http://danvilledaily.com/technicals-at-a-glance-for-ambika-cotton-mills-ltd-ambikco-ns-shares/

Pls help me understand. Why is Ambika special? If I compare it with other textile players, say Vardhman Textiles, it would seem to me that Vardhman has better ROE, a better track record, at least 10 times larger size, and has a PE ratio which is 30% smaller. It even has a better dividend yield.

What specifically makes Ambika a better business?

2 Likes

Few things

Debt

Vardhman : 2000cr

Ambika : NIL

Receivable days

Vardhman : 44

Ambika : 9

ROCE better for Ambika

8 Likes

One more thing - Better management

Ambika is likely to handle any problem/shortcoming in the future better than its contemporaries

@samir_brd Though question was not to me, a similar discussion happened with one of fellow VP colleague which pushed me to think in same direction few months back and hence sharing the findings.

First thing first, future is unpredictable, so, let us look by history:

I had data available only till FY 16 that time. Hence, analysis is based till FY 16 numbers

Analysis of profitability on the basis of margins, mean and variation to mean in terms of consistency of performance:

- Due to size and leadership, though Vardhman has a better margin, the gap between maximum and minimum is relatively lower for Ambika which means more consistency. However, there are few other business reasons and I will come to this. However, they overall look comparable

Deployment of resources for revenue generation

- Though Ambika on a long term lagged on revenue generated per unit net fixed asset but it is catching up well. Now, this may happen due to different age of assets and utlization increase which would be more evident once you start analyzing net fixed asset to gross fixed asset ratio and depreciation numbers

3 On a man power productivity basis, Ambika loooks ahead of Vardhman but Vardhamn leads when it comes to SGA expenses

4 So far on profitability scores look at par where one has relatively better margin, other has more consistency and still quite comparable

Story starts getting interesting once we get into operations and cash flows

Let us analyze efficiency of operations by looking at working capital , debtor and inventory days

5 Ambika leads Vradhman by a huge margin more than 2x times on working capital management and 3x times on debtor management. though historically, Ambika was lagging on inventory management, offlate, it has started performing better than Vardhamn. All thsi is reflected consistently year after year whichever comulative average one takes

6 This remarkable different performance gets reflected further in cashflows where due to strong working capital, debtor and inventory management Ambika is able to converts more profits into cash and hence compensates for lesser profit margin (which is an accounting concept to actual cash) on a cumulative basis. Also, please note few things here that during 2011 cotton crisis, none of textile companies were spared including Vardhman whose cash flow went negative but Ambika looks more consistent. Infact out of 10 years , Vardhman had 3 years of low cashflow but Ambika has been more consistent. Also, please note that in 2015 , Vardhamn CFO to PAT is 3.4 but i think Vradhamn textiles apart from holding textile business has few unrelated businesses like steel and i think this exceptional gain was due to some one time gain or sell off please check. Having these unrelated businesses is another reason why Vardhamn ROCE is lower than Ambika apart from higher leverage despite of similar kind of other paarameters

7 Also, looking at ability to convert accounting profit into free cash flow, Ambika wins it over Vardhaman. Similar thing could be analyzed even in terms of FCF to sales ratio. I am not sure if Vardhman is working under capacity and it can improve. However, believe Vardhman has plans for 300 cr capex in next 3 years ,so, that does not look the scenario where as Ambika revealed their latest capex plan which converts into 35% ROCE analysis as per done by @vivek_mashrani which is again much better than Vardhman. Offlate Ambika performance looks deteriorating but we need to exclude Vardhman one time gain and check numbers and also for cashflow related stuff, it is better to take a long term consolidated view.Still, it makes sense to deep dive further into why Ambika has deteriorated and Vardhman has improved. This could be an important trigger for future valuation if compared relatively

8 In terms of leverage, again, Ambika wins over Vardhman and in future also, Ambika is expected to be debt free

Growth Aspects:

9 Considering how these two companies have grown historically in terms of revenue and profit, on a long term basis, by revenue they were comparable ,however, Vardhman had upper hand in profutability. However, in 2016, Ambika had a dismal year where has Vardhman had strong growth (hoever i think this profit growth was a result of one time gain, people who have tracked Vardhman in detail can confirm)

So, overall on accounting profitability and growth basis, both companies more or less look comparable but when it comes to convertion of accounting profit to cash profit and cash profit to free cash flow, Ambika looks clear winner on a long term consistent basis.

Now coming to future, both Ambika and Vardhman have revealed thier plans. The extra challenge for Vardhman would be to prove their mettle in value added product but given their backgroudn they should be able to do. But i think if one does a return on capital on additional future investments, I have a feeling that Ambika would fare better though these would be pure estimates

Also, the unrelated business of Vardhman remains an overhang

now coming to valuation, on a PE basis Ambika is trading some where around 13 and Vradhman around 10 which is approx 30% difference. I would leave it to individual to decide how they would like to valuate businesses in long run on a relative basis.

