Hi @Akhil_7306

Disc - i am neither invested in Dmart or Infosys

However, in my opinion , it would be unwise to look at historical growth rates extending too far back into the past. As long as Infy was expected to grow at 25% - 30% + , it commanded the valuations it commanded. Over time mgt has given a lower guidance and the prices have adjusted to this. The numbers also have reflected this. In the last 5 years profit growth has been 11.49%, 3 yrs - 10.44%, the recent yr - 6.4% & the recent june qtr - 1.4%.

When earnings are expected to grow at a rate than is significantly less than the long term inflation rate , the PE ratio has a tendency to remain very low even for companies with a strong balance sheet and lots of cash flows in stark contrast to the teenage version of infy which was doing an earnings multiple of 300. But those were exciting times for the IT sector.

This low PE further creates an optical illusion of value that is incorrect. The flip of course is a company that is expected to grow at rates significantly exceeding the long term inflation rate. These kind of companies have a high PE which again creates an optical illusion of overvaluation.

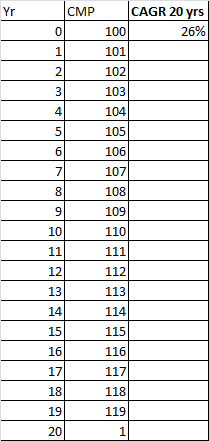

A few years back, i was given an example by an investor on not relying too much on historical growth rates which has stuck with me and is part of my “akal khaata account”. Imagine a company over 20 yrs. This company has grown exponentially only in 1 yr , 20 years ago. In that one year ( 20 years ago) profits grew by 119 times. After that it has been a degrowing every year.

Yet if you do a 20 yr growth rate , the 20 yr CAGR comes to 26% & at that rate it would appear undervalued - again an optical illusion. Obviously, this is an extreme example but it helped me in improving my thought process.

Please take these views as a theory and my personal views. As with all theories they are peppered with my biases that i cant shake despite my best efforts. I acknowledge that. But under the investment process i now follow - i have found better performance in high PE stocks & therefore - unsolicited as they maybe - i have a tendency to share these views spontaneously.

Best

Bheeshma