Massive frozen foods recall over apparent fears of Listeria outbreak involves millions of packages in US. So far the list of items include only organic frozen foods (veggies)…it might also spread to meat items…

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/6AA64C7F_FB9E_40C0_8057_CD91B3BEEB5D_151216.pdf

Q4 results came out 3 minutes ago

Consolidated figures, a quick comparison Need I need to say more? The figures speak for themselves

a final dividend of Rs. 7/- Per equity share (350%) of Rs. 2/- each for the year

12 Likes

Great set of Q4 numbers by Avanti. Even after floods, 15% Top line growth and 21% bottom line growth in H2 YOY shows how resilient this company is.

Disc: Invested.

2 Likes

Yes - the numbers are solid. However the market has not rewarded this stock like it used to in the past.

Disc : Invested - this stock has significant % of my total investment.

Couple of relevant news items:

Chinese shrimp farming is looking in a bad way in 2016.

Widespread reports of low or no stocking, cautious farmers, a lack of finance, and lower sales of feed and medicine all point to depressed white shrimp production.

It appears that the industry has not got a handle on disease and many farmers are giving up, or being forced out of business. Rental prices for shrimp ponds have collapsed.

A reporter from Current Fisheries, a Chinese trade publication, has got some depressing replies from white shrimp farmers and sellers during a survey of the white shrimp aquaculture sector.

The shrimp aquaculture has been trapped in an extremely tough situation after over a decade of high-density farming. Although various industry participants have tried to improve the situation, there are few changes to the whole industry.

As China is the largest shrimp consumer, this should give the prices a good kick. However, also a point of caution, as India too may end up in similar situation in future.

Test production will start in June in Avanti Foods, the Indian joint venture plant with Avanti Feeds. Boonmechote previously told Undercurrent he wants the plant to be able to produce a full range of products, including value-added, as the company’s Thai factories do.

“We can provide more variety of sources all of the same quality, with everything managed by our people,” he said.

The plant will house raw, cooked, and value-added production lines with raw material production capacity of over 25,000t per annum, Boonmechote said.

Value added shrimps and hatcheries should be the main story in Avanti for some time.

11 Likes

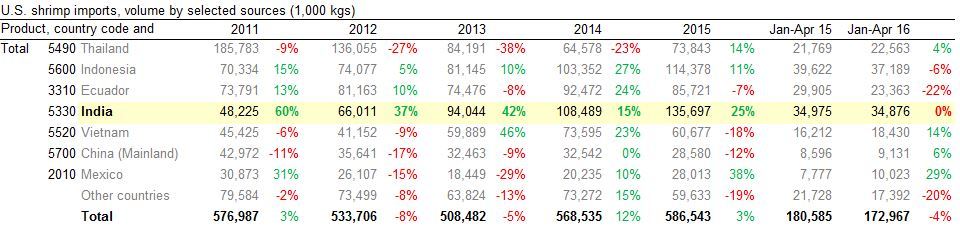

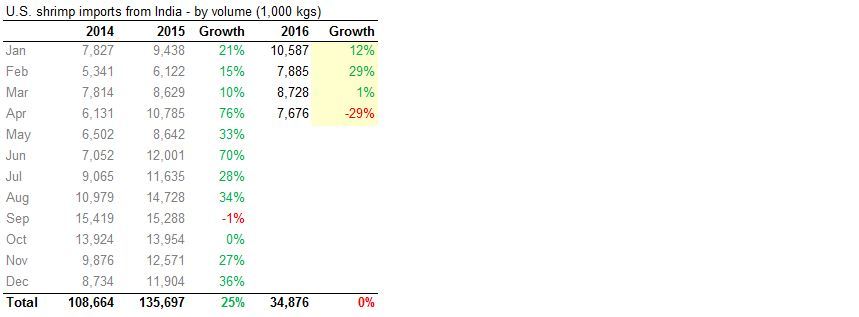

U.S. Shrimp Imports (April 16)

- India shrimp export to U.S. drops 29% YoY in Apr '16.

- Seems impact of anti dumping duty hike and high base data.

- U.S. consumption down 4% YoY.

- May '16 outlook: Per Zauba, Indian shrimp export to US is up ~50% QoQ. Can expect ~15% growth YoY.

- Seems Indian exporters are switching to other markets, particularly to Vietnam (re-routing for duty benefit?).

Source: http://www.ers.usda.gov/datafiles/Aquaculture/Trade/AquacultureTradeRecent.xls

Disc: Invested. No transaction in last 30 days.

