Radical Changes for promoting Food Products manufactured/produced in India

It has now been decided to permit 100% FDI under government approval route for

trading, including through e-commerce, in respect of food products manufactured

or produced in India. Says the commerce ministry…

http://pib.nic.in/newsite/PrintRelease.aspx?relid=146338

1 Like

Also mentioned

Animal Husbandry

As per FDI Policy 2016, FDI in Animal Husbandry (including breeding of dogs), Pisciculture, Aquaculture and Apiculture is allowed 100% under Automatic Route under controlled conditions. It has been decided to do away with this requirement of ‘controlled conditions’ for FDI in these activities.

Hi,

It is a common practice amongst companies, especially the ones which do not issue CP/NCD, to switch rating agencies and get higher ratings. Once they get higher rating from competing agency, they do not continue rating with the earlier rating agency and the rating gets suspended. Think from a management point of view, they would be more interested in getting higher rating and reducing their interest rates rather than looking at whether the new rating agency had done some goofups in the past.

Thanks,

Ankit

9 Likes

2 Likes

This is my first post on analysis conducted recently… happy to have ur feedback/ criticism.

Avanti feed: june 8th, mcap of 2,182 cr

Disclosures:

I am a recent investor in Avanti with holdings less than 100k inr

This is my first post, so I might have missed a few rules (if any). DISCO, let me know my fault.

Please highlight if any errors, i will be willing to amend them

Any feedback (good/ bad/ ugly) on below, is always welcome

Shrimp industry

Shrimp is a globally traded commodity (and an actual one, with almost no product differentiation/ branding) and so the prices of shrimp, like other commodities fluctuate hugely; a factor of demand, production in different countries (and disease impact thereon), foreign exchange rates. Prices of shrimps, like other soft commodities will remain volatile and so I wont spend time chasing an unchasable ghost. Although, it has increased substantially over last few years (not counting year on year volatility).

On the volume front, imports in key countries (EU, US and Japan) has largely remained static at 1.6 mm tonnes1, however on the supply front there has been a huge shift and with beneficiary being India. Frozen shrimp exports from India increased from 189KT in FY12 to 357KT in FY15 and down c10% in latest FY. Production from key countries like Thailand was impacted by shrimp diseases (c.50% down from its peak of 600KT), from which India remained insulated, until last year. Another reason for the increased quantities was shift from black tiger (Penaues monodon) to Vannamei; which has higher density.

The dream run we had in shrimp production witnessed a bump in FY16 with India’s shrimps exports down 10% yoy due to lower production on account of shrimp. And the outlook in terms of industry growth now doesnot look very promising. We had a peak production of c.357KT in FY15 and it is unlikely we will see this volume doubling up in next 4-5 years; partly due to the fact that adoption of vannamei that yielded volume benefits is now largely over and growth would depend on new pond being brought under cultivation and at the same time warding off spread of diseases. The link below available on google of Rabobank presentation very well captures the volume dynamics of global shrimp industry.

Feed industry: Feed industry in India is dominated by two key players, Charoen Pokphand a Thai player with 41% market share and Avanti being a close second. Over the years, Avanti has gained market share, registering volume growth above industry rates. With Avanti already close to being a dominant player and further growth rate would be tied to the fortunes/ volume growth of industry.

Feed conversion ratio for shrimps is c.1.7 (obviously dependent on a lot of factors).

Feed cost and composition: as per the raw material consumption provided in Avanti’s annual report; feed composition seems to be pretty static, comprising 32% wheat, 22.0% fishmeal, 39% soya and c.10% others. To note, prices of each of the component is again dependent on market pricing, and in terms of value, soya and fishmeal form c.80% of the RM cost.

From the below, seems like, the Company’s feed sales price is dependent on the raw material costs, which forms c.75% of sales value and is predominantly comprised of soya and fish meal costs. Avanti has been able to increase its per unit profitability and that has also seen an increase in EBIT margins from 9% in FY12 to 11% in FY16.

