Guys, Whoever able to attend conf-call, please pose the deep discounted ESOPs issued reasoning? Grill in detail. And ask to correct it.

Thanks.

My earlier apprehension was that the ESOP might be given to management personal who are part of the promoter group. But then I came across this link:

“As per Company Rules, only (i) a permanent employee working in or outside India; (ii) a whole-time or part-time director of company; and (iii) an employee of a subsidiary (whether in India or abroad), holding company or an associate company, can claim benefits under an ESOP scheme. It is absolutely important to note that neither a ‘promoter’, nor a director holding more than 10 per cent of the equity shares of the company is entitled to take part in this scheme.”

So I guess the promoters(J Patel/Alok Patel) are not taking the ESOP. I wonder why would the company would like to dilute equity at such discounted price for human resource. We should ask in the concall though.

1 Like

Employee cost % revenue (consolidated, fy17)

Arman = 19%

Ujjivan = 20%

Satin = 22%

I do not see a major difference in the employee cost of Arman.

I don’t see a major issue with the ESOPs. It is just 97500 shares and that too to be vested over 3 years. Even at the current market price, the net effect on employee cost comes to around Rs 50 lakhs/annum. In my opinion, its no big deal and will go a long way to retain key employees.

I agree that material impact is not much. But the question is on intent of management to dilute equity at such steep discount. Management should have used other tools in the arsenal like performance bonus, high salary, etc. My only contention is option price and dilution of equity at discounted price which clearly could have been avoided.

How are deeply discounted ESOPs an issue? ESOPS are issued to firstly incentivize the employee and second to ensure his loyalty to the company for at least the period before exercise. If the ESOPs are not well discounted from CMP, both objectives would not be met.The employee can just buy from the market and move on from his job, in that case.

2 Likes

ESOPs vest at a future date on vesting price. Vesting price is fixed when ESOP are issued.On vesting, employee has an option to pay the vesting price and take the shares or not pay the price and leave the shares.

If management & employee are confident about the present price and future prospect of the company they will generally issue the ESOP at the closing price of the day.

Have a look at ESOP issued by IndusInd bank at this link. You can also look ESOP given by other good companies like Infosys etc.

Issuing ESOP at Rs. 50/- when market price is 190/- shows the lack of confidence of management as well as employees in there own company & future prospects thereof.

It is a small company with more uncertainties than an IndusInd Bank. Surely, it is reasonable for the management to offer a much higher upside to an employee and also provide a good margin of sfety? Do keep the objective of ESOPs in mind when deciding whether such a move reflects low confidence of the management or a move to offer their employees higher upside/margin of safety. Getting IndusInd Bank at today’s market price 3 years hence seems like a a decent deal, and most people would assume IndusInd’s price to be decently higher 3 years hence. But there is a lot more risk with a tiny player like Arman, therefore there is no such (relative) certainty in the mind of the employee. Hence he needs an incentive to know that he has a big margin of safety on the ESOPs. There is no shortage of NBFCs that will hire employees with prior experience, so I think this is a reflection of the company’s smaller position and other realities.

To be frank. I am not invested in Arman and never was - this is purely an academic input based on various experiences I have had (professionally) with respect to ESOPs.

So I attended the concall today and asked about the esop options. Here is what Alok Patel said: they are aware that this was a tricky issue and acknowledged that there was deep discounts. But these options are for mid and district level employees. Some of them are on low salary bracket so they won’t be able to pay higher amount. Also, after the three year vestige, there would be additional lock in for one year. But he was open for feedback and suggestion.

Other notes:

-

MSME: although they did not give guidance for aum, their target for msme business is 80 crore for this year. Currently, they have disbursed 9 cr of loan and have 2500 client. The average loan size is 50k to 1.5 lakhs. These are unsecured loans. They take pdc cheques and there is a guaranter for the loan. Cibil check is done for the borrower, guaranter, and spouse of borrower. They are still lending conservatively as they haven’t finished one cycle of lending and collecting. They said 25 branches will be open for MSME.

-

Microfinance: they acknowledged the headwinds in the business. Although, they are still positive on the sector and growth rate. They want to restrict the business to 50% of loan book. The collection have actually gone up in UP after the loan waiver. Business is back to normal. They will do minimum disbursement of 60 cr this quarter and the number can only increase. They said they will beat this number. They have assured that they will try to collect from those who haven’t paid. They don’t want to expand microfinance business in Gujarat and will plan to expand in UP, Maharashtra and MP.

-

Demonitization: Jayendra Patel said that such crisis come once in every five years and they have survived for twenty five years. He said the company has faced the crisis beautifully and they have emerged stronger. Business is back to normal and there is no effect of demonitization anymore.

-

Cashless: they have acknowledged the change in this massive trend and taken strong measures. As a pilot they have started to disburse the money in UP through NEFT

-

AUM guidance: they did not give any but they said they will get back on this

Discl: invested

8 Likes

quite satisfactory and logical answer.

