Two most imp takeaway from Toxhong, textile company listed on HK exchange

- China is losing its competitiveness, companies moving to Vietnam

- Ambika policy of producing only against firm orders, prevent it from yarn price fluctuations.

Two most imp takeaway from Toxhong, textile company listed on HK exchange

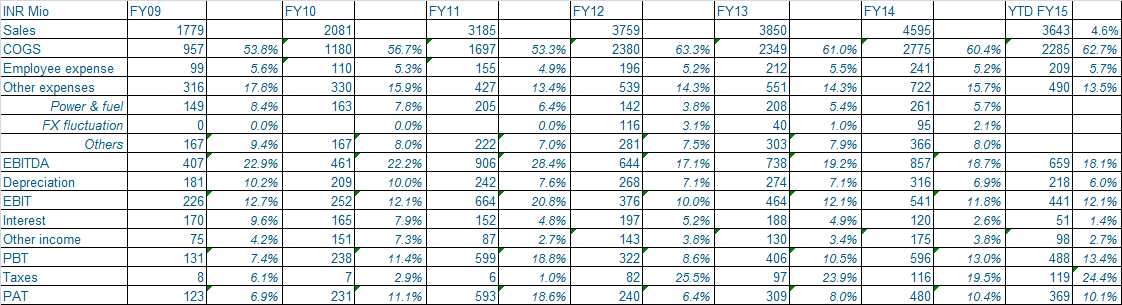

@anil1820 Hi Anil, What is the source of your data for Ambika? The RM cost looks off by quite a bit. Its around 60% in FY14.

Also would be good to know how did you get data for Premier and Thiagarajan Mills as both of them are unlisted,

HK companies define GM as EBITDA + SG&A…

ROC downloads through MCA12 website & ace equity

@anil1820 Got it. I was talking about the data in the chart where you compare KPR and Thiagaraj mills.

