In my view, I think the directors (Kedias) have huge amount of black money, and they are trying to convert it in good money, this is by means of inflating profits and then drawing high salaries.

This pattern is seen after 2014, demonetisation period.

Also, I noticed one more thing, I think they may have 45 MLD capacity well before 2010 (found from old AR), but they showed only 30 MLD in 2014, and by manipulating they increased it to 45 MLD again, and showed investors a different picture that they expanded.

So, in my thinking that money may had came from that 15 MLD capacity which they were hiding before 2014.

In India bad government policies is the biggest reason to incentivise black selling of alcohol, and to be honest I think almost every small alcohol manufacturing company is involved in such kind of activities.

Thanks for sharing the information.

Company Looks good and we are seeing the strong growth in previous quarter.

For me also only concern is their salary rise. This is too high. I think it will increase year on year.

Completely agree. otherwise ENA and bottling business does not have much margins . They don’t any strength in branded imfl segment. Country liquor is also not much lucrative . Company can make this kind of profits through seconds business or duty evasion .

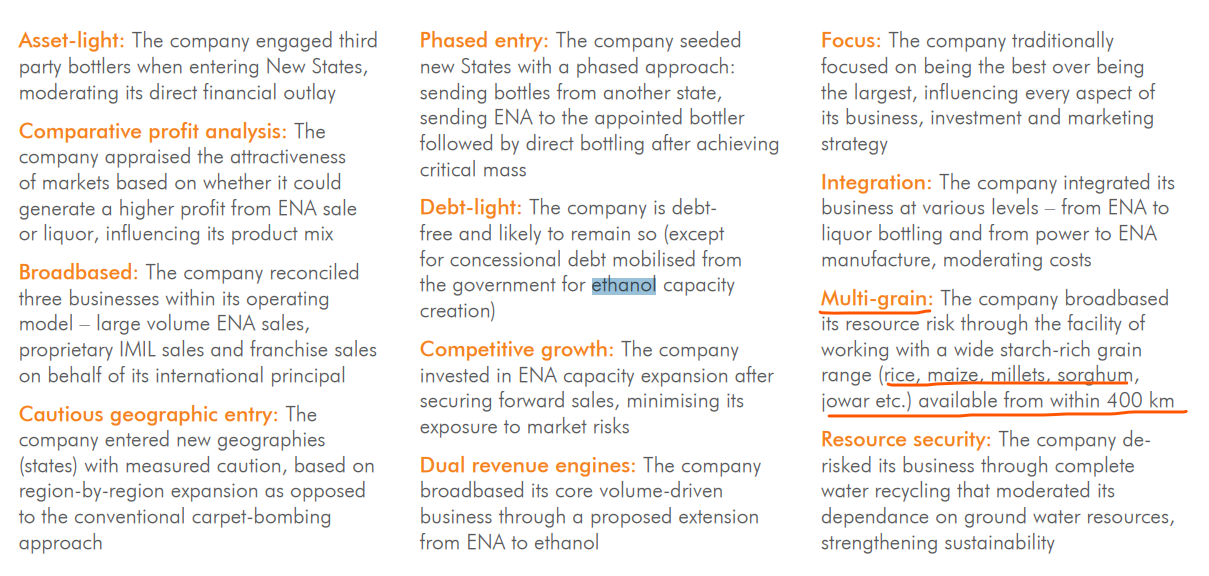

Civil work for expansion has started it states. Also, equipment procurement is finalized with Praj Industries Ltd and other vendor agreements are also under finalization stage.