2 Likes

I don’t find it satisfactory though. It looks more like they didn’t had any other answer for it. Mid and district level employees and their salary is in low bracket is questionable. When stocks are given to employees they do communicate their worth and when the company is already listed everyone knows the worth already.

Why did they not gave less quantity at higher price ? The total worth of the stocks communicated can be managed that way too. And as per my knowledge the vesting period is usually for 4 years only, so additional lock in doesn’t make much sense either. May be it varies for company to company, but still I think this was not appropriate on management part to offer deep discounts.

ESOP means issuing stock at a discount to market price. Higher the discount, greater the profit for employee. Hence a low issue price simply means a guaranteed profit for employees at the expense of shareholders. I hope this answers your question “Why did they not gave less quantity at higher price ?”. Less quantity at higher price will be a double whammy.

Of course a low issue price still indicates a low confidence towards future price.

1 Like

Loan waiver off announced by Maharashtra Government. Any impact on M/s Arman’s revenues ?.

I find it quite ok. ESOP’s mean that when they mature employee has to payout that much amount. For larger companies these payout’s are funded by NBFC’s in form of ESOP funding. The employee uses these funds to vest the share and then sells them, books profit and repays the NBFC.

My assumption here is management thinks that:-

- Employees won’t be able to give the downpayment for vested shares

- NBFC’s may not fund employees at district levels.

Regards,

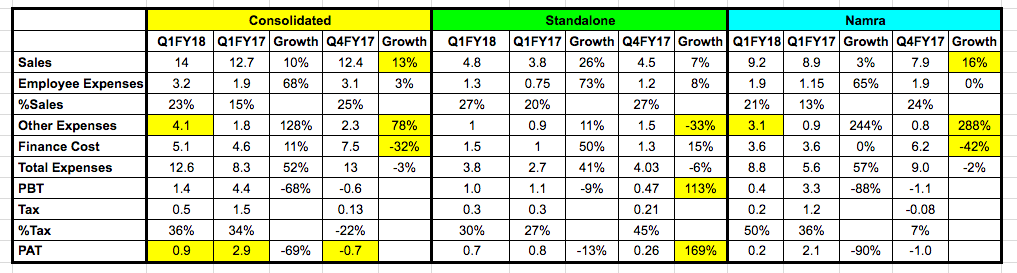

Another bad quarterly result for Arman →

- Two wheeler financing business was saving grace at consolidated level in Q1FY18.

- Other expenses increased for Namra on both QoQ and YoY basis. This seems to be due to provisioning for PAR (portfolio at risk) accounts.

- Finance costs were brought under control for Namra and hence it managed to report some profit.

Results Link →

http://www.bseindia.com/xml-data/corpfiling/AttachLive/843c533a-8138-43ac-8fcb-fbad03d1d37e.pdf

The provisions should be check for which quarter. Ujjivan said their provision increased for the loans they gave in November and December. Arman had clarified that they had stopped lending completely during that quarter.

Bad numbers though.

while yoy numbers as expected was bad but the sequential quarter trending is good

The company came up with their press release and the concall was very good.

Some points:

-

Total AUM: The AUM of the company was Rs. 229.3 cr which is a growth of 21.19% compared to last year.

-

Increase Cost: The increase was on two fronts: branch/employee cost and provision. The company expanded rapidly as far as branches are concerned especially in UP. Their collection figures in UP are the best and they are also trying to occupy the space vacated by other MFI. Provision increase because of demonitization and they said that most of the pain is behind us. Collection for new loans is in the range of 99% and discipline is intact

-

MSME: They have a target of Rs. 75-80 cr disbursement this year for MSME. The ticket size is Rs. 50000- Rs. 100000. These are very high interest rate loans and are more expensive than MFI loans. There is a constant month on month increase in MSME disbursement and the focus is in Gujarat and MP. They are not launching MSME in UP.

-

AUM 3 year Targets: Alok Patel reiterated that they are on track for Rs. 800 cr AUM till 2020 and by Q1 or Q2 of 2021 they should have an AUM of Rs. 1000 cr.

-

Credit Rating: They are not going for any upgrade of their debt because of the current environment in the sector. But their safeguards are working and they would be going for an upgrade of their credit rating once things settle down. Currently, they are borrowing in the range of 14% approximately and this year they might try to get it down given the cut in interest rates. 60% funding is from banks and rest 40% is from NBFC.

-

Loan Book: They are making an effort to increase the disbuserment of 2 wheeler financing as they dont want high dependence on MFI portfolio. So the targets for this year have been revised upwards for 2-wheeler financing.(sorry could not track actual number that was given in concall).

I will post the transcript(or main points) once it is published.

Thanks,

Kunal

4 Likes