The Company’s feed business forms around 85% of its revenue and profitability. The feed business has been the focus of the company in past, growing more than 10x in past five years. As discussed above, the margins of the business has gradually and consistently improved over the last few years, increasing from 3.3% in FY11 to 11.2% in FY16. The increase possibly comes from the benefits of scale along with increased channel efficiency and should possibly help it sustain these levels, although the huge growth from here remains questionable.

Segment (lakhs) Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Sales 20,773 39,340 64,803 1,13,159 1,77,625 2,01,828

Feed 13,307 27,148 50,184 85,710 1,50,746 1,73,009

Shrimps 7,293 11,976 14,379 27,209 26,691 28,605

Others 173 216 240 240 188 214

EBIT 575 4,132 4,603 10,498 17,256 21,905

Feed 444 2,537 2,575 7,219 15,058 19,441

Shrimps 40 1,489 1,897 3,153 2,107 2,352

Others 91 106 131 126 91 112

EBIT 575 4132 4603 10498 17256 21905

EBIT Margins 2.8% 10.5% 7.1% 9.3% 9.7% 10.9%

Feed 3.3% 9.3% 5.1% 8.4% 10.0% 11.2%

Shrimps 0.5% 12.4% 13.2% 11.6% 7.9% 8.2%

Sales Composition 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Feed 64.1% 69.0% 77.4% 75.7% 84.9% 85.7%

Shrimps 35.1% 30.4% 22.2% 24.0% 15.0% 14.2%

Others 0.8% 0.5% 0.4% 0.2% 0.1% 0.1%

EBIT composition 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Feed 77.2% 61.4% 55.9% 68.8% 87.3% 88.8%

Shrimps 7.0% 36.0% 41.2% 30.0% 12.2% 10.7%

Others 15.8% 2.6% 2.8% 1.2% 0.5% 0.5%

EBIT

Shrimp processing: Avanti’s shrimp business basically comprises buying grown shrimps and process (removing head/tails) and then exporting frozen shrimps (c.66% weight yield). These are usually low value products and Avanti I believe would now be focusing on value added processed shrimps. It is targeting c.40% revenue from shrimp exports over next three years2.

The business which had been a better margin business in past, reported lower profitability and part of the reason explained by the company was stringent US regulations, which resulted in increased costs and diversion to other markets.

Avanti transferred the existing processing business into a new subsidiary, in which Thai Union has recently bought 40% stake.

The Company is increasing its processing capacity from current 25tonnes/day to 75 tonnes/ day, which would result in revenue increasing by three times to close to 900 crores. If it maintains its margins of c.9%, we will see c.30% increase over next two year coming from this business alone, although equity return would be diluted by 40% stake sale. Thai union is amongst the leaders in processed sea food and with technology transfer, Avanti should be able to transition from frozen shrimps to value added shrimps and which should aid margin growth. Good things aside, it gets c.7% to 8% of its shrimp exports value as some kind of export incentive, which in FY16 was 23.54 cr, a tad more than its EBIT of 23.52 cr. The company’s margins have been impacted over last two years and thus making this divisions profitability more and more reliant on this export incentive. Can somebody explain me what this benefit is and how long its going to last???

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Frozen shrimp KT 189.000 226.00 302.00 357 321

