Where did you see that? The company has published Shareholding Pattern only up to Quarter Ended 30th June, 2016. And for that quarter it has gone down from 28.81% to 28.1%.

1 Like

there are regular disclosures on bse

Thanks for guiding. ![]() But a promoter buying just around Rs.3 lakhs worth of company’s shares does not mean much.

But a promoter buying just around Rs.3 lakhs worth of company’s shares does not mean much.

quantity hardly matters…

if he’s buying he sees value…

1 Like

Interview by Alok Patel.

Here are some points:

-

Collections are up to 95%. The shortfall of 5% is in isolated rural areas where there was no bank presence or big liquidity crunch. Mostly, milk belt of Gujarat where dairy farmers are not getting their dues.

-

Collections went as low as 70%.

-

Confident that from Jan 1st things will be back to normal

-

Demand is very much there for credit. Rural India is not use to cashless economy.

-

Three distinct portfolio:

a. Two wheeler/Three wheeler segment has taken ten percent hit. (Pre Diwali 10 cr dis. to 5 Cr in Nov)

b. SME segment has taken 20% disbursement hit, but portfolio small

c. Microfinance has taken maximum hit and has come to standstill. (From26- 28 crore dis. in peak now the disbursement has come to 1cr.) -

Conservative approach was taken proactively by management when it came to disbursement to understand the effect of demo

-

If withdrawal limits are removed, then the company can go to peak level disbursement rate in weeks.

-

But the company is sceptical of normalcy for the next three months.

-

Expansion plan of branches have been on hold. Starting Jan they might continue. Understanding the situation in Maharashtra and UP where some places have issues.

-

AUM growth post demo target was 15-20%. Will try to cover ground in the next two to three quarters

-

Cash and digital mode: Did not answer question on split between cash and digital disbursement. Said lot of education will be needed by MFI to customer as many clients have never written cheque, have no cell phone, etc. Repayment is expected in any form like pos machine, cheque, etc. Most customer still prefer cash route.

Thanks,

Kunal

13 Likes

Thanks for sharing.Very sensible management commentary. No hype.

Hi all,

I just wanted to understand valuation of microfinance on Market Cap/ AUM metric. Would it be fair to say that if a firms market cap / aum is less than 1, it is undervalued as far as microfinance firms are concerned.

Or what is a fair market cap/aum metric for microfinance firm?

Armans market cap is currently in the range of 130 crore whereas AUM is nearly 220 crore.

After demonitization, other microfinance firm are trading on par with their AUM. Like Bharat financial has market cap of Rs. 10330 cr and AUM of Rs. 8531 cr.

Also, most of the stocks of microfinance companies have recovered apart from Arman Financials. Would it be fair to say the market is mispricing this stock compared to other microfinance stocks purely on Market Cap/AUM ratio?

Results of December quarter:

Lots of interesting facts about results in the press release

Kunal

Does anyone have the transcript of the concall? Or Can someone share the notes of the concall if attended ?

Q3 Concall – a few points

On Business:

-

We have made Rs.1.6 crore extra provisioning on Standard Loans this quarter which is a one-time hit. It is included in Other Expenses. Recourse to extra 60-days granted by RBI is not relevant in this quarter; it will be applicable in Q4. We will see at that time whether to use it.

-

New product SME loans introduced, pilot launched. Here average ticket size is Rs.82,000. Yield around 28 - 32%. This is a totally cashless business. Here risk is higher, we are expecting higher NPA, and so pricing is also higher.

-

There is no competition from banks at all. They are in a totally different mode and cannot do what we are doing. At the most, they tie up or acquire MFI.

-

Long run growth of 30-40% is absolutely possible going ahead

-

Expect a crisis every five years! We are confident we will be okay.

On Mudra:

It (doubling of the amount in Budget) is not a budget but actually a target. It is not that the Central government has allocated that much money under Mudra. We do not read too much into it.