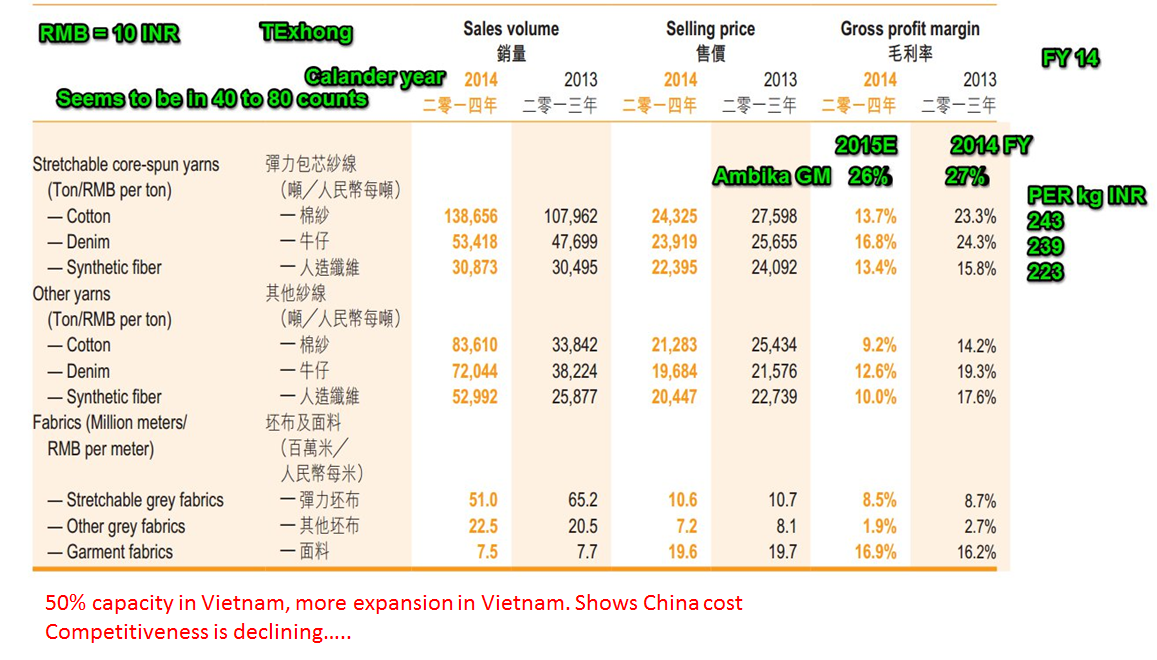

Anil- the loss in competitiveness was mainly due to artificially high cotton prices the Chinese government had mandated to protect their farmers as cotton prices plummeted over the past year, that policy has now changed so China is competitive again from a RM perspective. Labor costs though are lower in Vietnam but so is productivity.

Bobby

Ambika singificantly improved its WC by reducing its RM inventory from as high as 200 days to ~75 days. This happened around FY12 time frame. I am not able the trigger for the same.

Based on my inputs, companies that deal with Indian cotton need to maintain significant cotton inventory (as good quality Indian cotton is NOT available year around).

Also, if Ambika manufacturers yarn against orders only, would it still need to maintain such a large RM inventory? Perhaps, 30 to 60 days, but 75 days seemed a bit on the higher side.

@Donald

I was rereading some of the most knowledgeable posts, one being “Towards a capital allocation framework”. In that post you had commented “I realised, all other things being equal, the Size of the Opportunity before a business, its competitive advantage, and its Ability to Scale Up (ability to fund, manage the growth environment, execute, etc.), determines the Growth prospects for a business - and the success of my Portfolio allocations.”

Now trying to put AMBIKCO in that framework to understand the size of the opportunity before this company especially if the company is specialised and focussed on higher count yarns. Can it incrementally keep adding capacity (similar to Mayur, Kitex etc)? For sure it can double the capacity from its low base, but what about beyond that unless they are forward integrating?

They occupy a profitable niche. That niche of premium shorting is small in the overall context of textiles market. Ambika’s presence in tha niche @ ~500 Cr could be negligible?

Think They can continue to grow for many years especially as newer applications of finer count cotton with man-made fibres are emerging.

The runway and their competitive position is not under question. What must be questioned is the pace of capacity expansion, power situation in TN and managing labour training & scalability.

Pace of growth may be the issue. We have been spoilt by our super fast growing choices in the past

@Donald You summed it up very well. The pace of growth seems to be issue. The growth this financial seems to be close to zero.

No issues on the profitability, competitive niche and other fundamental metrics. My question is purely about growth and more specifically the growth mind-set of the promoters/management.

In last 4-5 years they have not increased any capacity except migrating to compact spindles. We can safely assume that management must be aware of competitive advantage, higher margins, better efficiency etc, so the question is why wont the management expand capacity. For a moment, lets put management hat and explore the reasons of not expanding capacity

Overall just trying to understand the management psychology on why there was zero capacity expansion in last few years.

It may not be a point that weighs highly for many investors here, but the fact is that companies cannot grow unless you have management with growth mindset.

To put things in perspective, one must study the industry dynamics- that will help clear some of this questions.

Instead of spoon-feeding, let me give some clues:

You are right probably that Management made a conscious choice of not expanding capacity till some parameters are seen to be conducive - but equipping ourselves properly with the dynamics of the domain will help us get to asking more pointed better questions

Good set of questions … trying to answer your queries pointwise…

I guess they did a wonderful job of improving operational efficiency if you look at sales / spindle and profit / spindle.

They have made a clean balance sheet and possibly now it is the time to take the next leap.

Demand for the quality of Yarn produced by Ambika would be there as it is the by product of their efficiency and not only for higher counts but for blending and manufacturing certain niche Yarns which other producers are either not interested to venture exclusively (as many of them are vertically integrated in the value chain) or may not be cost effective for them. Vertically integrated manufacturer and loom owners would look to improve Loom Efficiency and here possibly by using Ambika Yarns they have found it best suited for their requirement and hence may stick to them for years to come unless something drastically changes in Yarn manufacturing process like a technological or demand pattern shift.