% Growth indian shrimp exports 22% 20% 34% 18% -10%

Avanti feed volume growth rate 125% 72% 46% 56%

Frozen Shrimp (Cr) 4,242 6,321 9,608 19,175 24,000

Shrimp Production Growth 20% 34% 18% -10%

Capacity Feed 42,000

Production

Feed

Shrimp Feed 27,033 59,230 1,05,422 1,45,930 2,33,489

Fish 10,098 3,589 402 -

Sales

Feed

Shrimp Feed (Tonnes) 26,642 59,837 1,02,988 1,49,891 2,33,489

Fish (Tonnes) 10,067 3,646 405 -

Sales Value

Shrimp Feed (Lakhs) 11,681 26,368 49,992 85,611 1,50,654 1,73,009

Fish Feed (Lakhs) 1,611 590 65 - -

Feed Value (Rs/KG) 43.21 44.52 47.42 58.67 64.52

Feed RM Cost (RS/KG) 38.63 30.51 38.48 42.45 48.95

Feed EBIT (Rs/KG) 1.2 4.0 2.5 4.8 6.4

Processed Shrimps

Shrimp Production (Tonnes, T) 1,450 1,966 2,713 3,289 3,409

Shrimp sales value (Lakhs, L) 6,444 10,817 13,525 25,338 24,935 26,351

Shrimp export incentive 813 1,160 853 1,870 1,756 2,254

13% 11% 6% 7% 7% 9%

No debt comes at a cost and that is inside the growing SG&A figure which in FY15 was at 102 cr. Of this 102 cr, 72 cr was cash discount or 4.1% of sales. Assuming a 90 day credit cycle, that’s a cost of 16.4% per annum. That’s huge. And also this number seems to be growing gradually. 3.3% in FY13, 3.4% in FY14 and 4.1% in FY15. Seems like the company is fighting share battle with comptetors offering extended credit in supply chain. Call me old school, but I prefer a ballooning number here than on the balance sheet.

Financial analysis of income statement:

The Company which has grown at above 50% yoy till FY15 slowed down in FY16 to just 12.3% and this trend seems to be here to stay. This company has grown above industry but now it’s very close to market leader at c.38%. Significant growth of +50% kind or even 30% kind from here seems unlikely. 30% would mean this company gaining c.8% market share from here; in oligopoly market, CP would fight fiercely for this one. The avenue for growth seems to be the shrimp processing division, where the silver light is moving towards value added shrimp; but the profitability of this division is under pressure; and dependent on the export incentive (remember??). Avanti is tripling its capacity, which means 858 cr in revenue (assuming flat shrimp prices); a growth of just c.30% over FY15 total sales. The segment is a bit small to make a dent in overall scheme of things. Also, 40% of this growth and profits would accrue to Thai Union. Avanti, the company is now more reliant on its old horse, feed business.

I have discussed the past trends for rest and there is nothing much there. Manufacturing expense has gradually come down possibly thanks to increasing scale and efficiency, also evident in electricity consumed per unit shrimp and feed over past few years.

This year 23cr was also contributed by other income (up from 9) and comprises usually bunch of gains (fx, asset sale, investments). Growing at a good rate, but that’s not why I am betting on this company. Amazingly this gains forms 37% (and that is after taking tax) of your FY16 yoy incremental EPS (up from 13% of contribution in FY15). Looks like we will see this again in FY17 with 40% stake sale closing, resulting in gain of c.90 cr (125-86.4*40%), but what after Diwali dhamaka??

Well I am bad with valuation and I find it funny given all the ifs and butts. But nonetheless, I have tried to go with a generous growth figures to see what is the max possible from here.

From revenue growth perspective, next few years seems like a consolidation phase. Assuming a liberal 20% feed revenue growth for next two years and another 15% in 2019 and 2020, and tripling of shimp processing every two years (75tpd by 2018 and 225tpd by 2020), you would be around tripling the revenue to c.5900 cr in 2020 (flat prices). If I take segmental EBIT and assume constant margins for feed and +1% margin expansion for processed shrimp to a max of 10.2%, we reach EBIT of 633 crores, c.3x jump from FY16. Remember the fun part, 42% of this is now coming from shrimp business, of which 40% is with Thai Union. If I remove, Thai’s stake, EBIT would increase to only 528 crores, a jump to 2.4FY16 figure.

