Published on 18th Sep,2020

Hi guys. Sorry I was busy over the last few days. Please note that I picked up shares of the Company since the last time I posted so huge disclaimer!

Anyways I’m posting some basic research here along with my excel model. Please feel free to critique or provide feedback on anything you read here including my astronomical valuations.AssociatedAlcohols&Breweries_IC.pdf (1.1 MB) AssociatedAlcohols_Model.xlsx (78.7 KB)

5 Likes

Thank you for sharing.

1 Like

Thank You for sharing such a good info. I recently started tracking this company. Helped me a lot in understanding the business in detail.

1 Like

thank you for this link.

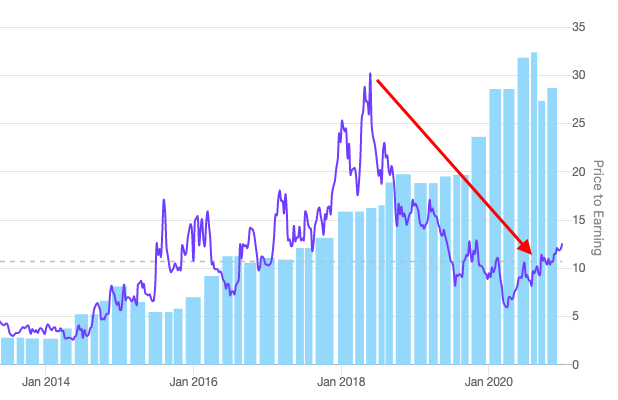

It went through nice time correction - PE went from 30 to 12 .

and price has now broken the previous 3 top resistance level -

Looks like going towards new highs if earnings keep on growing as it has been.

7 Likes

Anyone has any idea about this road show thing -

Looks like Associated Alcohols’s this Q3 result is best quarter so far in their history with Quarterly sales as 153cr and profit as 25cr as per unaudited results.

We need to wait for conf call on Monday for more details to know the reasons for good results.

2 Likes

Notes from Investor presentation:

The company achieved its highest ever quarterly Revenues and Profit Before Tax in Q3-FY21.

• The third quarter seasonally remains the best quarter, which has aided the pick up in sales and normalcy has also

been restored to pre-Covid-19 levels.

• The Plant reached 100% capacity utilisation during the quarter.

• Substantial reduction in raw material prices this quarter versus a year ago as well as improvement in price

realization of IMIL and IMFL resulted in improvement in margins.

• Company commenced sales of its IMFL products in state of Uttar Pradesh during the qua

1 Like

The company has reported fantastic set of numbers in this Quarter. I attended the earnings conference call today. Management seems competent and capable. It has a very bright future ahead. Company is planning to complete execution of capacity expansion of distillery capacity from 4.50 crore litres to 9.00 crore litres in next 12-15 months timeline. Covid delayed the expansion timeline by almost 6 months. Company is expanding in other states where ever it is finding opportunity. In this quarter it has started sales in state of U.P. Also it has become 5th largest player in the state of kerala.

Disc : Invested since 2016.

6 Likes

globus spirits is also good. posted decent q3 numbers.

Despite good balance sheet, what puts me on hold is the salaries drawn by Mr. Anand Kedia and Mr. Prasann Kedia. Both being promoters of the company, but not present in tthe Board of Directors. In fy18 they took home 4.44 Cr each (total 8.9 Cr) against net profit of 25 Cr, accounting for roughly 35% of PAT. In FY20, they took home 3 cr each (total 6 cr) against net profit of 49 cr, accounting to ~12% of PAT.

Normally, if they both were part of the baord of directors, then their salary would have to be approved by shareholders and perhaps central government (if the total managerial remuneration exceeds >11% of PAT) and so it seems they are kept out of the board and enjoying high salaries.

Perhaps, someone can throw some light here. Everything else in the business seems great.

4 Likes

So what do you find wrong with that ? Can you elaborate ?

1 Like

I don’t find it wrong, I just find it very strange that the promoters are not part of board and are taking really high salaries (as % of PAT).