Labor training and skill building is the single biggest factor for not scaling up fast. Wind Mill and gradually improving power situation in TN will mitigate the power issue to a major extent. No other issues seems apparent from their performance track record and financial situation.

The kind of products they manufacture and the small capacity they have (110000 spindles against million + spindles with major companies) are the major pointers for me that incremental capacity may be easily absorbed by the market.

Creating new client base may be an issue but it is also possible that existing clients may increase their capacity or intake from Ambika if they can supply … These are my conjectures. But with a very conservative promoter who consistently performed, possibly he would focus more on taking every step right than suddenly start running at a fast pace…

Over the past week, I have spent time speaking to a few industry experts and players to understand the market and competitive landscape…It was difficult to get a list of the top 10 players in finer count, but managed to get a few interesting insights, which helped dig further on the top players (provided in the following post) -

Market size for finer count is very small. Demand is limited, so larger companies have not focused on finer count

a. In 2011 - 12, total production of cotton yarn by mills was 3126 mn kgs (http://www.citiindia.com/images/database/table9.pdf)

b. Of this, 14% was more than 40s count (416 mn kgs)

c. Of which 112 mn kgs was more than 60s and only 52 mn was more than 80s

Finer count players will be based in the South (except larger players - Vardhman, Welspun etc) and predominantly in Tamil Nadu

a.Long staple is grown in and around Tamil Nadu, so mills in that part have focused on finer count

b. Road transportation cost is prohibitive (~2 Rs per tonner per km) from Tamil Nadu to North, making the economics a bit unviable

c. It is possible that companies near the port areas would import long staples from Egypt (Giza) and US (Pima), as port transportation is cheaper than road

The best way to get to the higher count players is to get a list of companies with EBITDA margin of more than 18% (lower count will generally not be able to achieve >18%+)

Market size for Suessen Elite & Elitwist

a. In 2013, total number of elite spindles in India were 42,00,000 (5,00,00 elite were sold in 2013), around 65,000,000 total worldwide

b. In November 2012, Over 37,00,000 EliTe spindles were running in India, about 57,00,000 EliTe worldwide (http://www.indiantextilemagazine.in/corporate-news/indian-spinning-industry-the-outside-view/)

c. About 5,00,000 EliTwist spindles are running worldwide, of which over 4,00,000 are in India (Nov 2012)

d. In 2015, Suessen EliTe Compact Spinning System has been sold for over 8,000,000 ring spindles

e. In Oct 2011, Peter Stahlecker, Joint Managing Director, Suessen Premium Textile Components said “Sixty per cent of our installations are in India. We have seen improvements in the market in the last couple of months. Further, we have an 80% market share of the Indian compact spinning and 85% are orders from the existing customers”

Have spoken to one of senior people at Venus Group (Mr Thakkar, who oversees Suessen sales in West India), which is the agent of Suessen in India. His view on the top players in higher count yarn are Ambika Cotton, Bannari Amman, LS Mills, Akkamamba Textiles, Sree Satyanarayana Spinning Mills, Rajapalyam Mills, Vardhman Textiles, GTN Textiles, GTN Industries, Premier Mills, NSL Group, Nahar Spinning and KPR Mills.

Please see below a short note on each including other players based one earlier research. Please note that the numbers maybe a bit dated -

Shanmugavel Group (Tamil Nadu) - 400,092 spindles, all of which are elite compact (will be ~5,00,000 spindles soon)…It is the largest customer of Suessen Elite Compact in the world (or was till a year back)…Produces 28s - 80s, with average 30s+…Exports to 60 countries…produces 250,000 kg of premium

quality yarn daily

Vardhman Textiles (Punjab) - Largest spindle capacity in India with total of 10,48,160 spindles, of which 22% yarn produced is compact based on analyst estimates…so 230,595 spindles are compact…they were early adopters of Suessen Elite in 2005, when they had 25,000 elite compact…exports USD200 mn of yarn

and produces 10s to 200s cotton

Welspun Group (Maharashtra) - Total 3,00,000 spindle capacity, of which 1,70,000 has been recently added all of Suessen Elite in Gujarat…Have recently opened a spinning facility in Gujarat for fine and super fine counts ranging 60s - 140s

