True… Very bad numbers and no one expected such numbers… Let’s see how Mr. Market reacts…

1 Like

I think Avanti may provide a good opportunity to add after Monday. The question is whether Mr Market has already priced this or not. PE compression of the company happened before the results and now I am expecting earnings compression to happen. As per the information shared by senior members here, looks like the headwinds are already receding and we may not get Avanti at a price of Depressed_Multiple*Depressed_Earning.

Kanv

1 Like

An interesting read about possible red flag in Avanti, https://www.quora.com/Is-Avanti-Feed-good-for-long-term-investment, any opinion about it from the learned members?

2 Likes

The author is a frequent poster here. I wouldn’t assign any more weight to his views than of other members here. P/B has its place in a valuation framework but can fall glaringly short in some situations and contradicting P/B and P/E ratios do not make things any more straightforward.

At the consolidated level in the balance sheet the trade receivables have gone upto 105cr in comparison with 50+cr for the entire FY18, is this something we need to worry about.

Have seen few things mentioned on various social media sites about rise in debt, receivables etc of Avanti. Nothing unusual about it. Domestic business of Avanti ( feed) is mostly cash & carry. So, we will not see much receivables. Coming to exports, there is a lag before Avanti receives payment from end customer. This particular part of receivables is financed through export finance loans from banks ( packing credit loans in banking parlance). Especially, Q2/Q3 being peak season for shrimp exports, we will see rise in working capital loans. These are typically 3-6 month/ low cost loans, generally availed by exporters, and are retired with proceeds received from customer.

Key things we need to dig around and look for answers to my mind are below ( not exhaustive and pls do add)

a) what’s the current on the ground situation w.r.t feed business. Have the farmers, who have stopped temporarily during Q2 returned to farming now?

b) what’s the situation w.r.t raw material and shrimp prices?

c) what’s the situation w.r.t exports by Avanti to Europe and other Asian countries? In the past, there have been news articles about Avanti starting exports to Japan and China? Have they started and what are the current volumes? And after the European audit early this year, what’s the outcome? Have they given selective approvals and is Avanti exporting to EU?

d) shrimp processing segment- current utilization levels and when do they expect to see higher utilization levels.

Was thinking, may be if we could do a VP member Q& A with management, like done in the past would give us more flavor? Most of the time in concall is wasted asking about next quarter targets etc. Would love to hear others.

11 Likes

waterbase delivers much better margins than Avanti feeds.

waterbase has delivered gross margins of 33 % vs Avanti 's 23%.

this is surprising given the fact Avanti claims its product to be better than peers.

seems like Avanti had to drop its prices to support the farmers , if we can get the volume data from the management we can understand the situation better.

it is also frustating to see Avantis management has no use of cash and it is just lying in mutual funds( 700 cr!). Management also does not see value in the stock inspite of the great correction in the share price , otherwise could have easily thought of doing buybacks with such great balance sheets. the way they take exorbitant salaries from the company also shows the attitude of the management is not to create shareholder value but rather satisfy their greed.Just because the RM prices had declined the management believed they should suddenly double their salaries ,even though there was no change in the underlying fundamentals or the manner in which business was conducted.

Avanti feeds has been a great lesson for me in terms of knowing when to exit a stock. When a commodity business , with greedy management starts doing well and is trading at exorbitant valuations its time to exit the stock.

Disc- Invested

5 Likes

W.r.t waterbase performance, we also need to consider their Balance Sheet. There is a surge in their receivables which clearly explains their growth in sales. For Avanti (standalone), receivables are less than 10% of total sales. where as for water base its more than 150% of their total quarterly sales. There would have been extension of credit period by waterbase to farmers which could have resulted in the surge where as Avanti’s majority sales are cash & carry. And with increase in topline, your margins also look better. During tougher times like these, credit sales might even result in bad debts.