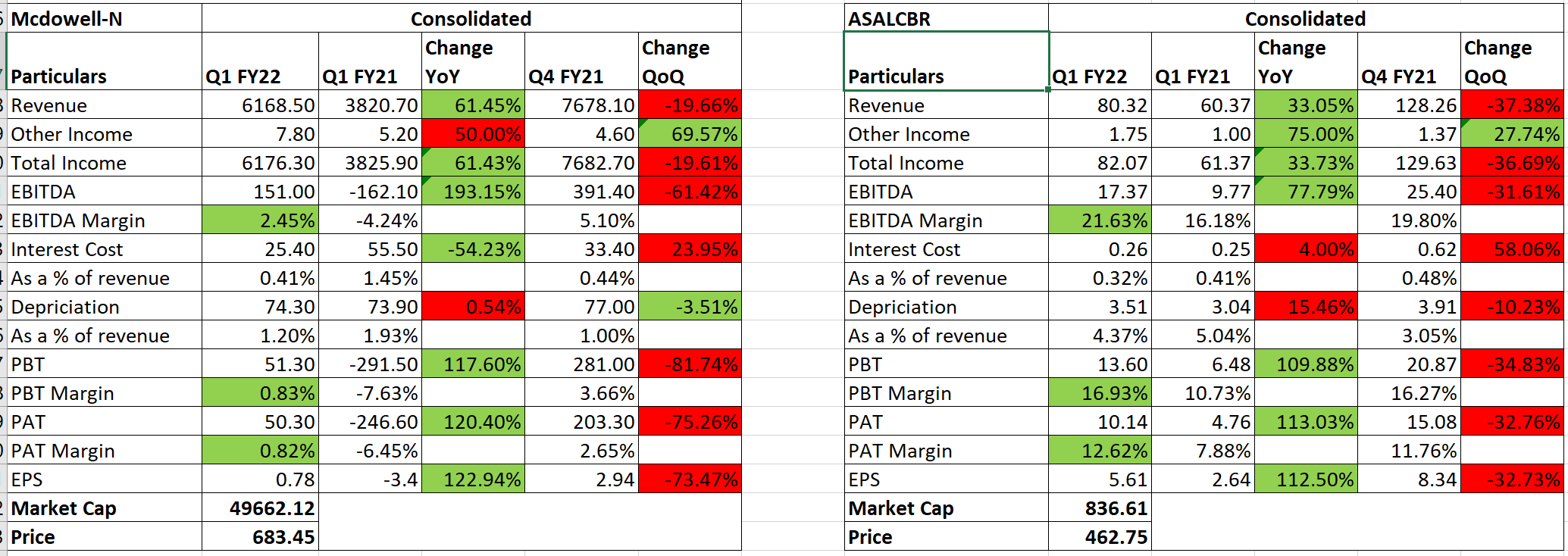

Results of Mcdowell-N vs Associated Alcohols & Breweries Ltd.! The Mcap/Sales differs a lot. The profitability also differs.

Disclaimer: Not a buy recommendation, Tracking

Sales has increased to 120.61 cr from 80.32 cr in June 21 and 103.35 cr in Sept 20

PAT has increased to 14.26 cr from 10.14 cr in June 21 and 13.17 cr in Sept 20

Company has cash reserves of Rs.89 cr as on 30th Sept 2021.

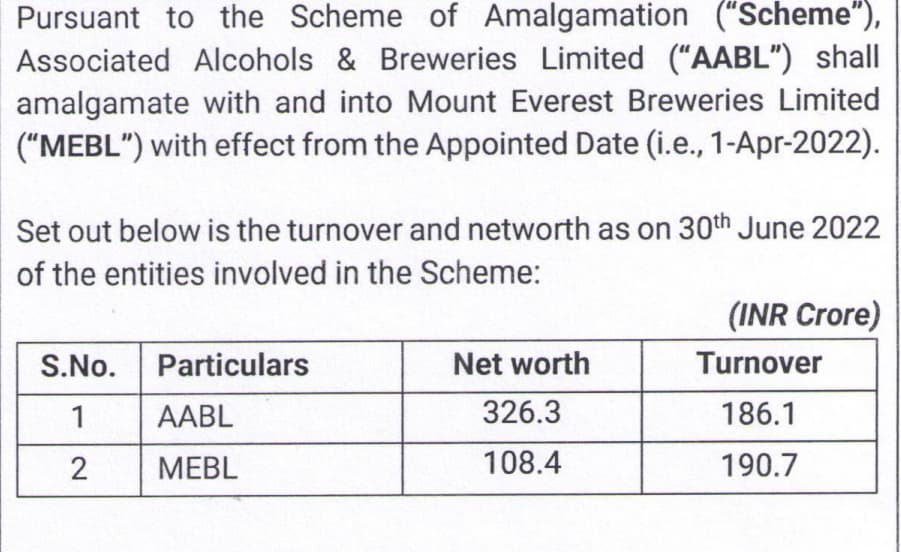

Management is exploring the merger/amalgamation with Mount Everest Breweries Limited. It should also further add to expansion plans. CARE Rating report states it is promoted by Kedia Group.05032021071224_Mount_Everest_Breweries_Limited.pdf (787.0 KB)

I was going through the quarterly results and found something amusing. Excise duty expenses have been really low in last 9 months compared to previous years. Check the screenshot of the latest quarterly resuIts. If the image is not readable, here is what I’ve highlighted.