-

Speciality cotton yarn has provided high margins so far…but sustainability of its competitive strengths not clear.

-

What can stop competitors to copy its technology & strategy? Textile industry has been traditionally prone to intense competition. Technology upgrades are easily acquired and any cost-saving & efficiency benefits percolate down to retail consumers, instead of improving business profitability

-

Sustainability of its moat and ROE is not clear, which should be of interest to a long term investor.

-

Free cash flows, while positive, have been volatile…not an encouraging sign.

-

Too richly valued at current price

I would like you to think deeper to get answers of your questions:

-

What does a competitor need to effectively produce and sell specialty cotton yarn with good competitiveness? Effective sourcing, certification, premium customers, consistent quality, good reputation, low cost labour…any other points?

-

Think otherwise…what can stop Ambika to acquire new technology as and when it comes and continue supplying to its partners who has long standing trust in Ambika and delivered consistent quality for years. Still I think it can remain low cost because of its better utilization levels and good bargaining power (remember the receivable days for Ambika is just 14 days…shows its bargaining power!!)

-

Generally its cost plus business and margins of such yarn will always remain higher than normal yarn. And always number of players producing this will remain low because its not easy to make such yarn plus you need strong relationship with clients to sell it.

-

Have you studied the reason of FCF volatility?? If you have closer look the dip is when they have done capex or upgradation or repaid debt…does it worry me? No, since FCF bounces in subsequent years due to this…

-

What is FCF yield it is trading currently? If you find this you will come to know that its exactly opposite…!! Do clean-up FCF for historical debt repayments since it is now debt free…!!

Disclosure: Invested and views may be biased; Do your own homework please…!!

3 Likes

Good thinking. Would be useful to study of its competitors. I have not done this yet.

If you have…would appreciate your thoughts.

Buyback to be considered on 11th Nov, 2016

http://www.moneycontrol.com/stocks/reports/ambika-cotton-board-to-consider-buybackequity-shares-5373721.html

1 Like

Completely debt free now.

it seems after Trumps win, Trans specific agreement (TPP) is as good as dead now

Ambika cottons has anounced a buyback. Promoters are not participating, which means they think the shares are undervalued and are confident of its prospects. Most companies announce buybacks instead of dividends only to avoid paying taxes on dividends. The company will buy back shares from open market, and not through tender at a higher price. These are definitely good news to shareholders. Happy to be one of them!

Disc: invested

have they given any date on which they will buy?

and how will they buy…in a single go or in phases?

Company has approved buy-back of 1,50,000 Equity Shares at a price not exceeding Rs. 1100 from open markets i.e. through stock exchanges.The Company proposes to buy-back 75,000 Equity Shares for a minimum of Rs. 8,25,00,000 (Rupees Eight Crores Twenty Five Lakhs only), being [50]% of the Maximum Buyback Size.

Disc: Invested. No transactions in last 30 days.

Buyback to commence on 1 December 2016.

Buy back thro open mkt purchase will not benefit shareholders except lifting of sentiment. In this downward bias mkts, Ambika will mop up shares around 1000. If they wanted to give benefit to minority shareholders , they should have opted “tender route” as done by Balrampur chine and Aarti Ind.

Agree, tender route have been better. But in this route as well, one can see company buyback order separately in the exchange. The more the number of shares extinguished at lower price will be good for shareholders who hold the shares. This will increase the EPS and future dividend to shareholders.

Further, if you analyze the cashflow statement of last year, they have repaid all loans and still generating huge cashflow. Given they are yet to get approval for new plant, the cash was piling up. They had two ways to deploy (a) pay special dividend (b) buyback of shares. Among these I think buyback is best particularly here since management is not participating. This gives 2 clear signals:

- Efficient capital deployment and rewarding minority shareholders

- Promoter’s confidence in the company since they are increasing the stake and not participating in the buyback

10 Likes

Buyback through tender offer route is operationally more complex and expensive. It is not feasible when the size of the offer is small. For an offer size of just Rs.16.25 crore, market purchase is the cleanest and simplest route. Also note that small shareholders have already got their returns, as the stock has moved up from Rs.800-odd levels to Rs.1000-odd levels in the run up to the buyback.

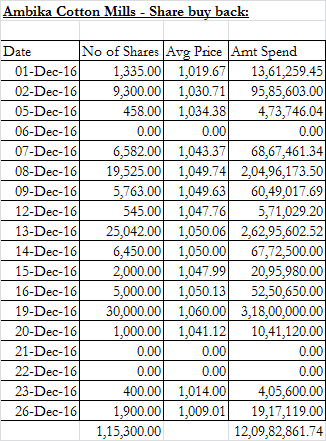

Ambika Cotton Mills bought back 1,15,300 share on open market.

The company has spend about Rs.12 Crores .

6 Likes

Prof Sanjay Bhakshi has added 65,000 shares this quarter through his fund Value quest

3 Likes

It is very surprising that after the buyback also the number of shares in Sep-16 and Dec-16 is same. Need to clarify the same with the company.

In the public shareholding heading goto sub heading “ANY OTHER”. Ambika Escrow account is having the buy back shares

1 Like

Detailed buyback in Dec 16 and Jan 17 is also available on their website in the archives section.

1 Like

Great. So I guess they will extinguish all after the entire buyback is compleet. Thanks for the response. Cheers!!

Results are published , YOY sales is up by 7% and profit up by 25% , EPS is at Rs 145/- Results seems good .

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/9933823c-714a-4909-b9b7-c79ecfa7b23b.pdf