Anu update from management/local guys …about impact of Titli cyclone and rain on Aqua culture?

Wheat and Soyabin price will remain strong

https://www.spglobal.com/platts/en/market-insights/latest-news/agriculture/101118-usda-cuts-estimate-for-2018-19-domestic-soybean-production-by-3-million-bushels

This data is wrong.

Avanti sources entire stuff domestically and price is hovering around 28-30 Rs per kg. My comments r based on data only

1 Like

GoI’s MSP for soya is a misincentive (along with China’s decision to cut import duty on Soya imports from India), which I expect to drive more increase in Soya Crop acreage in India. So,I expect soya prices to come down (already down by 25-30% from yearly highs).

6 Likes

I have gone through the above and Avanti Feeds AR. Srinivasa Cystine holds ~27% shares in Avanti Feeds. And hence, for Srinivasa Cystine, Avanti is an associate company ( which srinivasa mentioned in their AR). Avanti does not hold any shares directly in Srinivasa and hence they need not consolidate srinivasa financials. Mr Inderkumar, i guess in his personal capacity holds majority stake in Srinivasa Cystine. Does this address your query?

5 Likes

Friends I am not expecting Q2 to be good one, check this moneycontrol link, though it does not speaks for Q2 nos, but it gives a cautious outlook for the company. https://www.moneycontrol.com/news/business/moneycontrol-research/recovery-not-yet-in-sight-for-avanti-feeds-apex-frozen-foods-waterbase-3059311.html. Happy investing!

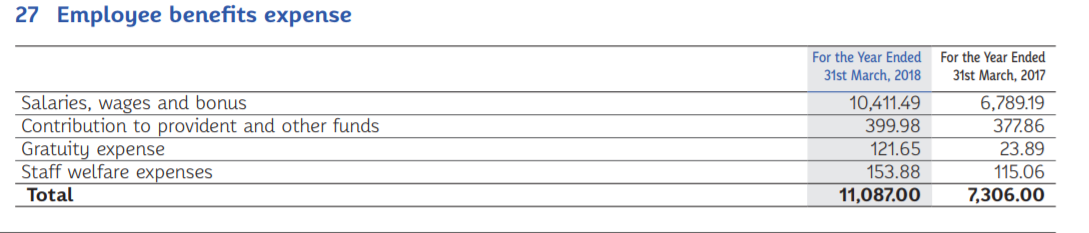

I do not see any increase in employee count. Rather reduced by 100 employees , 1020 in AR18 vs 1100 in AR17

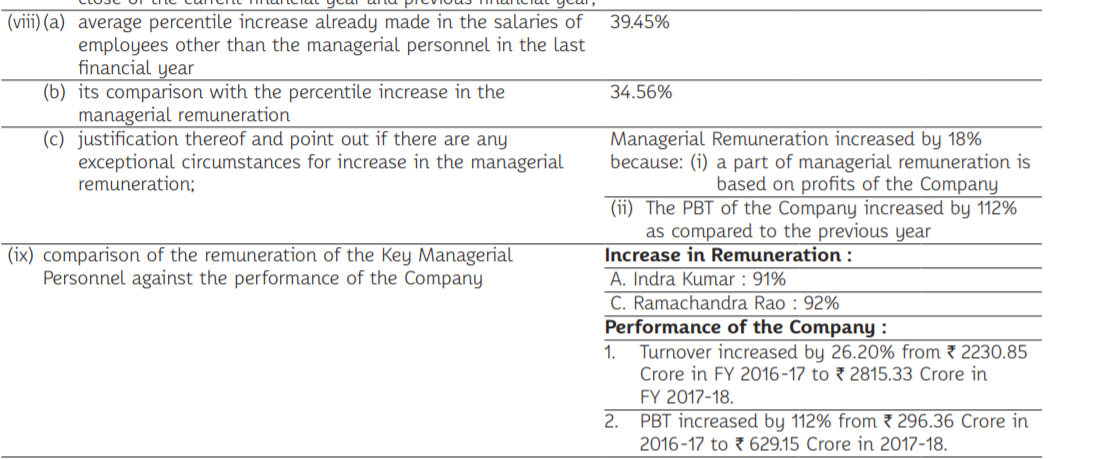

Does Avanti feeds gave 35 percentile increase of salaried ?

MC has taken a crusade to highlight all things negative about the industry.When the valuations are already approx 60% down and PE severly contracted,one wonders how low can it get. Since it started its run,more people have spent time in running it down rather than appreciating how singulalrly these companies have put India on world map.Media needs to excersise utmost restrain unless and until they have solid facts. Though there are thousands of company, MC everymonth comes with one article where the assumption that the shrimp industry is in dire trouble. Shrimp companies are facing multiple challenges but no way are they struggling to survive. Being positive harms no one,unless and until there is a corporate governance issue.Investing is not one way upward journey.