Points which make associated alcohol a good investment :

- Unpledged promoter holding above 51%

- Healthy OPM,ROCE , ROE and ROA. Best in the sector.

- 100% Capex planned from current levels. Majority of the same to be funded from internal accurals. No major equity dilution, neither burden of interest cost due to debt. In the past management has already shown their capability by completing expansions in a time bound manner with financial discipline.

- Entering newer geographical areas to diversify the risk of being in a single state.

- Company working on to increase sales mix of branded products to increase overall margins in the long run.

- Company has substantial land available to the tune of 250-300 acre, so they do not have to incur additional cost to acquire land for expansion.

- Long-term relationship with United Spirit Ltd (USL) as their supplier which can give company access to global markets. ( Through USL ,company has provided ENA for europe market in this quarter as per the conversation in earnings call)

Considering above factors it seems company has huge growth potential and lower risk for long term investment.

The remuneration point that has been stated above is not a negative one to affect investment decision from equity share holder stand point.

In evaluating whether a company is invest-able or not, weights have to assigned to all the important parameters and then one has to arrive at conclusion. Randomly saying something doesn’t seem right without elaborating in detail can be a personal opinion only, not useful for any decision making purpose.

( Also there is no rule that ALL promoters have to be in board of directors, so nothing strange about it)

2 Likes

I think you probably missed reading this. I did acknowledge the fact that the companys balance sheet is good and that was the only point of concern for me. So its not a “Randomly generated thought”, a personal opinion - yes, but that is what the forum is about, to raise concerns one have and discuss about it.

I neevr said anything about it being a rule or whether it is wrong, its just strange to me that they are not a part of board and the remuneration seemed high to me as % of PAT. Normally in all the companies I have analyzed, promoters are in the board and thus the salaries are withing the limits of the companies act.

This is just for the information of other forum members, who cares to spend some time on the management analysis. In this case, I am not yet convinced and may be someone can do some study on this part and clear the air around this (?) without any bias.

5 Likes

Does anyone has conference call playback link the one which was held on 15 february 2021

I think you are correct!

I have sold my position because of this issue. But management quality in this company is very subjective as with change in management this company has started changing its way few years back. So it is upto us that we want to consider its questionable history or give benefit of doubt to new generation. Nobody doubts that it is great long term bussiness and now management is trying to meet market expectations.

My personal opinion is that: “It is worth risk taking if you find valuation in your favour.” However, management quality at present is like half glass full and half glass empty😂.

5 Likes

I had zeroed in on this stock until I came across @rmehta26 's valid insinuations regarding the promoter’s integrity.

The promoters not being a part of the “Board of directors” seems to be a deliberate attempt to circumnavigate the clause of Companies Act,2013 below.

“Managerial remuneration in excess of 11 % required government approval. However, now a public company can pay its managerial personnel remuneration in excess of 11 % without prior approval of the Central Government. A special resolution approved by the shareholders will be sufficient”.

On further analysis I found this 2013 article about the promoters forging the signature of the then Assistant Commisioner of Excise for importing raw material and had been booked for fraud.

The company seems to have potential for growth however these red flags still seems to be a big concern.

@rajeshaaidu : Thanks for your inputs on the topic, you mentioned about the change of management would improve the outlook of the company in future, however I still see Anand Kedia and Prasan Kedia at the helm of affairs in the company & drawing huge salaries disproportionate to the the PAT. Am I missing something?

3 Likes

Hi,

I have compared the management when his father use to run the bussiness and it use to be a typical Indian c… company. It was just like Som distillary controversy that time. But these people are trying to change the things but nobody can predict : how they will behave in bad time? So valuation should give me comfort to counter the negative sentiment that management integrity will cause during bad time.

However, management integrity is very subjective thing and it can be only found out during bad times and not when things are going right as now for Associate. Most of the liquor bussineses are very good bussineses with tainted management. But this can be perceptional bias also as they are in bussiness where they have to always fight regulator, health care and social acceptance.

Thanks!

3 Likes