9 Likes

Devi Sea Foods - This unlisted company is part of the next Fortune 500 India companies list - seems to be in the same business as Avanti and claims to be the largest exporter of shrimp from India to the US.

http://www.deviseafoods.co.in/our-story/

Financials not disclosed on its website

Deepak Shenoy’s brief recommendation on Avanti Feeds - watch from 6 min mark

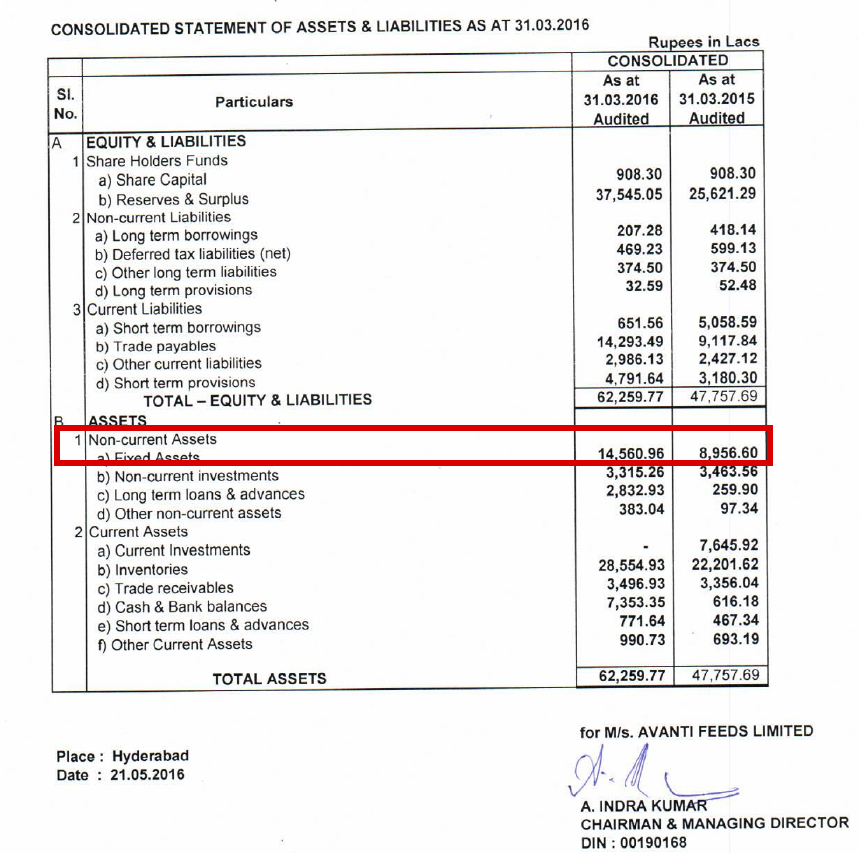

Below is Fy16 balance sheet of Avanti feeds

It show an increase of 56cr in fixed assets. I think the increase must be due to 25K ton shrimp processing plant added to Avanti frozen foods.

Any new information on expansion will be useful.

Courtesy: Economic Times issue dt June17, 2016

Small-sized shrimps are finding big global takers that may lead to better production of aquaculture shrimps this year

Higher global prices for smaller-sized shrimps may lead to better production of aquaculture shrimps, which are the mainstay . 33,000-crore Indian seafood of the ` exports, this year.

Farmed shrimps now account for around 70% of marine products export from the country. Last fiscal, the export remained subdued with a plunge in shrimp prices and a decline in production due to rains and diseases.

Though the stocking was slightly delayed by prolonged hot weather, harvest has started in farms, mostly in Andhra and Tamil Nadu. Unlike last year, prices for smaller size shrimps have gone up pro mpting farmers to harvest early.

“The harvest has been good so far.Instead of waiting for 140 or 150 days, they can harvest in 90 days, which helps in better survival rate as mortality rate could be higher if the shrimp grows bigger,’’ said S Muthukaruppan, past president of Society of Aquaculture Professionals in Chennai.

Prices for smaller sizes of 60, 70 and 80 counts per kg have increased by 30% to 40% from last year hovering in the range of `. 260 to 310 per kg. In the last three years, the larger sizes (of 30 to 50 counts) used to fetch higher prices.

“Both demand and prices are stable. With the trawling ban in Kerala, the catch of squid and cuttlefish could come down. But it could go up after July,’’ said Anwar Hashim, managing director of Abad Fisheries. Though data on seafood export for 2015-16 is yet to be released the first six months saw a 20% drop from a year ago. Globefish under FAO that provides information on world fish trade says that despite lower output, India was the lead supply source exporting 3,83,000 tonnes of shrimp in 2015. Lower shrimp prices helped producing countries increase exports beyond traditional markets, especially to Vietnam, China and other markets in Asia.

Click To Enlarge

Click To Enlarge

1 Like

Coverage of the sector and Avanti in the upcoming issue of Business Today - http://www.businesstoday.in/magazine/corporate/aquaculture-gains-on-the-back-rise-in-shrimp-exports/story/233663.html

7 Likes

Ayush don’t you feel the OCF even this fy is not very good how do you feel they will be able to Improve there operating cash flow is it not a worrying factor to consistently have lower cash flow pl. Guide. Thanks

Hi ,

Any idea about Aries agro this is also something related to blue revolution …isn’t it ???

