Please download the Annual Report 15-16 from the link below

http://www.avantifeeds.com/AnnualReports/Avanti%20Feeds%20Ltd-Annual%20Report%202015-16.pdf

Please download the Annual Report 15-16 from the link below

http://www.avantifeeds.com/AnnualReports/Avanti%20Feeds%20Ltd-Annual%20Report%202015-16.pdf

The annual report on page 19 mention that Avanti Frozen Foods (AFFPL) is implementing at 15k ton/pa plant

whereas the earlier news item in Undercurrent news at this link mentioned the plant to be 25k ton/pa.

Hi Gaurav,

25000 MT will be added in 2 phases- Phase 1 15000 MT and Phase 2 will be another 10000 MT

Hi Rokrdude,

Ok, do you have time for implementation of phase II. The article in Undercurrent has no mention of phase-wise implementation.

Was going through the FY16 annual report. Found the below paragraph

A quick question to the experts:

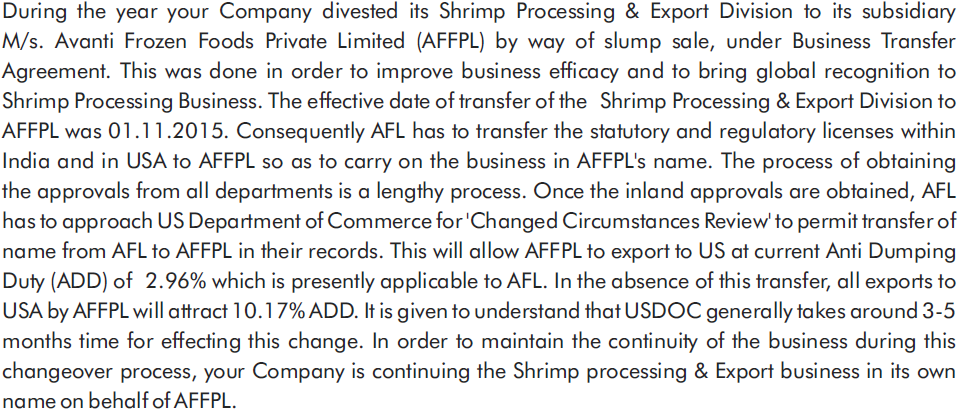

Antidumping duty(ADD) is mentioned as 2.96%. Doesn’t the new ADD rate applicable to Avanti? Is the ADD company specific or is it country specific? Since when does the new ADD rate come into effect(Thought it was announced and in effect in last quarter of FY16 )?

Thanks in advance.

Disc: Invested

Guys in addition to the above mentioned question around anti-dumping duty, can anybody help me with what is this export incentive for their processing division (2,253.96 lakhs in FY16; pg 159, note 19), essentially contributing most of their operating profits from processing division for past few years.

Sensing huge growth in Indian aquaculture sector, CPF India Limited a subsidiary unit of The Charoen Pokphand Group (CP) will be expanding its operations in India with a corn processing plant that will supply local and international shrimp and animal feed producers.

Q : Will this benefit Avanti in any way?

not sure, but corn is not typically used in feed preparation. its wheat, fishmeal and soya…