Now there are a lot of dependencies in above; I agree hands down, but even with the liberal in my heart, seems like the dream run is over. And the good times in Indian industry remains dependent on a lot of factor including the shrimp disease gods. If you are an atheist, check with a Thai shrimp farmer, he will tell you what can happen when gods go angry.

1 http://icwpf.com/wp-content/uploads/2015/11/Shrimp-industry-dynamics-ICPF-presentation.pdf

2http://www.businesstoday.in/magazine/cover-story/emerging-companies-2015-avanti-seeds-growth-on-shrimp-demand/story/221077.html

14 Likes

I have done some projections for FY17 for Avanti feeds. The projections are based on following assumptions -

-

Price of feed in fy17 will remain constant (average) and same as in fy16.

-

Price of processed shrimp in fy17 will remain constant (average) and same as in fy16.

-

Avanti and Thai Union will not produce any new value added product from the new plant.

-

Overall size of Shrimp feed market will increase in India.

-

No news of new feed plant triall & commissioning therefore assuming 2 quarter delay & 100% capacity utilization once commissioned.

Feed production in fy16 = 2.5L tpa (lac ton per annum)

Feed capacity increase by 1L tpa

Utilization 50% in fy17 = 50k ton

Feed production in fy17 = 3L ton

Revenue from feed in fy16 = 1730cr

Revenue/L ton = 164.4 cr

Revenue for 3L ton = 2076cr

Shrimp processing 7300 tpa at 50% capacity utilization, Revenue = 286cr

Additional 25,000 tpa for 3 quarters at 50% capacity = 734cr

60% share of Avanti feeds in Avanti frozen foods = 440cr

Revenue fy17 = 2516 (Growth = 25%)

Assuming, Net Profit Margin = 7.7m%

Net Profit = 193 (Growth = 25%)

Disclosure: Invested.

Soya/its derivatives are important raw material for shrimp feed. So this could effect margins for a while if they cant pass on the prices

2 Likes

Firstly appreciate your diligent effort on the very first post on Valuepickr. keep on participating, I am sure, you will be able to add value for yourself and the forum.

Here is my assessment, specifically around the bread winner for the family, that is Shrimp Feed business:

Past: The feed business has grown exponentially between FY 12 to FY15, ranging from 100% to 75%. Key

thing to notice is that around 2012 -13 feed was contributing close to 65% rest was from shrimp business (same proposition that Avanti want to attain again).

Shrimp Feed business growth:

2012: 104.01%

2013: 84.85%

2014: 70.79%

2015: 75.88%

2016:14.77%

Current state: For FY 15 -16 total sales was around 233,000 lac tons, a growth of 14.77%. More of an outcome of running at approx. full capacity of 2.5 lac Ton/year. Mr. Indra Kumar’s admission on that:

“We are a close second. One of the reasons we are expanding is that at times we are not able to meet demand for our products,” link

Near to mid term Future: With the proposed investment of ~300 Crores they will get 1,10,000 lac ton (~44%) capacity increase thus a linear growth visibility of 30%-40% for next few 4 -8 quarters.

Long term future: (possibly 2018 onwards): Now the next pertinent question that I as a long term investor will try to decode is, how the landscape will look like once the augmented capacity of 3.5 Lac ton/year is exhausted? How much of head room for further capacity expansion thereby sustaining the growth trajectory?

Few pointers;

-

Total market size of shrimp feed in India ~600,000 ton/year. Shrimp production growing at ~16% link

-

CP had massive capacity expensing plan between 13 -15 (~500 crores if I recall correctly). Will be difficult to dislodge from #1 position.

-

Avanti positioned close #2 after CP Aquaculture. Have a market share of ~31%. With the improved capacity of ~3.5 lac tons they will possibly have a market share close to 50%.

-

Shift of focus towards shrimp/value-add products.

Basis the above, personally to me it seems that it will be little uphill for Avanti to have high growth rate on the feed business. A lot will be riding on the shrimp business for Avanti to deliver growth and profitability.

