I could speak to one of the promoters’ sons in Gimatex last night (Donald - saw your post this morning only, however will ask him for more references if he can provide). Gimatex is from the Mohota group which has been in the textile industry for five generations now. They’re present across spinning, weaving and processing; however, their forte is high quality spinning. The guy I spoke to is relatively new in the business, but still gave me a few good insights.

Here are a few salient points from the conversation:

1) Spinning & Counts

"We do cotton yarn in the count of range 60, and upto a maximum of 80. The bread and butter of most companies is counts in this range and its a good growing segment. Whatever type of spinning you use, you can manufacture cotton yarn in this range (<60). However, if we stretch, we can manufacture yarn upto counts of 80.

For yarn with a count > 80, you need specialized machines, greater levels of moisture (created through machines), controlled temperature conditions (again, created through machines), more power etc. It is not easy, and you need a fair bit of specialization, technology and know how. If I have to enter the finer count cotton yarn segment (even with the decades of spinning experience in my organisation), it would take me atleast 4-5 years to come upto terms with both manufacturing and marketing (Will come to the marketing part later). However, I am not interested in entering this segment because the growth has kind of stagnated in Europe and USA. In India, there are not more than 10 players in this segment, and Ambika is certainly the leading name"

2) Why does a player like Ambika not forward integrated into manufacturing of grey fabric and finished fabric

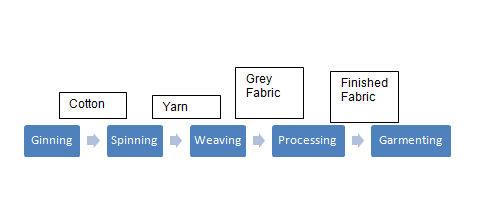

"For this, I will venture into the textile process:

So, each of these processes is an industry by itself.

Spinning - High capex, low labour, no environmental norms for starting.

Weaving - Medium capex, high labour intensive, environmental and discharge norms in place. Besides, weaving for high quality / fine count shirts does not take place in India - Turkey and Italy are hubs for the same

Processing - Medium capex, high environmental and discharge norms serve as a major entry barrier (lot of water & chemicals usage)

Garmenting - Highly labour intensive

So why can’t / won’t Ambika forward integrate? Well, first because of labour and environment issues. Second, to the segment it serves, manufacturing takes place in other countries and not India because of the quality required (weaving has various processes in itself). In yarn, it is easy to outsource and buy from other countries. However, when it comes to fabric for premium shirtings, conditions have to be controlled and a lot of manufacturers prefer to process in-house. However, its possible for a player like Vardhman to do this. Third, yarn can located at far off location as procuring it is not a problem. However, delivery schedules are extremely critical in procuring grey fabric and finished fabric. For this reason, players prefer to manufacture fabric themselves or outsource to locations closer home."

3) Marketing

"Yarn is sold through agents to fabric manufacturers and the payment is received from manufacturers directly. However, finished fabric is sold through intermediaries to end users and payment is received through these intermediaries (Dalals). You do not know where your finished fabric lands up.

Normally, fabric manufacturers do not ask for the yarn of a particular company, except for specialized organic yarn. If, as you are saying, Ambika’s yarn is specifically asked for, its a big deal."

4) More questions

I asked him to find out

- Ambika’s reputation in the market

- More about other fine yarn manufacturers and why Ambika enjoys the reputation it does

- More entry barriers for the fine count industry

- Growth and demand for higher count yarn

Will add Donald’s request for more references and will drop him an e-mail.

-

-