Bannari Amman (Tamil Nadu) - 70% capacity is Suessen Elite Compact - 1,57,728 spindles…produces 16s - 100s…120 tons of combed yarn every day…24% revenue is exports

Eveready Spinning Mills (Tamil Nadu) - 80% capacity is compact - 1,21,056 spindles…10s - 60s cotton…36 mn kg produced per annum

Premier Mills (Tamil Nadu) - 119040 spindles produces >60/1s, and other capacity of 44,400 produces 40/1…Total group capacity is 3,24,072 spindles

7.L.S.Mills (Tamil Nadu) - elite compact 60000 spindles, EliTwist 35000 spindles, Ordered 11000 more elite Compact…total spindles 1,50,000 of which 1,00,000+ compact…60s to 160s in Egyptian, Indian and Supima Cotton

8.KPR Mills (Tamil Nadu) - Commissioned 1,00,000 Elite Compact Spindles (total 3,53,088 spindles), 90,000 ton annual production capacity

9.GTN Industries (Andhra Pradesh) - 13s to 120s, 1,00,000 Elite Compact and Elitwist Capacity (Total 1,20,000 capacity)

10.Loyal Textiles (Tamil Nadu) - Total Elite Capacity of 1,00,000 spindles (total 1,80,000 capacity), 5000 spindles with Siro Compact Spinning, USD 300 mn textile company, 6s to 120s, 34,000 ton yarn annual capacity

11.SJLT Textiles (Tamil Nadu) - Ordered in 2011 for 1 lakh elite compact (total

1,50,000 capacity), Sold in Italy, US and South Asia

12.NSL Group (Andhra Pradesh) – Total 2,77,168 spindle capacity…~32% production is compact yarn…and based on discussions they are a key player in higher count yarn…(~90,000 Elite/ Elitwist)…

14.The Lakshmi Mills (Tamil Nadu) - One unit of 66,432 is for 100% combed cotton yarn (-50s - 120s), total 128,720 spindle capacity, Spinnovation mentions Lakshmi Mills order for elite compact spindles, does polyester in other plant (40 - 100s)

15.Nahar Industrial (Punjab) - Only 65,000 Elite/ Elitwist capacity of total 5,00,000 spindles…produces 6s - 120s cotton

16.Sportking (Punjab) - 57,120 elite compact and elitwist (total 138,720 spindles), Average will be lower than 40s, Also does polyester, blended

17.Sri Nachammai Cotton Mills Ltd.(Tamil Nadu) - All 53,616 is Suessen Elite Compact Set

18.KP Textiles (Tamil Nadu) - All 50,000 equipped with Elite and Elitwist, 100/2, 94/2, 110/2 combed high twist

19.Maris Spinners Ltd. (Tamil Nadu) - All 46,176 spindles are Elite/ Elitwist, 30s, 40s and 60s, Caters to domestic market primarliy, 19% EBITDA margin (120 crore revenue)

20.Aarti International (Punjab) - 43,400 compact (175,000 total spindle capacity)…20s - 50s (has suessen compact)…100% cotton yarn…3 lakh tonnes per annum

21.Thiagarajar Mills (Tamil Nadu) - Has 81,168 capacity of which atleast 40,000+ is suessen compact…produces 6s - 140s double yarn…48% revenue is exports

22.Sree Satyanarayana Spinning Mills (Andhra Pradesh) – Has 39,000 spindles…adding another 11,000 spindles…focused on very high count (80s –170s)…60 crore revenues with 20% EBITDA margin…

23.Sree Akkamamba Textiles (Andhra Pradesh) – 86,928 spindles (of which 36,000 Suessen elite)…focused on 80s – 100s…achieves 56gms/ spindle/ shift at 80s…revenues of 130 crore with 17% EBITDA margin

Some other companies include Shri Govindraja Textiles (40,000 compact), Super Spinning Mills (32,000 Elite/ Elitwist), Kallam Spinning (31,488 suessen - 20% ebitda - 220 crore sales), Sambandam Spinning Suessen customer since 2000, only 100% cotton yarn, 1,10,000+ spindles), Precot Meridian (have some Suessen Elite/ elitwist capacity), Idupulapadu Cotton Mills, Nitin Textiles, Sri Balambika Mills (18,000 Suessen), Sri Venkatram Spinners.