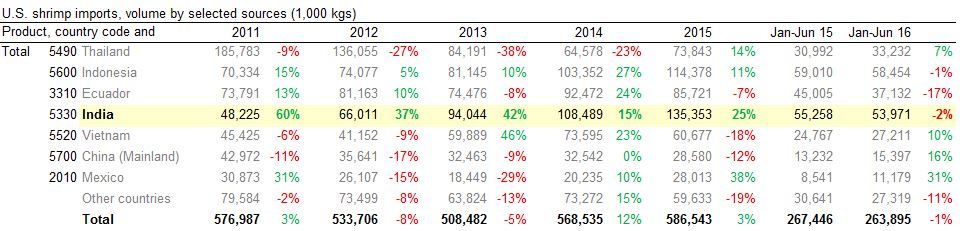

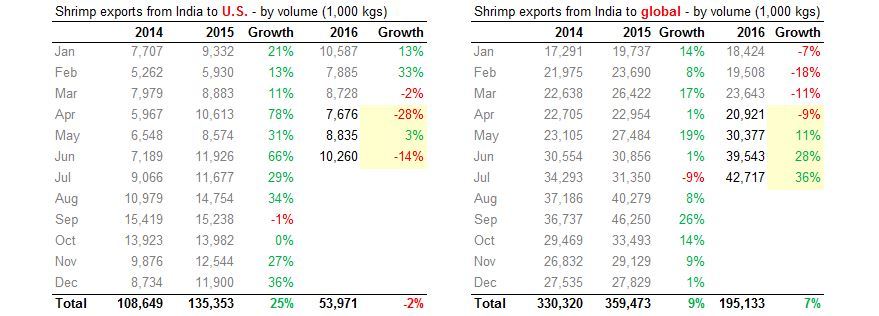

India shrimp exports (figures and analysis - by volume)

To U.S. (source: www.st.nmfs.noaa.gov/apex/f?p=169:2:0::NO::: )

To Global (source: www.zauba.com)

Avanti Feeds Ltd has informed BSE that Expansion of Company’s Shrimp Feed manufacturing capacity by way of setting up of new plant, with an installed capacity of 125,000 MT per annum, at Bandapuram, West Godavari District, Andhra Pradesh has been completed and the commercial production commenced.

Read it here.

Q1 results are out on NSE

https://www.nseindia.com/corporates/corporateHome.html?id=eqCorpAnnouncements&radio_btn=company¶m=AVANTIFEED

My summary - Very good top-line growth of 25% driven by ~40% increase in export sales. However, operating margin has dropped from 10.3% last year to 9.7% primarily because of increase in raw material prices and other expenditure.

Also received exceptional gain on refund of Countervailing Duty of 4 crore which has been accounted in Q1 of last year. All this has meant meagre PAT growth of 10.2% (~20% if you take out exceptional items).

Fairly decent results but operating margins would be my main concern if any.

I think these are very good set of number. Very few companies have shown a topline growth of 25% this quarter. With increase in feed as well as shrimp processing capacity the company is in a very sweet growth spot for at least next two years.

Disclosure: Invested.

The growth in the revenues from shrimp processing is good but margin in the same division has been declining with profit from division stagnating inspite of higher topline.

Otherwise the results in terms of 25% topline and 20% operating profit seem decent.

Avanti’s valuation in terms of PE has also come down drastically from about 27 times earlier to 16 times TTM now. Any particular reason for this that you can think of?

I think there are a number of unsaid rules about the P/E multiple a business should command and there is definitely no exact science that I’m aware of. For companies showing good growth like Avanti Feeds, I think markets are always trying to determine the correct P/E. But I believe there are 2 main factors which will help in arriving at some sort of a P/E range

For Avanti, pace of earnings growth is there for everyone to see. For type of business - you should probably go through this thread as it has evolved over the past few years.

Just to share my investment philosophy - I don’t buy a business (partially) expecting P/E expansion from let’s say 15 to 30, or even 6-8 to 12-13 times. That is just a MoS for me but it’s not factored in my potential investment returns.

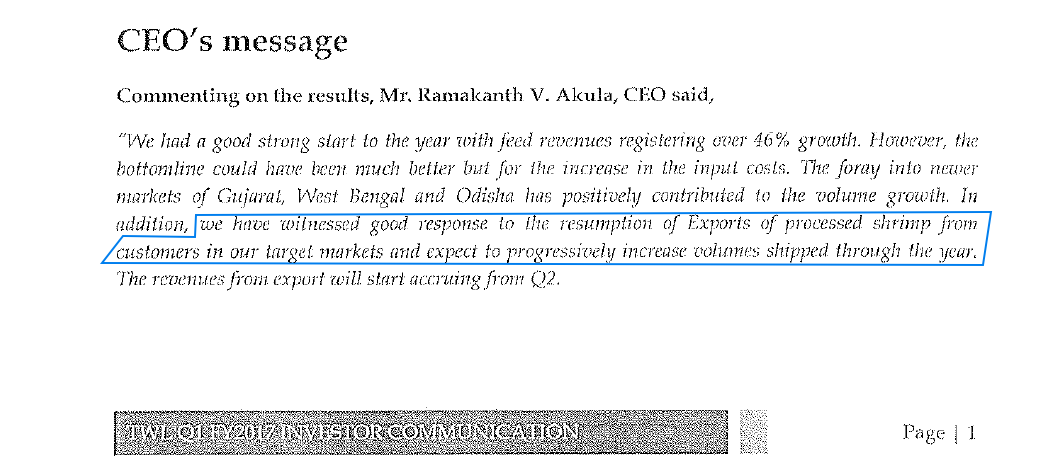

Corroboration of the point mentioned in the article liked by @Vivek_6954 by Ceo of Waterbase in q1fy17 results