On Demonetization:

-

Currency situation has mostly come back to normal except a few isolated places where there is still some liquidity crunch. We are expecting the situation to come back to normal by April or May.

-

Throughout demonetization, lowest overall repayment rates never went below 80-85% and at branch level, 40%. Cumulative repayment is now 94%.

-

People are gradually accepting cashless, psychologically the resistance is going down. Clients are ready to go to ATM, micro-ATM etc.

On Politics & Loan Waivers:

-

Political interference was there in a few individual pockets, that too mostly from local small time politicians. It has mostly died down now.

-

Confident that loan waiver will not come. Even if it comes it is not enforceable as we are regulated by RBI. The governments will have to repay us from their own funds.

-

Risk of loan waiver and political interference is an inherent part of our business; we are living with it since beginning.

Miscellaneous:

Micrometer, which is published every quarter, provides a lot of data on the industry.

(Others may please add / correct if there is an error in my listening or understanding)

12 Likes

Arman Financial: Conservative management exploring growth opportunities in difficult times!

2 Likes

any news on Arman anyone may have,would be helpful

Bad Results by Arman →

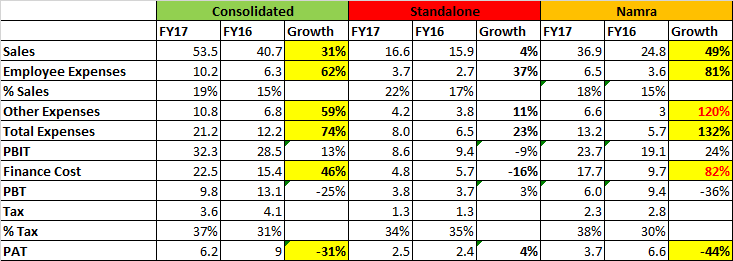

-

Employee expenses increased 81% for Namra. This might be treated as expected due to branch expansion and lower growth due to demonetization. This number will look okay in coming quarters as branches start churning out business.

-

Other expenses increased 120% for Namra. Although company was planning to build additional provisioning reserve, this number is higher than my expectation. Looking forward to understand this more.

-

The finance cost of Namra grew 82%. This again is a higher than my expectation. The ST borrowing increased by 9Cr and LT borrowing increased by 2Cr. Due to this, 24% growth at PBIT did not translate into PAT growth.

Disc - I hold, this is not a buy/sell recommendation

2 Likes

Dear Mr Rupesh, Trust the demonetisation had little impact on Q4 financials.

Arman Press Release →

https://nseindia.com/corporates/corpInfo/equities/AnnouncementDetail.jsp?symbol=ARMANFIN&desc=Press%20Release&tstamp=300520171951&seqId=101824337