Disc : Hold 7% of portfolio in Ambika and 1% in vardhman (have started a slow accumulation recently , however, if valuation gap closes by Vardhman’s appreciation, wont mind switching the money to Ambika considering everything else remains the same in investment assumptions)

Note ; Some of conditional formatting elements are not true reflection of what I wanted to project as the excel used tool is still in development phase

31 Likes

Thanks @Hocuspocus32 and @ricky_ and @suru27 for your replies. @suru27, you have an especially detailed response, which requires a lot of chewing over. I hope I can do this exercise one day, and come back with a more considered reply.

@Hocuspocus32, while Vardhman has debt, this debt is very cheap, and the ROE is much higher than the cost of debt for both Ambika and Vardhman, and has been consistently higher. In such a situation, it is most appropriate to take debt, because for the same ROCE, a company with debt will deliver a better ROE. And indeed, Vardhman’s ROE is higher than Ambika. Also, their cash and cash investments account for much of the debt anyway. For sure, what you say about receivable days is true, and as @suru27 has pointed out, the working capital management at Ambika is clearly better.

@ricky_, I am not sure how you can come to the conclusion of better management. Indeed, these guys have built a huge business (more than 10 times Ambika size) in a generation. And they have a clearly defined succession line, which is not the case with Ambika. And I have held the company since a few years, and I can’t see any example of bad governance or so.

@suru27, you are clearly going somewhere correctly with the working capital management. Vardhman has both high receivables, and they seem to be also hoarding cotton. However, my own feeling is that CFO is actually better than for Vardhman than Ambika. But I need to check more.

I am not sure I agree with you about the investments in other businesses. The only “non-textile” business VTL itself has invested in is Steel, of which VTL owns only 30%, and the original investment is only 5 crores or so. In any case, the steel business is less than 10% of the turnover of VTL. It is hardly significant. On the other hand, VTL is so much more diversified across the textile chain than Ambika. They spin yarn, they make fabric, they process the fabric, they make garments, and they also make (or used to make) threads. They are not cotton processors alone, they also make blends, and the use of man-made fibers is increasing in the overall consumption basket. This clearly makes them less susceptible to changes in cotton price and production.

On the other hand, Ambika seems to have a nice niche in extremely high end cotton. One needs to mull this over, along with the other issues which @suru27 has raised to make the comparative investment case.

Disc: Own VTL (about 0.5% of my portfolio). Had more, but sold much of it last year@1200. Reentered in a small way recently.

4 Likes

Hi All,

I have a couple of queries for the management on the various projects Ambika has initiated in the past couple of years.

- In Annual report 2016, the company mentioned about developing a new knitting facility at the cost of ~8.4 crores. And in AR2017, investment in knitting facility comes out to be ~10 crore - That signifies ~20% increase in the Project cost. Although a deviation of 1.6 crores may not be huge amount but an escalation of 20% in cost estimate for a project <1 year period definitely need some reasoning

- Approval for an additional spinning facility (project cost ~100 cr) is still pending for over 2 years. Management has not mentioned neither why they have not been able to make any progress in the last tow years nor when they are expecting clearance from the government to start working on the capacity addition. The recent political turnmoil may justify a possible delay of 6 months in government approval, but the delay in plan approval is for period much more than that.

- In Annual report 2016, management highlighted that they are undertaking capacity augmentation steps at the cost of 12 crores in the existing facility (as they have not made any headroom in planned capacity addition). There is no clarity available exactly what they are planning to do or what would be the potential outcome of that. In annual report 2017, there is no commentary about this capacity augmentation.

- One more clarification - In all the annual reports, Ambika has mentioned about undertaking investment on technology upgradation - Can someone clarify whether it is maintenance capex against depreciation or new capex.

These questions are relevant for the understanding management project’s execution capability and what are their plans for making grown in next few years.

- In the case, Ambika is unable to undertake projects for expanding spinning capacity (Project capex of 100 Crore or 12 crore) apart from what mentioned in annual report 2017 (Capex ~35 crore), there would be a good amount of cash surplus company would have at the end of this financial year. What would be Ambika’s steps in utilising the cash generated in current year?

If anyone can share any information on above aspects would be very helpful. Also, anyone attending AGM this time may ask management about these issues.

Thanks in advance.

Do you any one know what is spinning capacity . I guess they are still waiting approval to add 30 K spindles

The Annual Report gives the spinning capacity. It is 108,288 spindles.

