0db0ec9a-a09f-416f-a485-8af43aae2ed2.pdf (395.7 KB)

Board has sought approval to merge class A share in ordinary shares.

0db0ec9a-a09f-416f-a485-8af43aae2ed2.pdf (395.7 KB)

Board has sought approval to merge class A share in ordinary shares.

Any idea how the valuation ratio of 65:100 has been arrived at?

arman no. of shares after conversion of Class A shares to ordinary will be 65L. plus 18.9 L saif capital shares. so total 84L shares.

q2 eps works out to 6.44. h1 is 12. full year they should do about 27-28. as per them they are well funded in equity for next 1.5-2 years with the saif capital capital and would be able to maintain 40-50% growth.

as of sep 30

LT borrowing is 281cr

ST borrowing is 43.5cr

they have shown OCL of 163cr, which (my guess) would include 50cr of ccd. adjusting for this (exclude it from liabilities and show under networth), total borrowings are 437.5cr

networth is 66.6cr plus 50cr ccd = 116.6cr. so total d/e is 3.75. they have some more room to borrow for their growth.

loans and advances has increased from 421cr to 517cr, by 23% in H1.

CCDs must be included in LTD, rather than other liabilities.

Possible. They had mentioned in one of the concals that it will remain under OCL. hence my calculation.

Lets say, it is part of LTD. OCL is mainly current portion of long term borrowings (as per AR, 123 cr out of OCL of 130cr was this component). So we take the entire OCL value (conservatively) and remove 50cr from LTD for computation of total borrowings.

We will have a better picture tomorrow with press release and concall. Current Equity is around 118 Crs including CCDs.

I agree with your point, 650 Crs AUM by FY’19 is easily achievable and I think they should be able to grow to 1000 Crs AUM sometime in FY’21 without diluting further. Current year PAT should be around 20-22 Crs. Assuming 60-70 Crs PAT in FY’20 and 21 should see net worth around 200 Crs. Even a modest debt to equity of 4:1 is sufficient for 1000 Crs AUM by FY’21.

as investors, we should just keep our fingers crossed against demo-like events in future.

Status: invested

arman commentary. makes for v good reading…

hello

what is the reason for decline in promoters holdings?

Dilution. Expected more not only Promoters but also non-promoters.

Hit: So, need to think on valuation.

I have 1 question about #armanfinanciala.

Why promoter shareholding decrease.

Any reason behind it.

SAIF has invested by CCD turning into shares, in October 2019 they were given 25% holding NET. This means actually 35% extra shares were issued and this means promoter holding of 40% turns into 28% automatically, NOT SOLD off. Some minor 0.8% holding has been sold-off by some promoter family group members.

Yes sir just searching all things about it and nice to see that company doing well and yes they playing good role in expanding customer base.

Great results by Arman yet again- https://www.bseindia.com/xml-data/corpfiling/AttachLive/ea17e3f0-f1bf-495f-be26-1046bf84727e.pdf