10 Likes

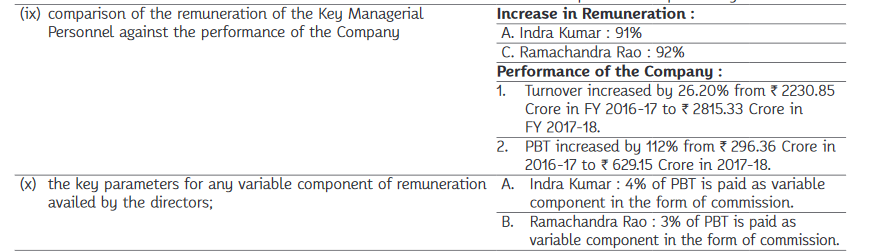

![]()

Source: Annual Report 2017-18, Page 44

The salary of the management is linked with profits and IMHO that is the best way. I really do not feel that management is greedy… Rather, I feel they are very genuine. Whatever targets they have given before they have achieved. Also, they have been saying that PY (2017-18) Margins were not sustainable. They have been giving a a lower guidance since long. If we take excel and project last year results as a longterm indication of times to come, it is not their fault.

Also, waterbase numbers include one time income of Rs. 3.54 cr

To compare the results you need to exclude the impact of this income also.

Disc: Invested.

9 Likes

Have you checked with the management if they discount their receivables?

In case they discount their receivables and convert them to cash immediately, you will never see outstanding on the balance sheet, while Waterbase might chose to hold them on the balance sheet as receivables until fructified.

Just a thought!

1 Like

To my knowledge, Avanti made a conscious decision few years ago to shift to cash & carry model in feed segment. This was done to manage their working capital in a better way and also to instill financial discipline among farmers (who may over buy during peak season, if there is a credit period by feed companies). And the same was reiterated by management in last year AGM (2017). And if I am not wrong, receivable discounting facilities are generally revealed by companies in contingent liabilities (nothing of that sort in 2018 AR).

7 Likes

Avanti Feeds is a classic example to learn how to differentiate a cyclical business from a secular growth story. Its one of the better variants of a cyclical business.

FY 18 was a bumper year for the company in terms of profitability with raw material prices abnormally low and end products (shrimp and shrimp feed) prices very high. This was obviously not sustainable going forward because of the nature of the business where the raw material prices and end product prices tend to fluctuate wildly. There are a lot of variables affecting this business, some of which like disease have not really played out in India and still the stock price has taken a huge hit due to other variables playing out.

A lot of investors even experienced guys tend to get sucked into the strong tailwinds (for ever) story and often end up buying at wrong price or failing to sell at the opportune time.

Currently the situation seems to have gone to other extreme and company is facing strong headwinds. For those contemplating buying I think it pays to be patient and wait for atleast some strong data points to emerge before going ahead.

26 Likes

the best time to invest in a cyclical business is when the industry is going through a bad phase with expectations of things bouncing back in the future. the shrimp industry right now satisfies both these check points. Also in such times it is prudent to enter companies with great balance sheet and market leaders with better competitive edge than peers. Avanti feeds satisfies this condition. The valuations also factor in the poor market conditions prevalent and do not even give premium to Avanti given the fact its a market leader with better competitive edge then peers. Hence i believe its a good time to enter the stock right now.

11 Likes

IMV, when data points show a recovery, stock would have flown up… And people will not buy, saying it is expensive…

2 Likes

I think what Hitesh Sir want’s to point out is you should wait for at least one or two quarter due to couple of headwind this industry is facing as far as I know.

- Raw material price like Soya are at very high level even the MSP was hiked by the Govt.

- Farmer have delayed the 2nd crop cycle hence the realization will be low. And this can only go up once there will be a demand recovery in US and EU market.

- Margin will not be that attractive for the company in future since it has venture into new area of low margin which is a good for long term outlook but near term trend is not looking good.

- Even though the festive season will playout some good benefit to this sector but demand recovery will not immediately reflect in the balance sheet of Avanti since crop cycle has been delayed.

- Also this sector has often has a great risk of disease outbreak and embargo due to geo political concern which has not materialized yet.

So it will be safe to avoid this cyclical industry as of now and only try to buy when it’s competitor countries will be facing this kind of concern[like in 2013 shrimp disease outbreak in Thailand] and situation of Indian environment is relatively stable.

3 Likes

Marine Products are de-growing and there is no reversal in trend.

