While analyzing population demographics, the contrast in population density of western countries compared to India may actually work against Indian retailers. In India, the population density is way higher at 1,042/sq. mile ranking it 8th among the most populous countries in the world, compared to US with pop. density of 86/sq. mile ranked 79 (source: UNDESA). A concentrated population base around urban centers in western countries makes it much easier for retail giants to cater to the large sections of the population by opening 2-3 giant stores which themselves become the urban population hubs for these cities… However, in a country like India, a retail chain will have to open countless number of stores to cater to even a fraction of the total population.

Also, the mom and pop store culture seems to be re-organizing at the local level in India with many small players upgrading themselves into mini superstores denting the large superstores’ market-share. Infact, I shifted from Grofers to Vishal Megamart first for all my groceries due to proximity. And now recently I have shifted to another local mini-store which is run by 4-5 young lads but is even closer to my residence. They deliver same quality product within an hour, without a minimum basket size, and are very accurate with their delivery. Their offers are quite reasonable and I don’t feel the need to go to any superstore for household items. And a few days back another similar store came up in my vicinity named ROC (Round o Clock). Their proposition is that they are delivering 24x7. These are some unknown stores with good value proposition for someone like me and I feel the giant stores sales would get needled by these local stores severely in coming years.

And as digital India progresses, road connectivity improves and logistical supply chains become more efficient, e-commerce will penetrate much faster than the brick and mortar players. The CAPEX required to cater to the huge population (which we see as an opportunity) would be almost impossible for B&M retailers, not to mention the complexities involved in doing business in semi-urban centers beyond metros and state capitals. At the same time, the e-commerce players will enjoy the government’s infra expenditure on roads and internet penetration, as they build a business around it with much higher capital efficiency.

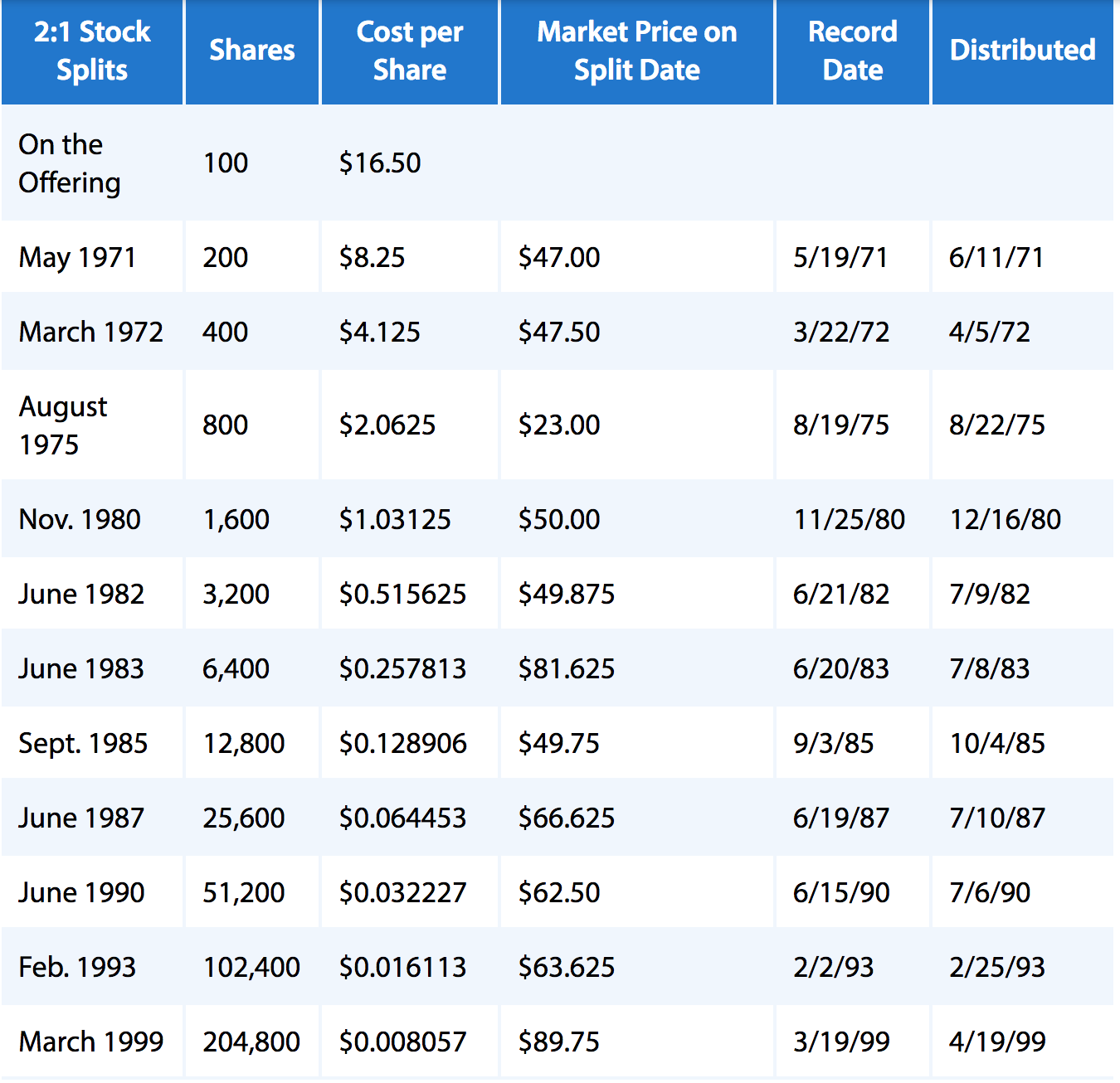

ASL is overvalued and most of us are counting upon its future growth to bridge the steep valuations. I am quite sure that its a risky bet for next 3-5 years as it may take longer than that to rationalize from current levels. But even if we are thinking with horizons of 20-30 years, is it even possible to factor in all major variables which can have an impact on its business for decades to come? I feel its a long shot and can be avoided unless it corrects and gives a significantly better entry point in near future.

Disc - Not invested