That’s cash eps. EPS is 95.4 which is also good at 26% up.

1 Like

EBIDTA per spindle increased to 9,734 in 2017 vs. 8,713 in 2016. Quite impressive. They are becoming more and more efficient each year.

Disclaimer: Invested

4 Likes

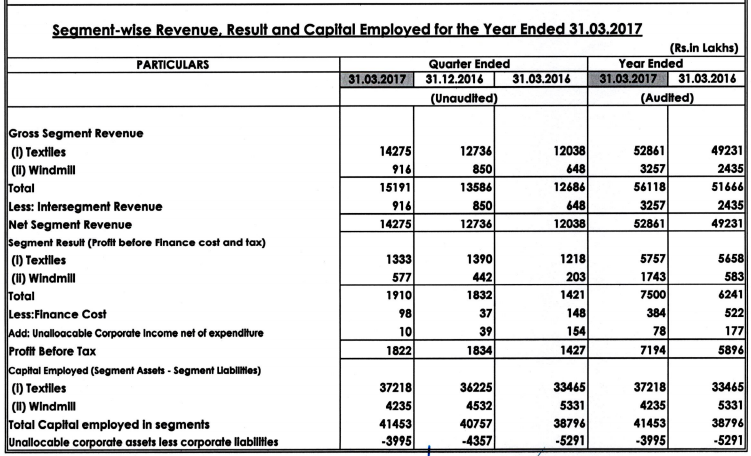

Largely profit growth is coming from Wind mill segment. Is it my correct reading or i am missing something…

Source: Company published result

1 Like

I think you are correct. So the results might not be so positive, after all. You want profits to grow in the core business.

Improvement of Textile revenue by 22 Cr. Yoy with same capacity utilization is a great achievement. Also, they use windmill for in-house power generation. So, now they are becoming operationally more efficient by using even more renewable power than using paid electricity. This should be viewed in combination and not isolation.

Having said that, let’s wait for their production quantity figures. If they have really produced more with same capacity, then its sign of de-bottlenecking existing plants.

7 Likes

I am not sure if anyone has noticed this. Crisil has rated its working capital credit line of 455 Cr as A stable and A1 (upgraded by one notch on both long term and short term basis).

Interesting thing is…banks are willing to lend them 455 Cr. while the market cap is 750 Cr.; But they only took short term loan of 7.5 Cr.

One should go back and re-read below article and connect that with this situation:

11 Likes

ValueQuest has increased its holding in Ambika as per the latest shareholding pattern.

3 Likes

Vivek bhai - They are very efficient. But they have not done any capex, where is growth going to come from? This is trading at 13 trailing pe, isn’t cheap. Any news on clearance on the expansion project?

1 Like

Hi Mridul,

On the growth part, if you compare YoY result, they have PBT growth of 22% YoY which is stunning. They achieved this through making operations more efficient + reduction of finance cost + new knitting facility that started in October 2016.

The way I look at the company is:

- They have high earning power, and running at full capacity which shows powerful demand for their yarns

- This is not cyclical business as they have fixed realization per kg and they have maintained in bad times >> Implying excellent pricing power

- Will they never grow in future? The answer is NO…at some point they should be able to do the capex

- They are generating almost 70-80 Cr Free cash flow now (with minimal chance to go down in future)

So, here is a company which has strong earnings power, ethical managent, pricing power even in downcycle, ability to scale up in future and excellent free cash flow available just at 13x PE (and if you consider owener’s earnings even cheaper!!)

On capex, as per my knowledge it’s still pending, but should happen sooner or later. Will be probably attending AGM and can provide more clarity after discussion with management.

Other way I look at it is, if they are unable to do capex in future, they can distribute cash as dividend or buyback. Even if they give half of 80 cr FCF i.e. 40 Cr. >> Its whooping 5% dividend yield vs. 6% of G-sec yield. So, I am ready to hold it like bond until they do a capex and further growth happens. Looking it like a call option!!

Disclosure: Invested and adding on dips; My views may be biased

15 Likes

I guess this is a very different kind of company. The management itself is the moat. Very rare …

2 Likes

If there is no growth in the topline then for how long they will be able to sustain the PAT? Salaries and other costs will increase with inflation. Inability to find the answer to this question is the reason which kept me out of Ambika.