Avanti Feeds Ltd has informed BSE that the Board of Directors of the Company at its meeting held on August 12, 2016, inter alia, has approved the following;

**

**

does anyone able to find the copy of the policy they approved? i don’t see it either in BSE or NSE.

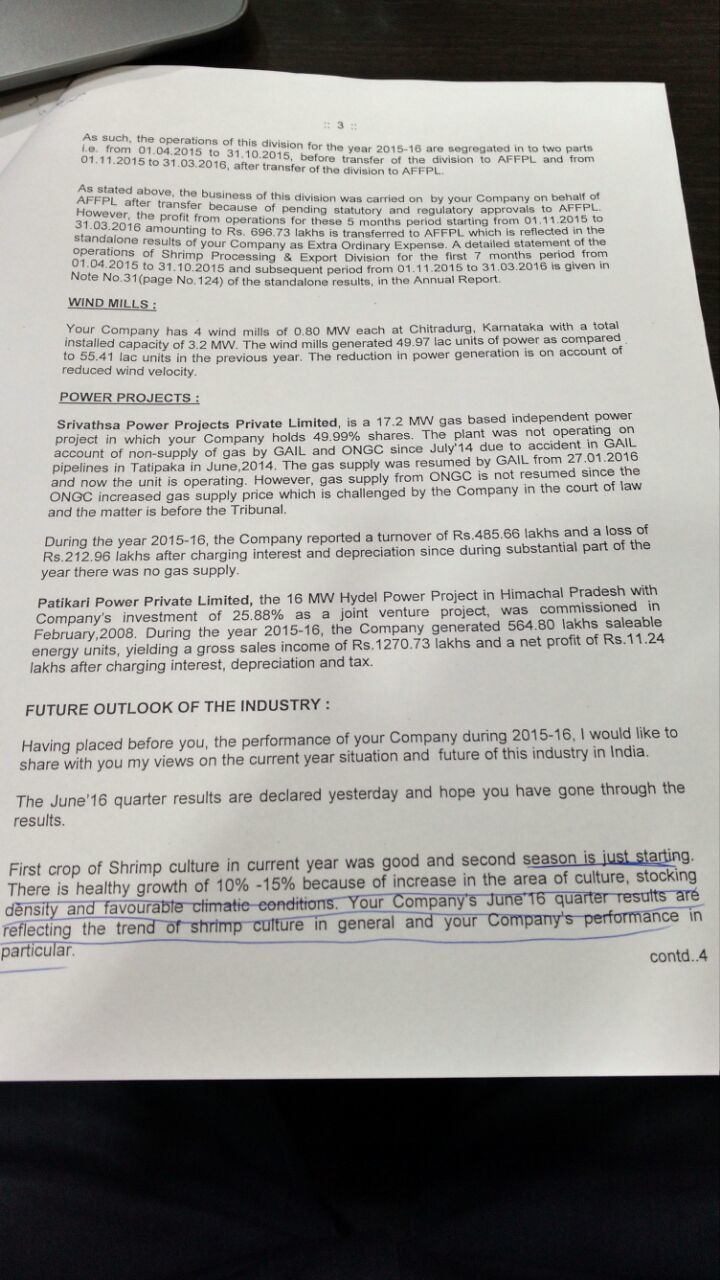

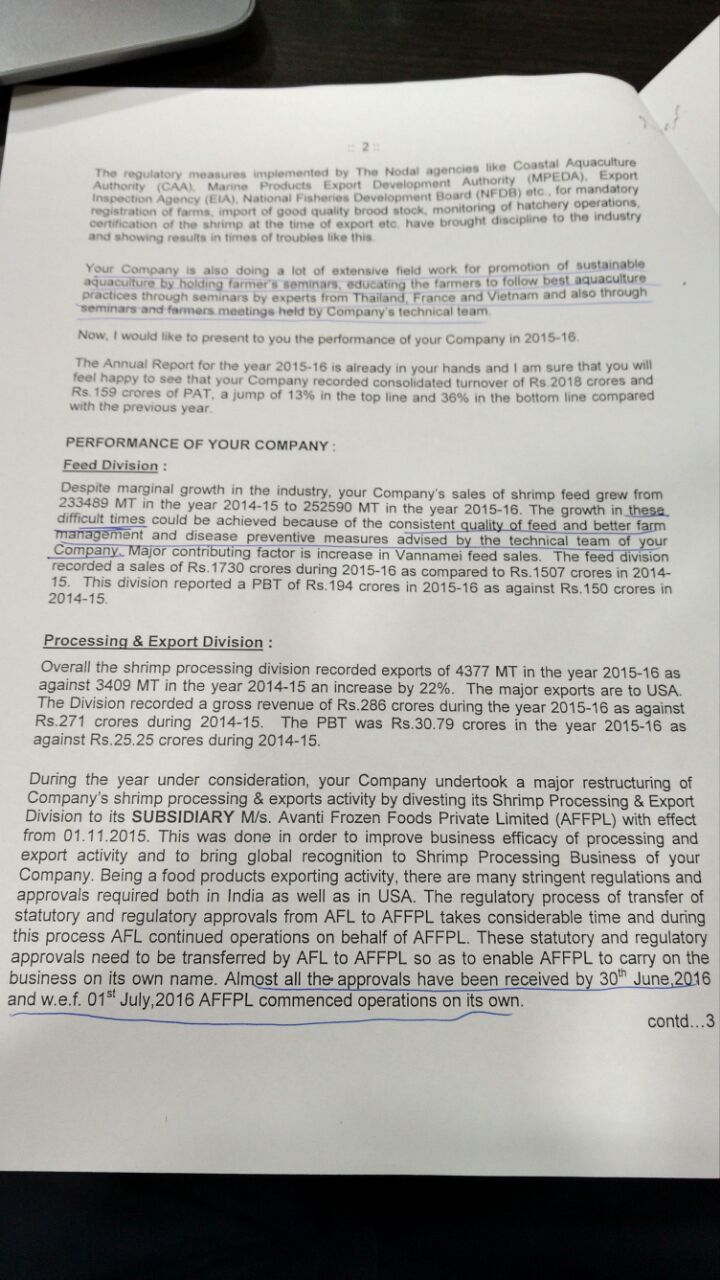

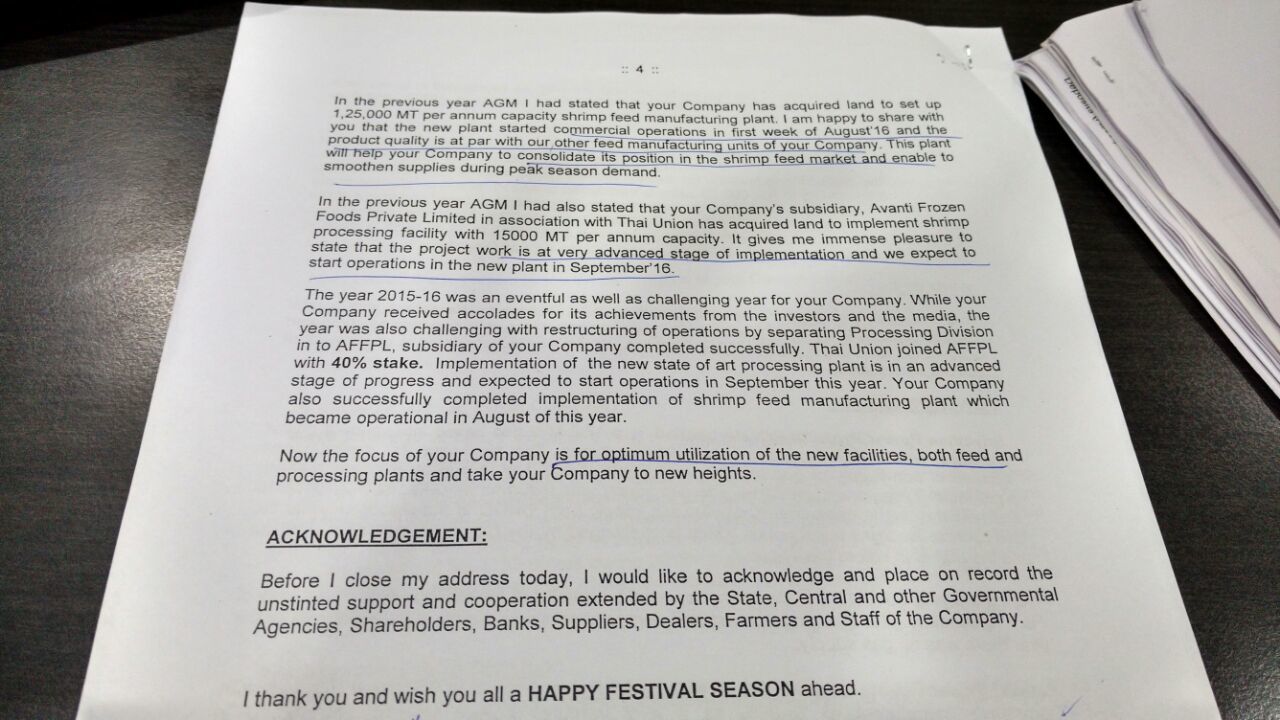

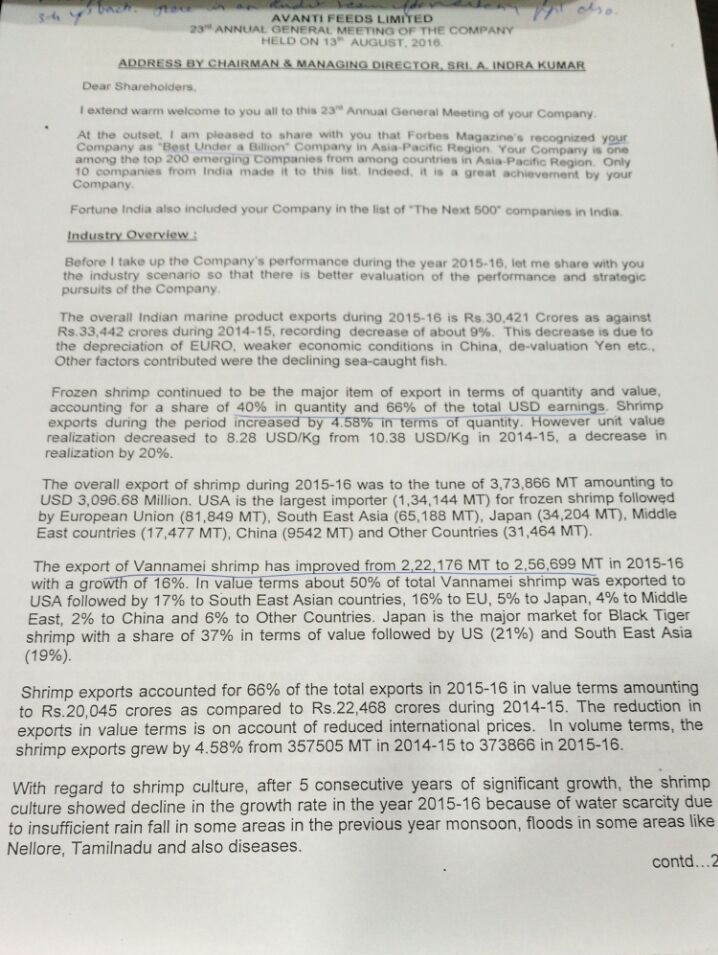

I attended the AGM of the company. Sharing the Chairman Speech and a summary of the discussion in the Q&A session - Avanti AGM 2016 notes VP - Google Docs

Ayush bhai Thanks for sharing chairman speech. What’s ur view on management commentary. Profit is not growing in line with top line specifically in last quarter.