I think, the following quote by Benjamin Graham is very relevant here.

“Obvious prospects for physical growth in a business do not translate into obvious profits for investors.”

6 Likes

Ambit never had a view even before the IPO. their IPO note suggested ‘NR’ i.e. NOT RATED, they do not have any forward view on the stock and within 3 quarters of listing they now have a sell call. I admire the contrarian view of Saurabh Mukherjea and his team but most of the time, they end up holding wrong end of the stick.

1 Like

Can anyone share the right calls made by Ambit. Recently they have given a

very positive call on Bhansali Engg Polymer. I hold a good position. Now I

am getting worried !!

If somebody (e.g Ambit) wants to sell his holding they release buy call when all good points are at its best and price also at pick so that new buyers ready to give them good price. See Ambit buy call for Garware wallropes and Bhansali Engineering Polymers Ltd !!

Avenue supermart is a combination of a good business with amazing management, everything is fine apart from the valuations. Whenever the bears will take over, we’ll see the impact on the price.

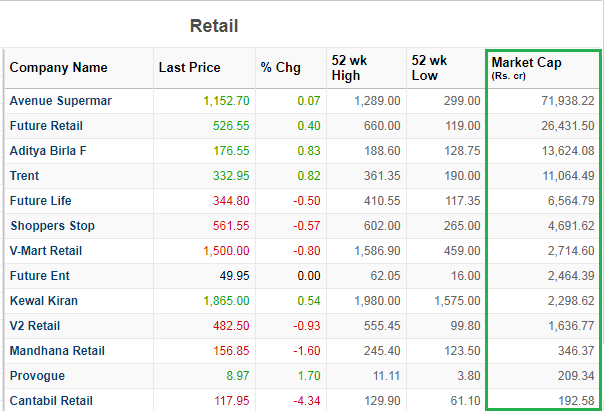

Historically whenever the valuations are so high, either the stock has remained range bound for a prolonged period or the price has gone down. A quick look at the market cap of various companies in retail sector we can easily figure out that valuations are super stretched.

Image Source:- Money Control

I need inputs from people holding it from IPO levels. Are you guys still holding or you feel this is the right time to book profits (as per the valuation parameter) and re-enter again when it is available at lower levels.

Disclaimer:- Partial holding at IPO price (Booked profits at 900 levels)

1 Like

Hi aashu24ahuja, your points raised are supervalid and the table put forth is quite concerning too. I am an investor since IPO levels and have added it up to 660 levels. If the sector leader’s market cap is nearly 3 times that of the closest competitor in the sector, then no room for doubt that the valuations are hyper-stretched at this point. This kind of scenario has happened in industries like telecom in the past, and the consequences were bad for investors holding on to the leader. With Future Retail tweaking and fine tuning its business model, this makes one worried whether despite excellent processes and management in place, DMART would prove to be a moneyspinner for a long time. However, periods of under valuation or over valuation tend to last longer than expected despite warnings of correction and thus confounding the most seasoned experts. So at what point do we call the tipping point and bail out is an open question. My personal metric, however, is when I lose 25% of my notional gain. These kind of companies make us feel good to invest but give sleepless nights about when to sell.

1 Like

A well written report by Amit Keerti merging the fundamental analysis with scuttle butt approach & highlighting Business & Valuation risks. Most of the points discussed and debated above in the forum on Offline vs. Online have also been v well covered.

6 Likes

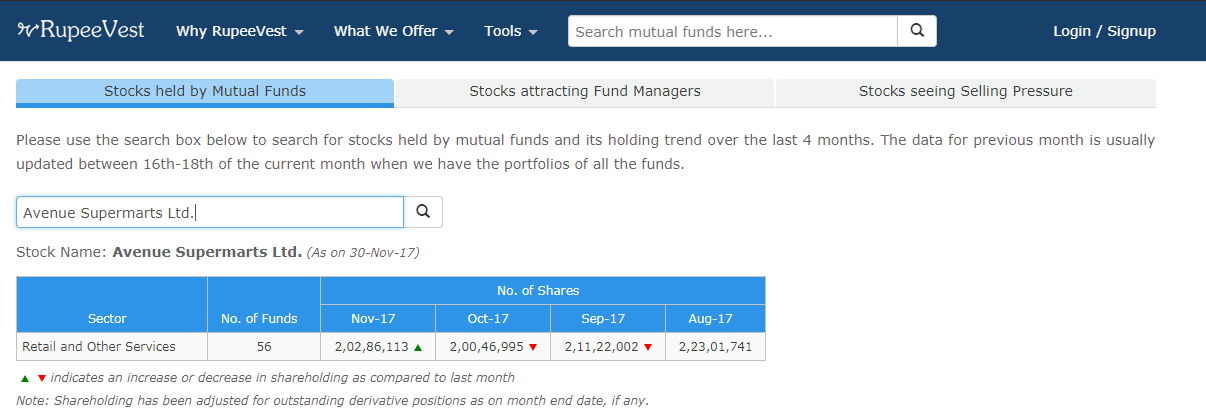

Agree with ashu24ahuja. The valuations are definitely looking stretched. As a result, the mutual fund houses have also trimmed their position a little as compared to 3-4 months ago. The stock could be in for a period of consolidation.

Source: Stocks held by Mutual Funds | Avenue Supermarts Ltd | RupeeVest

Looks like MF holdings are being replaced by FIIs and FPIs if you go through the shareholding pattern for June end and Sep end. It may be worth seeing the trend for Dec end.

1 Like

Some renewed buying interests seen in Dec by DIIs. https://www.rupeevest.com/Mutual-Fund-Holdings/Avenue-Supermarts-Ltd/223595

Fy18 Q3 Numbers: http://www.bseindia.com/xml-data/corpfiling/AttachLive/e3ca2c95-5aaa-4bb8-809f-c3a57a839be0.pdf

paid up capital of Avenue e-commerce is 85.7cr. I think return to the promoters are less than 6% since it was incorporated in Nov - 2014.

1 Like

As per company release, Paid up capital of co is rs 85.7 cr, rs 1.2 cr t/o of 16-17 was from operations started in some locations of mumbai in Dec16

1 Like

Although great businesses do sell at relatively higher P/E and P/B multiples, the stock market systematically underprices quality in the long term. This happens because most investors tend to discount delayed gratification too heavily. A must read by Prof. Sanjay Bakshi.

2 Likes

Thank you very much for the talk delivered by Sanjay Bakshi. Really makes one think harder about selling an extravagantly expensive stock like D-mart. As mentioned before in this thread, buying, holding and selling a company like D-mart are equally tough decisions.

1 Like