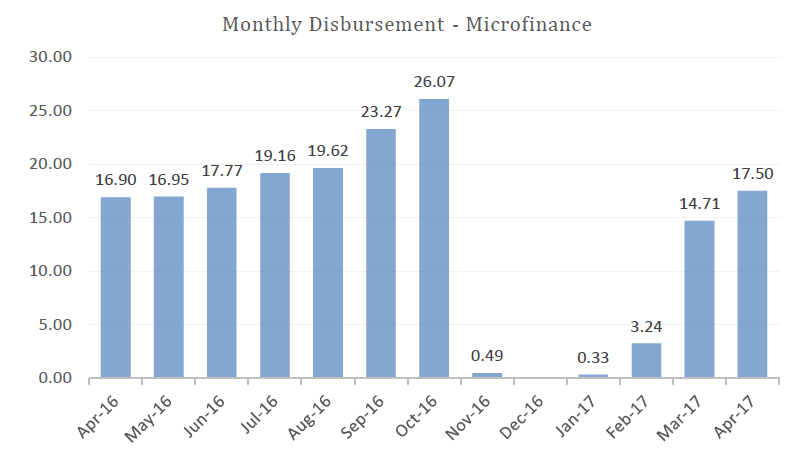

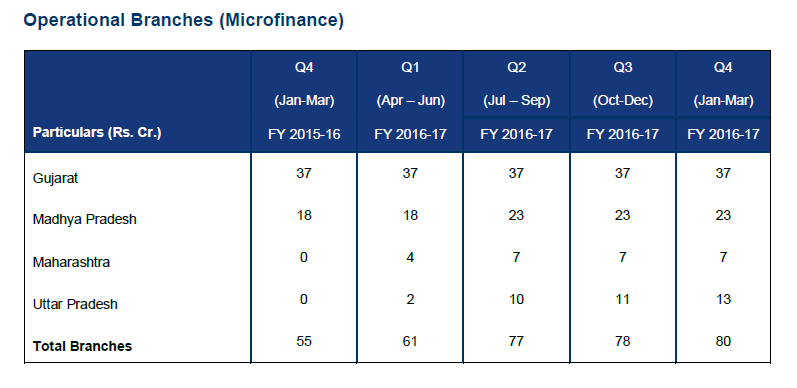

Interesting things to note →

No/Minimal disbursements from Nov to Feb

Branch Expansion

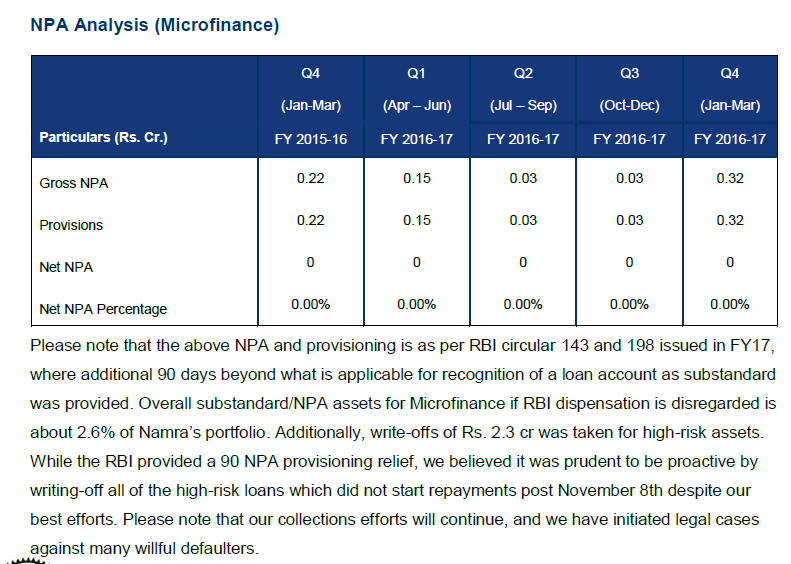

Write-offs in MFI business despite relaxed guidelines from RBI

2 Likes

Given the rationale given by the company in the press release, I am comfortable with the results the company has posted.

-

Stopping Disbursement in November- Feb: This was an extremely bold call by the management and I appreciate that they had the courage to take it. During times like these when other companies were chasing growth, company showed wisdom by focusing on protecting the capital.

-

Going Cashless: I am slightly disappointed here because in the last quarter they cited reasons as to why they should not be going cashless. Main one was the interest getting charged on the same day when the amount was credited to client. The other reason was “no bank” accounts for the customer. Now they have said that they are pushing for cashless aggressively through banks.

-

Diversifying: Although, they have on previous occasions said that they want a more diversified loan book, the future guidance was on the assumption for robust growth for microfinance. We need to check if they still maintain the same guidance with new products like MSME loans.