Some other points based on the research -

Decision to be in finer count or coarser count depends on throughput (production per spindle) vs contribution (yarn price less cotton price)

a. Cost of setting up capacity is almost the same for finer/ coarser counts

b. Capacity can be switched between finer/ coarser counts

c. For finer count, contribution is higher, but production per spindle is lower

d. If contribution margin goes down, then the capacity is switched to coarser counts

High Price sensitivity (no bargaining power with the buyer), and ready demand for lower quality yarn

a. Traders and small weavers determine the price of the yarn

b. Even a 10 paise cheaper price for coarser quality yarn would be purchased

c. There is a ready market for coarser quality yarn and any quantity of the yarn can be sold

d. However, for finer quality it is a smaller market, and you need a differentiated product to ask for the price demanded

India’s yarn export destinations for 2014 include

a. China (40%), Bangladesh (12%), South Korea (4%), Egypt (4%), Hong Kong, Portugal, Turkey, Italy, Columbia, Vietnam

b. China has in the past been ~25–30%, and had jumped up significantly last year

Capex per spindle

a. Capex per spindle could be Rs ~30000 – 35,000

b. Ambika in 2009 annual report also mentions they spent 139.73 crores to build 43,200 spindles (outlay of 32,000 per spindle)

c. RSWM in their 2014 annual report says that their average spindle capital cost is 28,707 against industry average of 30,000

Uses of compact Yarn

a. Shirting, woven products, hosiery, trousers, socks, denim etc.

b. All different fibres are used : cotton, blended, rayon etc

c. Commercial count range is 7s to 300s

Based on my discussion with Mr Thakkar, who is responsible for sales of Suessen in West India, have updated the list of players focused on higher count yarn.

@Donald, I asked him his views on the GPSS for higher count. He quoted the following examples -

His views on capex per spindle -

Regarding international players, he did not have any idea. I have been able to get the following names, who have focus on higher end -

For folks spending time to understand Ambika Cotton, Mr Kakkar made an interesting comment, which should keep us focused at digging further. I did not tell him that we are evaluating Ambika Cotton. However, when I asked him the top players in higher count, he said by a huge margin it is Ambika Cotton, which he says is focused on being the best player providing the best quality yarn.

Cheers

Fantastic discussion; this is the first time I’ve been able to see such a detailed discussion on VP.

I’d just like to step back a little from the industry analysis part which Donald and others have lead to step by step to the basic numbers for the company (I’ve removed other operating income like trading and windmill income and put it in other income):

The big question, still unanswered for me is the drop in gross profit in FY12 the the inability of the company to increase it thereafter. Now for FY12, the explanation is not difficult. For this, we will have to go to the cotton purchasing policy of most companies.

Most companies, including Ambika, procure most of their cotton requirements during the peak cotton season (October-January). This leads to a high inventory holding period of 6-8 months to ensure high cotton availability for operations through the year (all the more important for Ambika). So what happened in FY12? International cotton prices increased significantly by 150% to 229 cents per pound in March 2011 from 92 cents per pound in August 2012. So Ambika (and other players) had to stock cotton at high prices. The market crashed by 58% to 95 cents per pound by December 2011. Clearly, all spinners would have had to take a major inventory hit in such a case, and that led to declining gross margins for FY12.