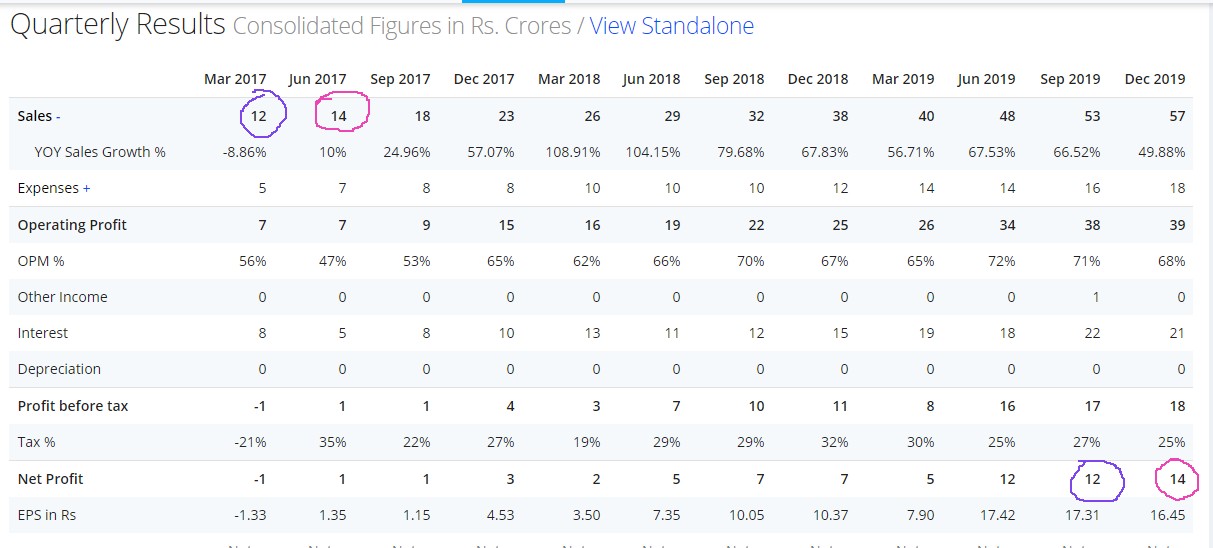

Q3FY20 revenues increased by over 50% YoY to 54.5cr from 36.2cr in Q3FY19

PAT increased by 88% to 13.5cr from 7.2cr in Q3FY19.

Their press release provides information on their AUM and provisioning. AUM increased by 40% from 580cr to 814cr. MFI GNPA is at 0.9% and NNPA at 0.1%. The main highlight is their MSME business that is gaining a lot of traction. AUM increased by 72% to 133cr in their MSME portfolio.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/07244f46-0ec9-49fe-bb84-db1b5469bc93.pdf

MD’s commentary- “Asset quality continued to be robust and steady vis-à-vis last year as well as on a sequential basis. Considering the current economic climate and rural slowdown, we have adopted a conservative stance by recognizing a higher level of provisioning in the microfinance book. Furthermore, we have also raised the standard provisioning on the MSME book to 1.0% from Q3 FY20 onwards as compared to 0.4% earlier. This is not due to any deterioration in asset quality but purely a prudent measure by the company. Both measures increased the overall provisions cost by ₹ 1.6 crore over-andabove the statutory and ECL requirements.Being mindful of the prevalent macro-economic headwinds, especially in the rural segment, we have temporarily slowed down our disbursements in microfinance, while also continuing to maintain sufficient cash reserves for two months of operations. Moving ahead, we remain confident of sustaining our positive growth trajectory, by focusing on scaling up our business in a calibrated manner while prioritising the quality of our book and profitability.”

Couple of interesting observations:

Disc: Invested

Would like to hear views, after being thru the results declared yesterday

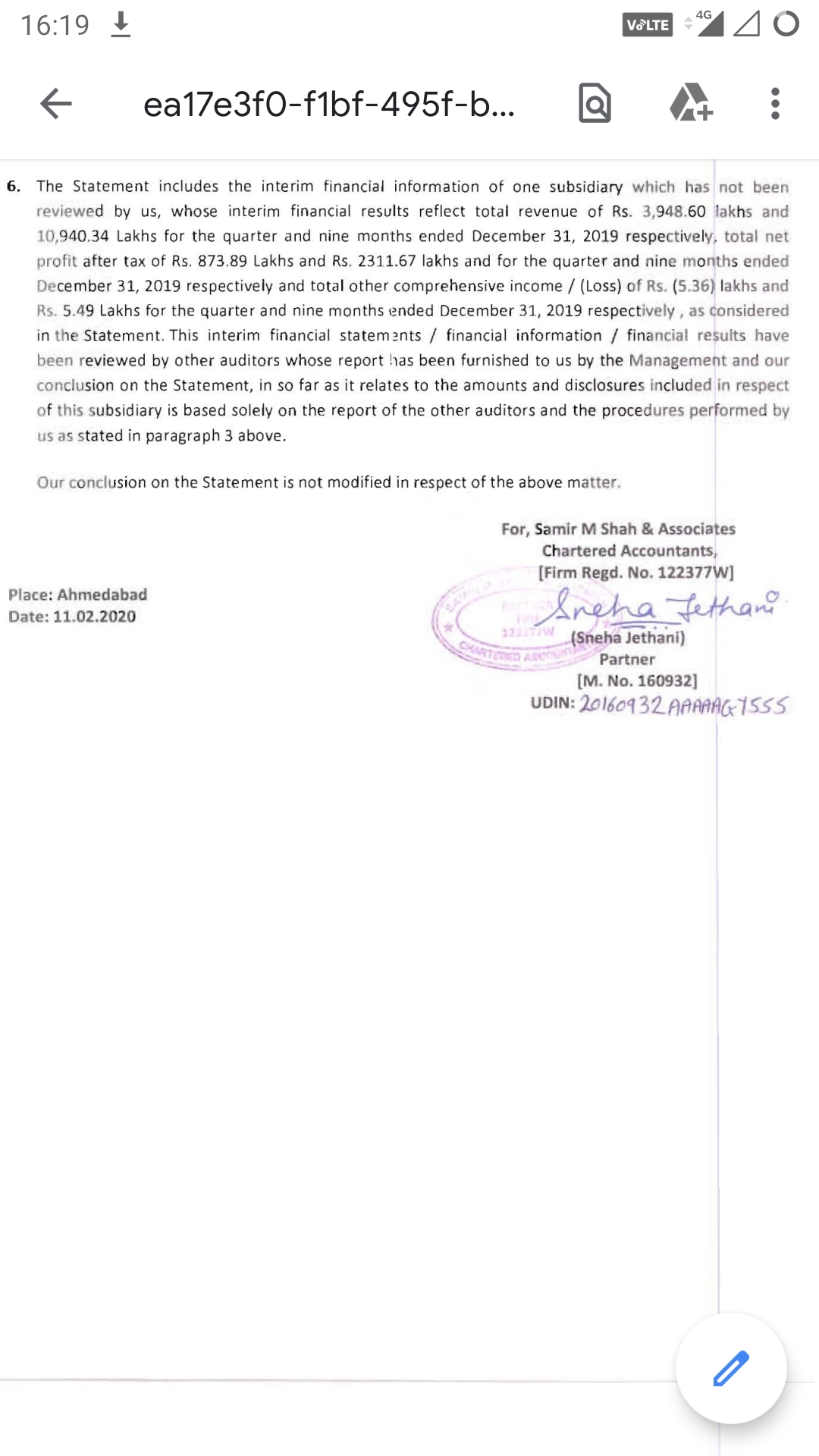

Auditor, Samir Shah has mentioned ( refer screenshot) that the limited review done by them does not cover subsidiary which has the bulk of revenue & net profit consolidated at the listed company level, surely a red flag !!

Screenshot_20200213-161932|281x500

I also see promoter holding going down, consistently, and little/ nil FII,DII interest in this company inspite of a secular run

Disclosure: not invested, watch category

Its hard to do a full review of the subsidiary Namra. Need a lot of field visits and is a costly affair that involves travelling to branch offices. Promoter shareholding is down due to change in capital structure not because they were selling.

Surely, some auditor ( not the main auditor, Samir Shah) has been auditing that important subsidiary, or are we saying no one is doing it, due to cost concerns. All the more disconcerting

1)Promoter holding down because of SAIF CCD conversion and not bcos of sell off

2)FI /DII get interested beyond a particular size ,it was too small a size ,now its close to 1000 cr market cap you will have interest coming in .Having said that SAIF,Mukul agarwal ,Amit Mantri etc are already invested

3)In limited review Subsidiary may not be audited ,its definitely audited in full review

Will this valuation sustain under current scenario?

I think too heavy lifting happened on this scrip fro past 1 month…Seniors can throw light on this

Yes the share price have gone up too fast to soon but you need to see this along with the current PAT and what they are going to do in future.I normally follow the underlying business and how the leading indicators of the business is showing up than the share price ,hence cannot comment on the share price /valuation .

I have done lot of research on this stocks ,met the management many times in last 3 years ,have worked in the field (to see their underlying processes ) in remote branches and villages . Have also attended a JLG meet and have interviewed few village women .Being a CA and also having myself run businesses in the past as CEO in different countries ,I can reasonably say that their PAT in next 2 years would be cross 100 crores if no black swan event happens (last year their PAT was only 21 cr) .Now if you put that context in mind where the PAT grows from 21 cr to 100 cr in 3 years (CAGR of approx 70% pa ) and then even if it grows at ROE of 30% post 3 years ,market will recognize this sooner or later .

I am attaching my last note of my field visit ,you can go thru the same (refer page 5 in both the link .

http://www.mydigitian.com/wp-content/uploads/2019/11/Newsletter-Oct-2019-compressed-1.pdf

http://www.mydigitian.com/wp-content/uploads/2019/12/Newsletter-Nov-19-compressed.pdf

Day before yesterday , JM financial came up with a buy report also ,you can go thru.

{kind=link}