-

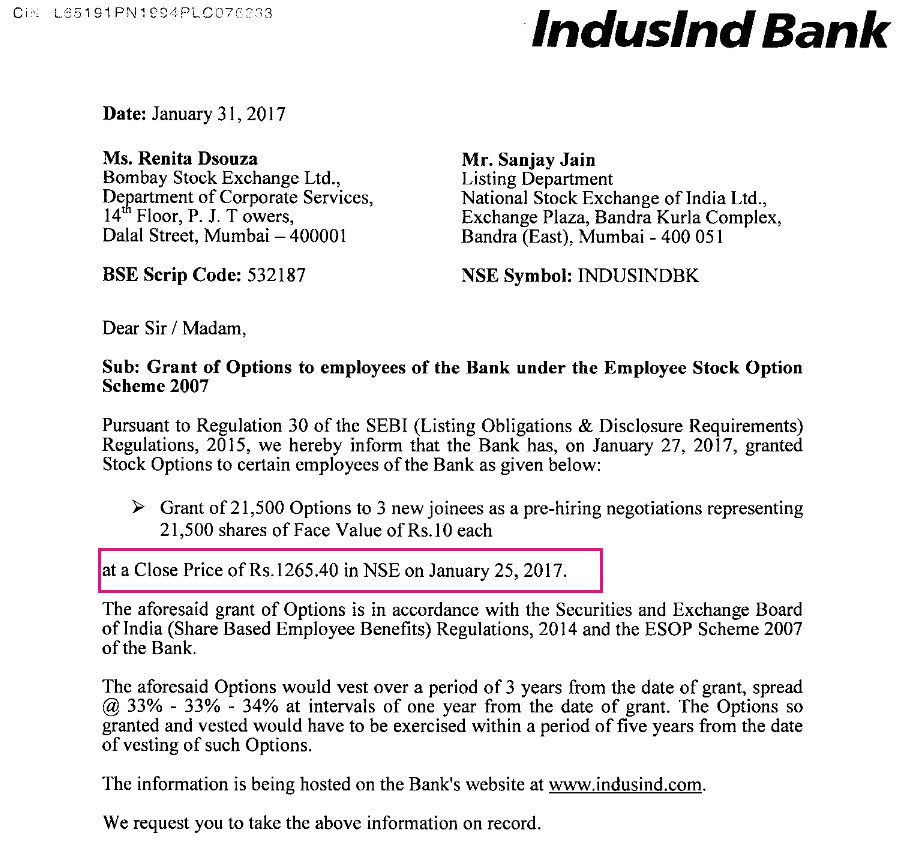

Options: They have granted options of 97500 stock with an exercise price of Rs. 50. These are employee stock option which will get vested in 2018(30%), 2019(30%) and 2020(60%). I am concerned that the options have been granted at a steep discount. What do others think?

-

Expansion: The company in its press release has not spoken about expansion of branch networks. They did mention about increasing the MSME loan book, but what are the plans for expanding Microfinance business. Their immediate focus has been mentioned which is to get the disbursement level at pre-demonitization level. But what is their overall outlook for microfinance sector as growth rates have fallen substantially.

Discl: Invested.

2 Likes

Yes, no doubt they have been given at very deep discount. I think they have been given at unjustified and unfair price. I have written to the board to re-consider its decision.

I could find these Sebi guideline for grant of options

http://www.sebi.gov.in/sebi_data/attachdocs/1291177727828.pdf

We need to study these deeply to understand, if they were followed in this case.

Disclosure - Invested. This is not a recommendation to buy/sell.

1 Like

Taxing of ESOP

ESOPs are taxed at 2 instances –

At the time of exercise – as a perquisite. When the employee has exercised the option, basically agreed to buy; the difference between the FMV (on exercise date) and exercise price is taxed as perquisite. The employer deducts TDS on this perquisite. This amount is shown in the employee’s Form 16 and included as part of total income from salary in the tax return.

At the time of sale by employee – as a capital gain. The employee may choose to sell the shares once these are bought by him. If the employee sells these shares, another tax event happens. The difference between sale price and FMV on the exercise date is taxed as capital gains.

Source - www.cleartax.in

ESOP generally issued at Closing Price of the day

Issuing ESOP at such a deep discount manifest that management themselves is not confident about the business, which is quite negative. Even when we know that business is doing just fine.