Positive thing is Thai union now has a strategic shift towards Avanti, possibly driven by historical geographical concerns, and Avanti playing a pivotal role in the risk mitigation strategy for Thai Union. Key thing to watch out for will be is this all about frozen shrimp (generally 70% of Indian aquaculture export) or other value-add products where better margins can be expected.

On a side note, really liked Inder Kumars confidence when he mentioned about aspiring to be a billion $ company by 2020.

disclosure:

1.Avanti feed consist of ~5% of my PF, no transaction in last 30 days.

2. Still learning

4 Likes

Thanks Tarun… Couple of new pints that i observed after that and reading yours:

-

New aquaculture policy targeting tripling of exports to 1 lakhc crore. This possibly means increased shrimp production as well as other species

-

Avanti in past produced fish feed (2011-2012). I think, they diverted away from it to shrimp feed for maybe better demand and focus. In terms of production, capacity should be interchangeable which means remarkable head room to grow, especially if above holds true and market grows substantially. The market is not limited to shrimp feed, but this needs to come from management if they are looking to enter fish feed business??

-

The processing division also has remarkable room with growth of industry. Especially with 40% stake, which in conjunction with their parental holding, gives them synthetic majority in processing division. This should allow tech transfer and better operational integration with a smart parent (Thai Union). Seems like good times (not great i would say) are here to stay and may be from a distance, we are looking at a story of shrimp feed company transforming into a full fledged aquafood processing company.

2 Likes

An article on Aquafeed market projection -

Aquafeed Market size worth USD 185 Billion by 2023: Global Market Insights Inc.

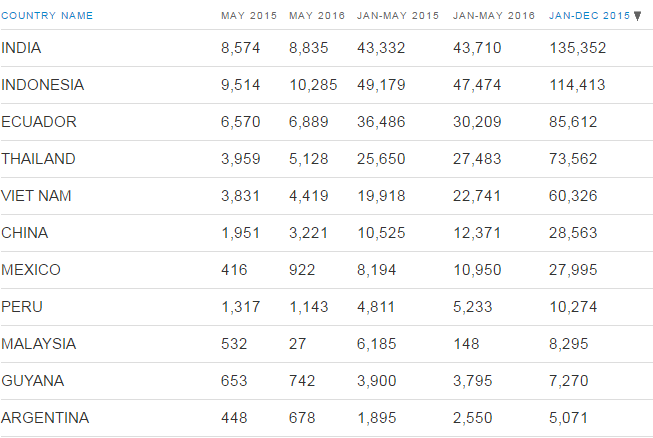

US Shrimp imports up by 11% while India export up by only 3% (Looks like India is loosing market share because of duty differential)

Indonesia shipped 10,295t, up 8.10% y-o-y. In second place in May is India, with 8,835t, up 3.04% y-o-y. Ecuador is the third largest supplier in May, with 6,889t, up 4.85% y-o-y.

The recovery in Thailand’s production from early mortality syndrome was evident in its May figures, with US buyers importing 5,128t of shrimp, up 29.52% y-o-y.

Vietnam also upped exports to the US in May to 4,419t, a 15.34% y-o-y increase.

4 Likes

I want to understand that why would they impose an import duty for Indian products as anyway they are importing stuff from so much countries hence no single geography dependency. Can you explain me if you have an answer?

One of the listed shrimp processing co - Coastal Corp - http://www.bseindia.com/xml-data/corpfiling/AttachLive/9EF4625E_705E_47DF_A111_44A2D5D5D5C2_143529.pdf delivers 35% growth in Q1

12 Likes

Ayush, on employee expenses & Finance costs itself they saved around 1.7CR, but sales wise it was very good result.

Indian seafood exports to go up by 15 - 20% in FY 17. Price realisations are also likely to move up due to disease in competing countries - says economic times. Good news and growth for Avanti feeds.

http://www.pressreader.com/india/economic-times/20160713/282016146662200