If we are convinced about Avantis potential, such articles which distorts the price downwards is a good opportunity to add or make new buyers come in… That is the nature of markets…

The real damage is done by regulators by arbitrarily changing market cap and MF rules and putting stocks in and out of asm…and that is not the nature of markets…

2 Likes

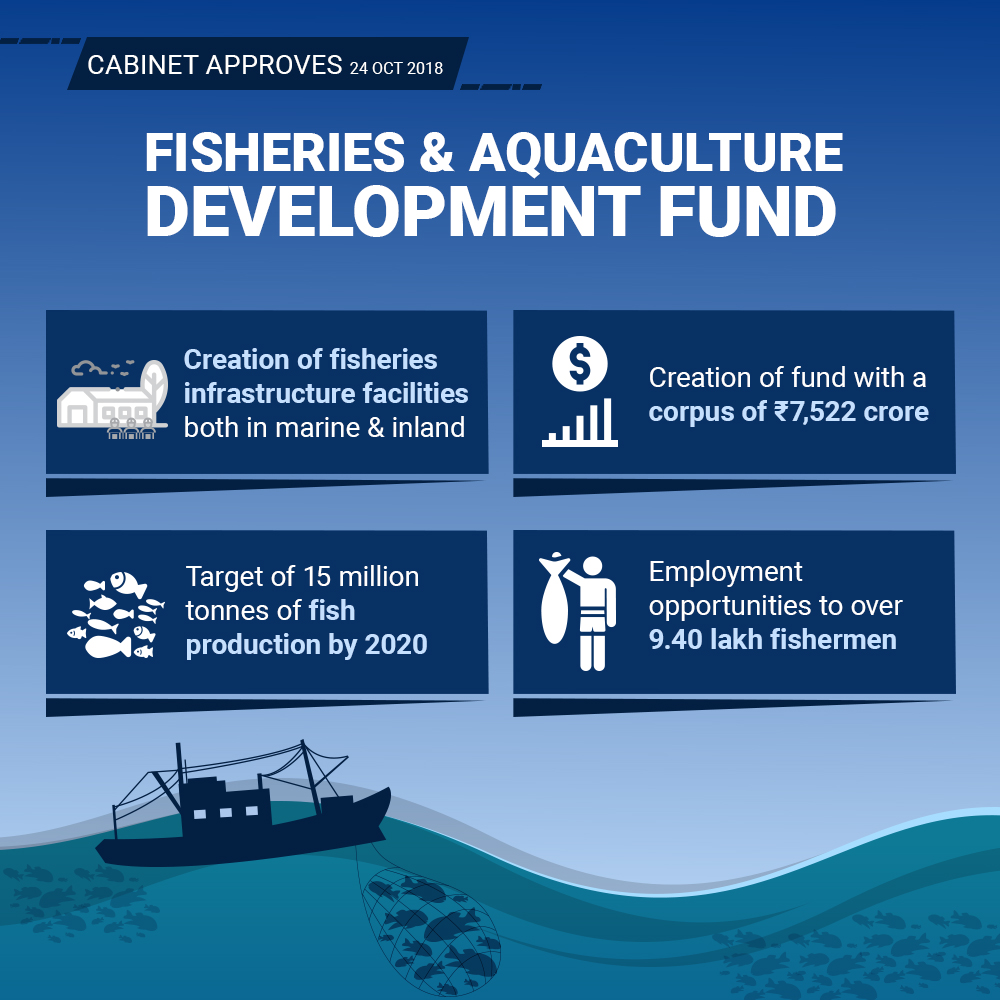

How is this fund going to be beneficial to shrimp industry other than helping in softening of fish meal (RM for shrimp feed) prices a little bit? I feel shrimp farmers do not stand to benefit from the FIDF.

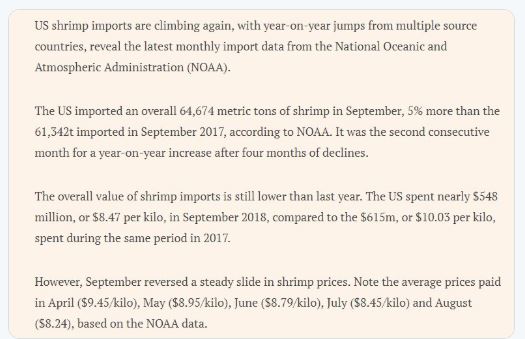

September shrimp export volumes to US from India has shown a growth yoy (14%). I think, for the full year (2018), we may see a marginal growth of ~ (5-10%) over 2017 levels.

Interesting to watch Q2 numbers of Avanti on Nov 10. While, industry headwinds (like lower shrimp prices due to which some farmers stayed away from re harvesting in Q2) were prevalent for most of Q2, INR depreciation and cooling down of raw material prices may partly negate the drop in profits (compared to Q2 2017).

10 Likes

Results look bad on all fronts - Top, bottom, margins, feed segment, processed segment.

Yes the result is bad but what I understand from multiple reports, things are stabilizing

- RM prices are now back to 29-30 level. New crop just arrived in last 2 weeks as I was tracking multiple reports in SM about the price

- Shrimp Price is stabilizing from Sept onwards. We have seen some improvement in volume also

Yeah. Results look bad. Though, things are improving on the ground, as per my expectation, we may not see the immediate impact in Q3 (due to seasonality factor and also Q3 17 being on a higher base). May be, we can expect some change from Q4.

Disc: Invested. Not a buy/sell reco. Pls do your own due diligence

Looking at the gross margin profile after result .Below are observation at consolidated level

Q2 Fy 19 - 22.34%

Q1 Fy 19 - 21.11%

Q2 Fy 18 - 29.52% (exceptional year rm cost was very low)

Q2 Fy 17 - 15.10%

Q2 Fy 16. - 24.13%

Damage alredy done on stock price. Margin getting back slowly.