Taxing of ESOP

ESOPs are taxed at 2 instances –

At the time of exercise – as a perquisite. When the employee has exercised the option, basically agreed to buy; the difference between the FMV (on exercise date) and exercise price is taxed as perquisite. The employer deducts TDS on this perquisite. This amount is shown in the employee’s Form 16 and included as part of total income from salary in the tax return.

At the time of sale by employee – as a capital gain. The employee may choose to sell the shares once these are bought by him. If the employee sells these shares, another tax event happens. The difference between sale price and FMV on the exercise date is taxed as capital gains.

Source - www.cleartax.in

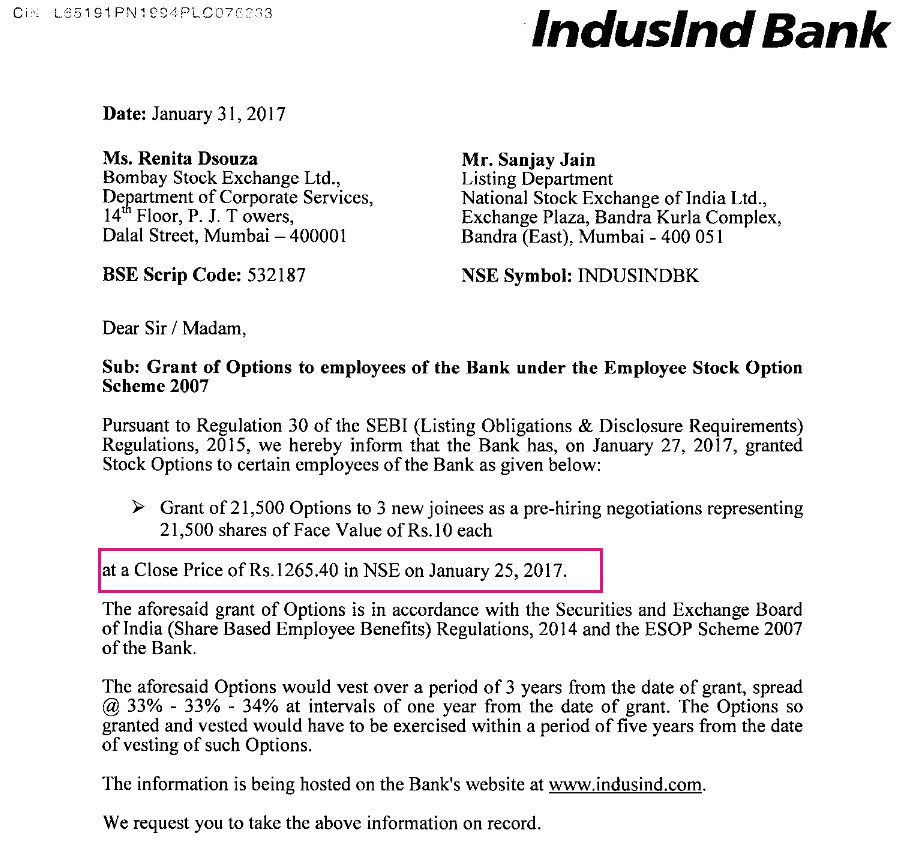

ESOP generally issued at Closing Price of the day

Issuing ESOP at such a deep discount manifest that management themselves is not confident about the business, which is quite negative. Even when we know that business is doing just fine.