So Mr. Biyani is saying that he is touching 2 cr. people. And its nothing compared to 130 cr. population of India. That’s misleading! When he is having all his 10,000 stores only in urban bases which are 30-35 percent of country’s population, then an apple to apple comparison would be more suitable.

Mr. Biyani’s strategy has a few merits. More stores means more penetration. How to manage capex? By having exclusive membership of atleast 2000 consumers per store, they would realize Rs. 999 per consumer. That makes it 2000 cr. (10,000 stores X Rs. 1000 X 2000 consumers). He talked about 1000 cr. being spent in technology and rest should go towards real estate expenses. But it would be a gradual process and the company would expand from internal accruals as its first lot of stores gain traction. But the flip side of this strategy is that he is still focused on urban centers making the competition even more intense there. Also, retail has to go massy not classy to succeed. So even Mr. Biyani knows that making it exclusive club memberly is only to get initial capex funding and a loyal set of customers which are going to be a steady market in initial period. Thereafter, it would be made available to all customers, with some free delivery benefits to the members just like Amazon Prime. And they are delivering in 30 minutes approx. with a nice Domino’s touch in it. He just stopped short of calling it ‘30 minutes or free’.

But when I see news reports like the following report from Goldman, my gut feeling says that similar to Telecom, Retail has its greatest opportunity still lying untapped.

Majority of the companies in India neither have the financial muscle nor a winning strategy to penetrate into the unorganized/semi-urban/rural segments. And that is why the much publicized market base of 1.3bn consumers is both grossly under-penetrated and exaggerated. These numbers look good in investment bankers’ reports (on behalf of their clients) to entice investor community to take notice and invest. Because calling it a market is different from classifying it as a target market.

Why only urban population deserves good products/services? Why can’t rural population be made part of the growth story so that their lives can improve too? As humans are they any less deserving than their urban counterparts? These questions are more socially oriented but less favorable to investing community. Because in investing money attracts money. Relax, these are not my questions. They come from the famous book “The Fortune at the Bottom of the Pyramid” by Dr. CK Prahalad. He has talked about innovative business models, products and services which can cater to the needs of the most poor people who lie at the bottom of the pyramid (to improve their living standard), and can still be profitable ventures for investors.

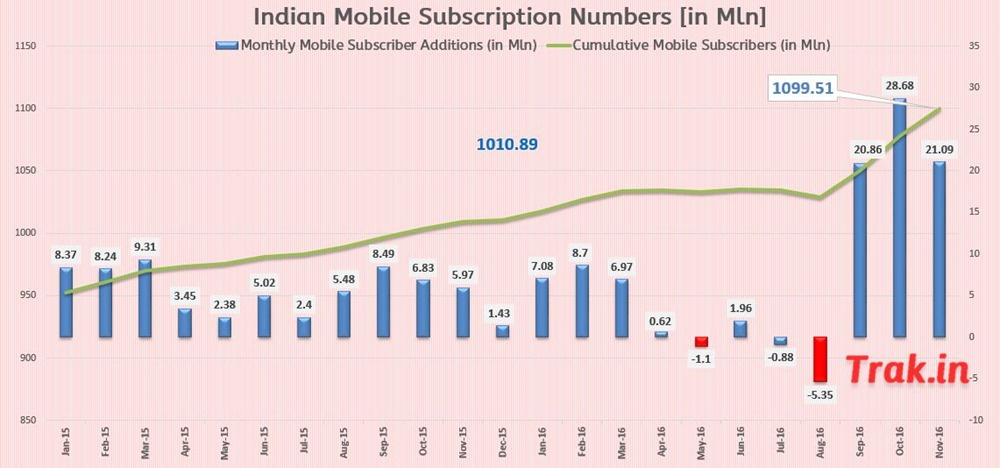

Reliance Jio’s strategy of cracking the rural code in India has unique insights into market penetration. Off course only a company of the size of Reliance or likes have the privelege to spend serious money in developing untapped markets. Today, from a scam plagued background, Telecom is re-emerging and getting a second wave of growth. The best part is that this growth is driven by volumes. The real beneficiary is the customer. It reinforces the belief in the free market where it is possible that sellers may control pricing in the initial part of the industry life cycle. But eventually competition catches up turning it into a buyer’s market. And the life cycles generally are getting shorter by the day making it difficult to control prices for long. In about an year or so Reliance commands a marketshare of nearly double digits in Telecom which is commendable. But what interests me most is the increase in subscribers. Just after three months of launch Jio made a world record of adding 50 million subscribers in 83 days. The overall mobile subscriber base showed unprecedented volumes.

Consider Jio from a rural consumer’s pov. Jio is following a cost leadership strategy where it is selling a service at lowest possible price. BSNL was always there but the services were below standard not creating much value for customers even at its low price point. And let me assure you that a company like Reliance can actually sell a service at a loss for extended periods to kill competition. If someone followed the Jio AGM, they would remember how telecom stocks across the board tanked as Mr. Ambani laid out his strategy of ‘FREE VOICE AND DATA SERVICES’. Its not that Reliance Industries’ stock was rising; it was holding itself without much gains because no investor likes the idea of selling a service for free. Why would Ambani do that? Because a few quarters of losses won’t dent his networth. But companies like Airtel, Voda and Idea began losing subscribers and had to dance to Reliance’s tune. Contrast this strategy with Biyani’s strategy of exclusive membership at a price which surely will make the customer think atleast once - why am I supposed to pay just for having access to a store?

Indians love freebies - all classes. We are not like westerners who feel anything that comes for free is worthless. Could there be a Jio integrated technology which can help deliver groceries free of cost? Only time will tell. After Jio’s success, I am waiting to see Reliance’s grand retail plan unfold which not only will steal marketshare in my opinion but will also target a huge untapped market beyond the urban pockets, which are slowly getting cluttered. The possibilities are endless once you put in the mind and resources to tap into it.

. Always v skeptical of people who talk/boast a lot and keep giving growth guidance. Let your work do the talk.

. Always v skeptical of people who talk/boast a lot and keep giving growth guidance. Let your work do the talk.