Dear Ayush

Kindly comment on the following comment by CRISIL while it suspended the ratings of AVANTI in June 2015

CRISIL is of the opinion that " non-sharing of information as a first signal of possible credit distress," since AVANTI is not providing the required information to CRISIL inspite of repeated requests. I am posting the link below; It would have already come to your notice ; I searched the forum and I was not able to see anyone highlighting this in this forum. Hence my post

Sorry that I am raising a red flag about AVANTI in my first post itself

CRISIL has suspended its ratings on the bank facilities of Avanti feeds Ltd (AFL). **The suspension of ratings is on account of non-cooperation by AFL** with CRISIL's efforts to undertake a review of the ratings outstanding. Despite repeated requests by CRISIL, AFL is yet to provide adequate information to enable CRISIL to assess AFL's ability to service its debt. The suspension reflects CRISIL's inability to maintain a valid rating in the absence of adequate information. _CRISIL considers information availability risk as a key credit factor in its rating process and non-sharing of information as a first signal of possible credit distress,_ as outlined in its criteria 'Information Availability Risk in Credit Ratings'

The link is here http://www.crisil.com/ratings/company_fact_sheet.jsp?ID=AVAFEED

4 Likes

This is quite serious and investors should reach out to IR team for knowing current situation. Also, need to check if the suspension has been lifted or ongoing.

Discl: Not invested but tracking.

I usually look at OCF for a block of 2-3 years and I’m ok if its about .8 times the net profit for a fast growing company. In the case of Avanti I think the OCF is good (the debtors are almost negligible, infact the working capital is negative…they only have to invest into inventory and it becomes high at March end as the next quarters are peak period). Let me know the number you are looking at?

@sekhar - thanks for pointing this out. I hadn’t taken a look. If we look the balance sheet of the company, they hardly have any borrowings (just 8.5 Cr in FY16 vs 55 Cr in FY15), infact they have paid back some of the borrowing so can’t think of risk of servicing of debt. It has been seen in some cases that whenever there is a credit rating company change, such things happen. But still its important and we should write to the company and the rating agency and seek clarity.

Thanks & Regards,

Ayush

4 Likes

@sekhar - Its seems the company had changed the credit rating agency - https://www.indiaratings.co.in/Issuers?search=1&issuerID=166&issuerName=Avanti-Feeds-Limited. Thanks for keeping a check

Ayush

2 Likes

Given the recent Ricoh episode of India rating, to me this does not reflect well on avanti- moving from crisil to indiarating

`

Disclosure 1: I have taken initial position in Avanti Feeds, within last <30 days only and forms ~5% of my PF.

Disclosure 2: This is my very first post on this forum. I have been a passive user of VP so far (more of learning and less of writing/contribution) and have learned immensely. Since I am recent investor on this counter, cant help being worried with the change in credit rating agency. Have spent some time understanding the context, rational and impact of this development.

So here I take the plunge…:

CRISIL rating 2014:

Last CRISIL report (link) dated Feb 2014 had following rating for Avanti Feeds for local debt instruments:

- Short term: Improved rating to A2 (strong degree of safety) as compared to A3 (moderate safety) for previous year for short term instruments totaling 500 mil INR):

- Long term: Improved rating to BBB+ (moderate safety) as compared to BBB- for previous year for long term instruments totaling 1110 mil INR):

Link to CRISIL rating scale

Fitch rating 2014:

FITCH report (link) dated May, 2014 has following ratings:

- Short term: Rating of A1 (strong degree of safety) for 370 mil INR.

- Long term: Rating of A- (just adequate degree of safety) for 1146.2 mil INR.

link to understand the FITCH rating scale.

So essentially what I see here is that this change of rating agency did not have much of a material impact on the short term / long term liability rating from two agencies. So on the face of it does not look like some hidden intents were in force behind the change.

Thanks,

T@run

1 Like

Trying to take a DIY(do it yourself) approach to see how Avanti Feeds looks like from the short/long term liability servicing standpoint.

- Current liability has has been broadly same between exit FY14 and exit FY15. however, almost 90% jump from FY’13. off handly I cant think of any assignable reason for that. is this more to do with seasonality?

@Seniors - if you can help on this. - Both current ratio and quick ration maintaining a health figure of 1.76 and 0.61 respectively. Icing on the cake, both rations has improved for FY’15.

- Significant FCF of 733 mil INR, grew by whopping 55%. By that does not that appear that short term will be an issue.

- last but not the least, (and thats why we love Avanti), high revenue growth clubbed with decent ROE.

Conclusion: My personal opinion is that seamless cash flow clubbed with efficiency are two key factors which should work favorably to short/long term debt serviceability.

P.S - I have just started out on this exciting journey called ‘collaborative learning’. There definitely will be room for improvement in analysis, envisioning, etc.

Thanks,

T@run

2 Likes