Last year’s high base will make it difficult for the company in Q3 as well. Weakness in the rupee has somewhat offset things I think. RM prices as well are putting pressure on gross margins. Negatives are piling up and are not reflecting in the price I feel. Technically there is a gap in the charts between 300 and 350 which I think will get filled. I think 300 is a fair price to pay and it will get there post Q3 when pessimism will peak.

9 Likes

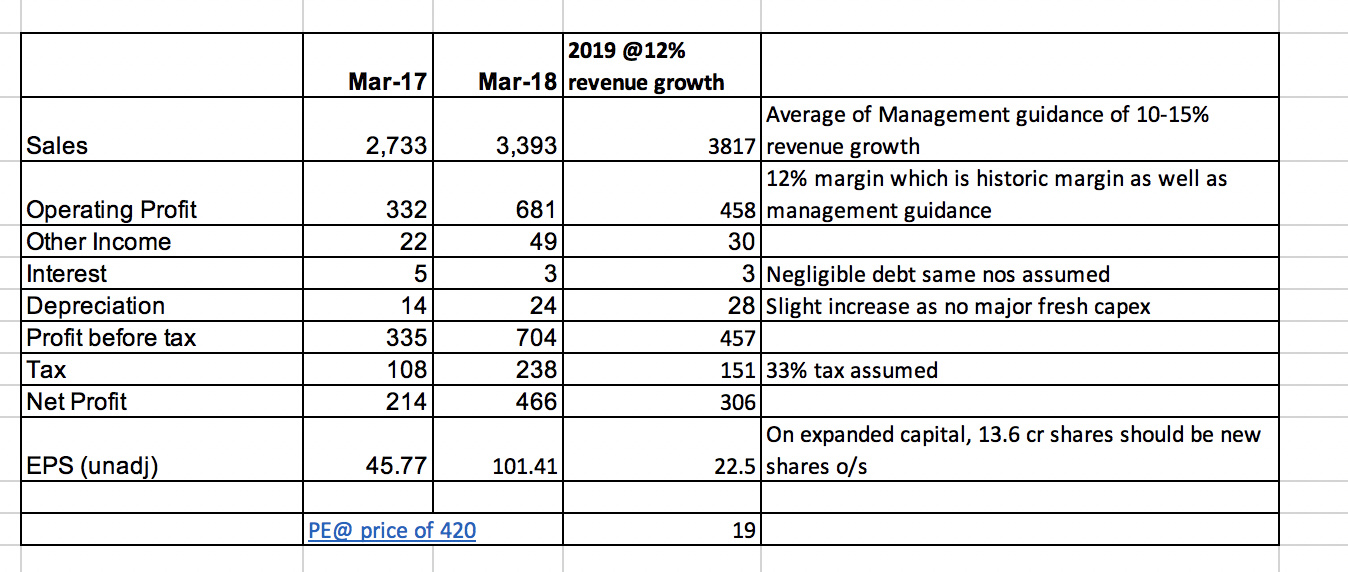

In my July post we were looking at EPS of 22 based on management estimations at con call which seems unlikely to be met, we are probably looking at around 20 EPS now. Even at current price of 370 odd we are close to PE of 18, on this. Long term industry fundamentals and good management notwithstanding, from a margin of safety perspective I am not sure it deserves a PE greater than 15…

{kind=link}

Disc - hold tracking position

4 Likes

Presentation and call details for concall on 20th.

The comments in the ppt seem to suggest q2 was the bottom for Avanti.

Rgds

RR

7 Likes

A cyclical stock like Avanti Feeds needs to be played very differently from a regular, secular business. Here’s an excellent link from @hitesh2710 - CYCLICALS-- When and Where to Bet?. Agree with @lastgenesis on Avanti Feeds

1 Like

Hitesh sir, in case of a avanti v need to know how company fared in last downward cycle and above how long the last cycle last, to my knowledge they were in loss in last downward cycle, latest momentum investors need to take account of that period, I feel current perception among the investors is this could be a mild down leg in a booming shrimp industry, which they consider to be a fmcg type of business and sir what should the p/e of a cyclical business like this, may be not more than 15. Considering that it seems to me that it’s still expensive

1 Like