Your input is appreciated

Kanv

2 Likes

You can look at historical growth in realizations per spindle and that will give you the answer

3 Likes

the key question to ask is growth not happening because there is no growth in market or is it because the management does not want to grow at this point of time or there is some temporary roadblock in growth plans. My personal assessment is for last 2-3 years it was point 2 and now it is point 3 (approval issues).Now, for a business with single digit working capital, single digit receivable days, even if market has no growth, i think growth can be possible by taking market share which qualitatively reflects when you hear that companies want them to give business but they are not taking. When such honest promoter takes a decision, I better go by his belief that he will take right decisions at right point of time. Also, few years back, promoter mentioned that he would like to get rid of debt. So, he is not a promoter who would like to grow on debt. Now this is a mind set . Depends. Personally i like such companies. No one knows future. History is best possible parameter. Look at history for how it has grown. Also, promoter has said after 30k spindles he will not do further expansion and next area of expansion could be fabrication. So, there could be a cap on core growth until he does some forward or backward integration extended business for new avenues of growth.Now, up to us whether we want to go with such a management which is honest, can grow well when opportunity given, believes in reaching to optimum efficiency to extract best out of capital invested, is financially prudent for investors, like to be debt free and market giving opportunity to buy at decent valuation or want to go with various other opportunities in market. There is no absolute right or wrong decision

11 Likes

Q1 fy18 results look good. Please follow the link to check the results. BSEINDIA

Good to see the management is expanding knitting facility.

Regards

Krishna

5 Likes

Indeed. Doing capex with RoCE of 35-40% is a great sign of efficient capital allocation (without any dilution/debt…fully from internal accruals). Even if this new facility runs at ~60-70% utilization it can provide good visibility for future profits.

Disclosure: Invested

5 Likes

Analysis on the new capex that is announced:

Extract from Annual report 2015-2016:

“The company is implementing knitting facility at an estimated cost of INR 834.92 lakhs (~8 Cr), fully funded out of internal accuals…expected to be operational from October 2016 onwards”

Since the new Spinning unit is stuck in land approvals, they went ahead to start knitting facility in the approved unit

Total outlay was ~8 Cr for this capex

Below is the sales in kg and value terms for Knitting unit for 2015-2016 (plant started after Oct-2016)

Sales 757990 Kg - Value: INR 156780807 (from annual quantitative data sheet provided by the company)

It comes out to be INR 206 per Kg. Assuming 4 months since knitting was working (~120 days) it produced 6,316 Kg. per day; Net profit margin for Ambika is roughly 10% which translates to INR 1.5 Cr profit for this period

Annualized profit translates from this to INR 4.5 Cr. against outlay of INR 8 Cr. >> RoCE of 56%

Company had capacity of 8,000 Kg per day which translates to ~79% capacity utilization of knitting facility soon after the commencement which is excellent sign of demand

After June-2017 results, company announces plan to increase its knitting capacity by 3x, from 8,000 Kg per day to 24,000 Kg per day by November 2017

Assuming capacity utilization of 70% initially i.e. ~16,800 Kgs per day it would translate to 61.32 lac kgs per year; Assuming same sales of INR 206 per Kg it would translate to yearly INR 126 Cr incremental sales and assuming 10% net profit margin it should translate to total net income from knitting facility at INR 10-12 Cr. (incremental net income of ~INR 7-8 Cr. assuming existing capacity gives INR 4-5 Cr.)

On an investment of INR 20 Cr., this translates to RoCE of 35-40%

Current net profit is INR 50-60 Cr per year on LTM basis; Incremental net income from this capex will increase net profit by ~20% even if we assuming status quo for spinning unit (for 1 year from Nov-2017)

At a market cap of INR 750 Cr. with full-year net income by Dec-2018 of ~INR 65-70 Cr. gives comfort in terms of valuation and growth; Owner’s earnings are going to be even better @ INR 75 Cr.+

Approval of pending plant (additional 30,000 spindles) remains additional upside whenever that happens

Disclosure: Invested

17 Likes

@vivek_mashrani Is this from FY 17 annual report ? Can you please post the link here

Annual report is not yet out. This is from latest result for June 2017.

Hi

Myself a knitted garments manufacturer from Tirupur…

I dont know whether these infromations are useful to you, since you talked about knitting unit facility expansion, here are some basic facts about knitting…

1. Production capacity of a single knitting machine is around 300kgs per day ( i mean 24 hours, they operate in 2 shifts)

2. Knitting charges will be Rs 8 to 10 per kg. so if you know the number of machines installed, you will get an approximate idea of how much it can contribute to the top line....

3. Because of GST implementation, about 50% of yarn business affected in July month....This is ground reality and i am talking about spinning mills over all...I am not sure how ambika stands out...

4. In August month, cotton yarn prices were reduced by the mills between 10 to 15 rs per kg.

Please forgive me if above mentioned details you already aware of..

16 Likes

Thanks a lot. Please do keep us posted with industry. Being someone on the ground is something which cannot be replicated with any analysis.

Appreciate your insights!!

1 Like