So why have margins not increased from FY13 onwards? Thats a big puzzle really to me. Most players seem to have rebounded from FY13 onwards, whereas Ambika’s COGS has remained where it is (Although the company has reduced its power costs). The explanation could lie:

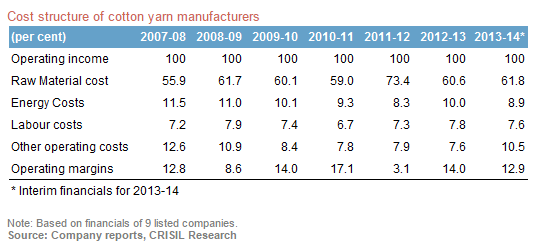

I reckon it is critical we answer this question. From CRISIL’s reports, I could reckon that Ambika’s gross margins are not very different from the industry currently:

Yes, where Ambika is doing very well as compared to other players is energy costs (Ambika in the range of 5-6% as compared to 9-10% for industry). So this implies:

So is the finer count really giving the company a competitive advantage? I am not so sure.

Still have to look at the other part of DuPont’s equation - asset turnover comparisons. However, that still does not lend credence to any competitive advantage enjoyed by Ambika because of higher costs (or certainly does not reflect in its current numbers).

Looking to solve this part of the puzzle because the numbers are not tying in with a lot of scuttlebutt which has been done by esteemed posters.

I will try and reach out to the promoters of Gimatex and RSR Mohota Mills (Know the promoters indirectly) and will try and update more on what I can find out on higher counts.

Disc - Not invested. Also, request you to ignore the tax & PAT numbers in the table; have not updated those.

The other thing is that Ambika has seen 2 rating upgrades in the last 18 months or so

BBB+ to A- by CRISIL last year

A- to A by CARE in November 2014.

Attaching the truncated CARE report (Dont have access to the full report)

AMBIKA COTTON MILLS LIMITED-11-07-2014.pdf (451.1 KB)

Just back in station. Thank you guys for taking the discussion/analysis further. Couldn’t help commenting straightaway for the sheer quality of posts. Will reply to some of the specifics raised, later.

@Naman

Thanks a lot for your painstaking work on industry mapping & scuttlebutt

Not many would be as systematic as you in their approach nor would they value this exercise as much. But in VP process, this is a much desired quality. We are co-opting you on the VP Process document creation team - that we have planned to submit - by the time we complete the Ambika puzzle

[quote=“Naman, post:158, topic:865”]

However, when I asked him the top players in higher count, he said by a huge margin it is Ambika Cotton, which he says is focused on being the best player providing the best quality yarn.

[/quote]

“This” is the real scuttlebutt - extremely valued by VP. Most times, it’s difficult to put a finger on the specifics of why someone is so far ahead of others in the game. We need to get this corroborated by the right kind of source(s) - and someone from Suessen should know the industry players very very well.

{In a VP Mentors words this is called “Going to the Gatekeeper” akin to someone getting to Monsanto (the royalty taker in Cotton BT Hybrids in Indian market) - when trying to ascertain Kaveri Seeds prospects in 2011, when they were still a fledgling but very promising player}

We need to however work on getting the “real” differentiator - what are they doing that others cannot copy? Is this for real?

@karanmaroo

Think we posted a comparison on RM/Sales for Ambika which showed a direct correlation with Operating Margins. If I remember correctly, margins drop was exactly in consonance with the rise in RM/Sales %.

So why isn’t the lower margins in last 3 years not attributable to Gross Margins staying where they are?

Re:Scuttlebutt with industry players

Great that you are trying to connect with Industry players for further scuttlebutt. Since you know them try getting further references to any of the higher count players like - Bannari Amman, LS Mills, Akkamamba Textiles, Sree Satyanarayana Spinning Mills, Rajapalyam Mills, Vardhman Textiles, GTN Textiles, GTN Industries, Premier Mills, NSL Group, Nahar Spinning and KPR Mills as mentioned by Naman. We have had very good feedback on some of these especially Bannari Amman, Premier Mills, RAMCO group, Nahar Spinning, GTN (had temporary staff problems but recovering)