share of or all revenues for that class of products or services. These situations are often found in retailing but at a local level.

This situation is found in real estate very often where a project that is only slightly better compared to other projects in that location gets all the customers. However unfortunately for real estate - it is not sustainable as the next project may not have these characteristics. The continuity is missing in real estate else it would also become like that.

Coming back, I am not saying that this is a 100% winner take all situation but it certainly has that flavour. This is the reason for taking an average EPS growth of 15% over a 30 yr period.

Another thing that is also worth looking into is the consumer behavior aspect - once a buying pattern is established and a perception of low prices is formed it is difficult to dislodge this perception. The demographic that DMart caters to are characterised by frugality and when frugality meets low prices in a winner take all situation one can expect sustainability extending long into the future. I also think that the housing for all mission will be a great thing for Dmart as population distribution patterns are going to change with this initiative creating favorable conditions for Dmart.

In my opinion looking at prevailing PE ratios is not suitable in situations such as this which are sustainable for a long period of time.

These are my views and i am not invested in Dmart.

Well said. I agree with the assessment that this can be a buy and forget stock with a long horizon like 20-30 years and will have a formidable lead in the years to come.

This looks like a stock only for investors who can stay here for 20-30 years (and not for next 1-3-5 years), and then it probably is one of the better bets in town.

Could be a good 24-36 month SIP candidate to flatten any price fluctuations during entry, and then a life long hold to retirement.

Walmart currently trades at a mcap of $260 billion. Dmart’s current mcap is $12 billion. Let’s assume that Dmart will achieve the status of Walmart after 30 years. So its mcap will grow from $12 billion to $260 billion(or 22 times) in 30 years. This is an annualised growth rate of mere 11%. Don’t forget that there was no Amazon in 1970s. I think we’re taking Amazon too lightly whose equity investment is several times the net worth of Dmart.

Just to add… Walmart had ample time to grow without the e-commerce challenge… The way India is getting digitized… And the rapidly changing digital way of doing things entering our lives… This was not the case in US

India is in a FastTrack mode to adopt digitization… We don’t have the luxury what the US Walmart and others had… Which was a long time they got before the onslaught from online digital channels… Hence Indian companies need to be viewed and assessed factoring this crucial point…

Note that all e-commerce players are in losses and they are surviving because of big discounts they give. Example: I am a regular user of Amazon super saver, weekend 10-15% off etc for household items as these prices cannot be matched by retailers nearby. However, recently I noticed they started increasing prices of few items on weekend - so I stopped buying those. In short, it may not be easy for these e-comm players to earn profit as well as give low prices at same time. Also, not everyone will shop online.

Different views makes a market and completely respect the opinion of others. It will be an interesting scene to watch over the next 3-5 years as to how this entire online vs. B&M retail plays out. My opinions may be biased in favour of ASL since I am invested from Day 1 listing levels and do not support entering at current levels as there is hardly any margin of safety available. Even assuming that DMart after 10years generates sufficient FCF to pay a 2% dividend yield, in my view the dividend yield for this stock will set the exit multiple floor much is the case with all matured MNC FMCG cos. Whose earnings continue to grow b/w 10%-15% p.a. but have a P/E b/w 35 and 50. A’s Howard Marks says, Experience is what I got when I did not get what I wanted. I am sure it will be a costly experience for me if this stock does not generate the returns I am expecting but I do not want to miss to ride this horse and open to a less than benchmark return. At least it will not be a quality trap and permanent loss of capital is protected.

When comparing one retailer with another in a different geographical zone one should also keep in mind the population characteristics. These are important variables and help to calibrate views. For e.g India is 4 times bigger than US in terms of population and theoretically can house 4 walmarts. Also India is 10 years younger than US in terms of average age with a signifantly higher population density.

The per capita income and poverty situation also differs vastly.

One can only speculate on the market cap of WalMart if it had been serving a population of 1.3 billion instead of 315 mil offering low prices to a largely poor but very young population. These comparisons are at best of mild academic interest and in my view cannot form the core of the investment thesis.

Best and as always eager to hear contrary views

Bheeshma

Congrats on buying in day one. While it is high probability that your capital is safe, itisnot certain at these levels. Years of high growth has been built in to the price. Any disappointment could easily take the prices down. I still cannot understand why the market falls so much in love with some stocks although not all perform to their name like Jubilant Foodwoeks and Dish TV for example.

This is my first post in the forum.

I have often heard of the high population in India mentioned as one of the reasons why companies like in the FMCG domain as an example will grow several times. However, are we not making an implicit assumption then that all of these young people in our country will have well paying jobs which will lead them to upscale and buy such products. That I feel is a big “if” as I think that squeezing in 1.5 billion people approximately (our last count was 1.2 in 2011 and I assuming very low growth) in a small geography like our’s will create more issues than nought. Just my 2 cents.

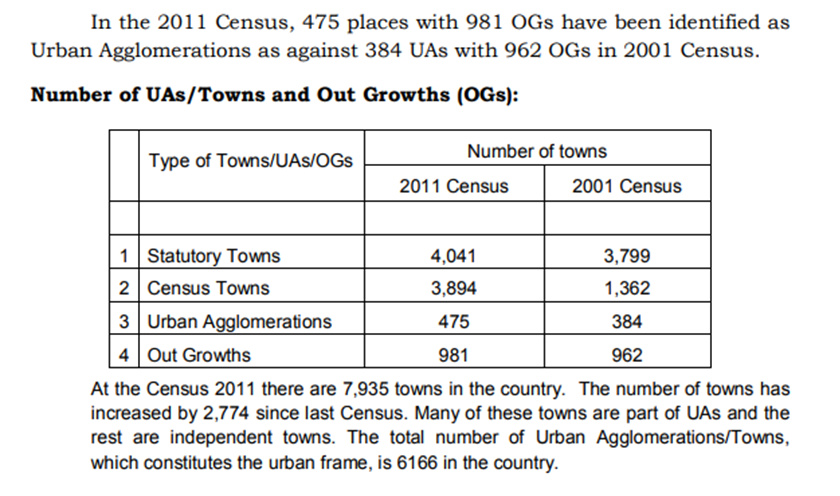

As you can see the number of UAs has increased from 384 in 2001 to 475 in 2011 - a growth of ~24% indicating new urban areas being formed continuously.There is more to the D-Mart story than meets the eye and it is worth digging further.

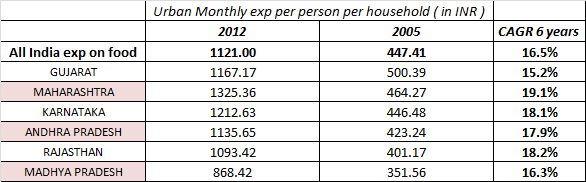

Another very useful table from the NSSO database. They conduct a survey on the monthly household exp per head across india called the “Household Consumption of Various Goods and Services in India”

Clearly, expenditure on grocery has grown across india at an average growth rate of 16.5% with all the states that Dmart is present displaying strong numbers