1 Like

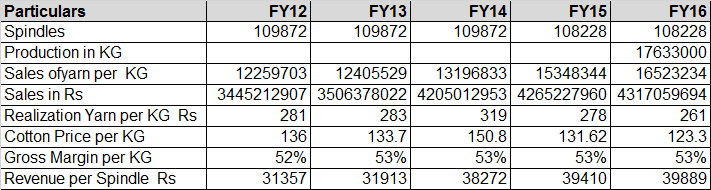

Have look at this

Particulars FY12 FY13 FY14 FY15 FY16

Spindles 109872 109872 109872 108228 108228

Production in KG 17633000

Sales ofyarn per KG 12259703 12405529 13196833 15348344 16523234

Sales in Rs 3445212907 3506378022 4205012953 4265227960 4317059694

Realization Yarn per KG Rs 281 283 319 278 261

Cotton Price per KG 136 133.7 150.8 131.62 123.3

Gross Margin per KG 52% 53% 53% 53% 53%

Revenue per Spindle Rs 31357 31913 38272 39410 39889

3 Likes

I wanted to understand how knitted garment per kg be less than yarn per kg. I believe Ambika is giving value add figure above yarn as they will be converting their yarn into knitted garment so 280 +200 will be actual price of knitted garment .

Sir

Your link of Ambika Cotton Mill excel is not accessible. Sir can you re-post it.

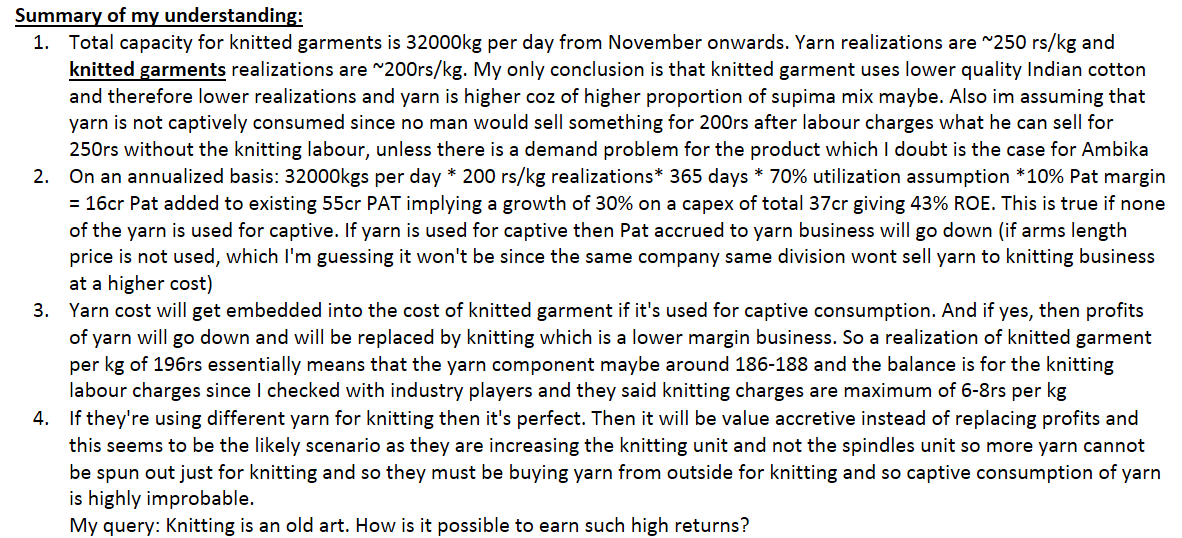

Summary of my understanding:

1. Total capacity for knitted garments is 32000kg per day from November onwards as per the latest AGM. Yarn realizations are ~250 rs/kg and knitted garments realizations are ~200rs/kg. My only conclusion is that knitted garment uses lower quality Indian cotton and therefore lower realizations and yarn is higher coz of higher proportion of supima mix maybe. Also im assuming that yarn is not captively consumed since no man would sell something for 200rs after labour charges what he can sell for 250rs without the knitting labour, unless there is a demand problem for the product which I doubt is the case for Ambika

2. On an annualized basis: 32000kgs per day * 200 rs/kg realizations* 365 days * 70% utilization assumption *10% Pat margin = 16cr Pat added to existing 55cr PAT implying a growth of 30% on a capex of total 37cr giving 43% ROE. This is true if none of the yarn is used for captive. If yarn is used for captive then Pat accrued to yarn business will go down (if arms length price is not used, which I’m guessing it won’t be since the same company same division wont sell yarn to knitting business at a higher cost)

3. Yarn cost will get embedded into the cost of knitted garment if it’s used for captive consumption. And if yes, then profits of yarn will go down and will be replaced by knitting which is a lower margin business. So a realization of knitted garment per kg of 196rs essentially means that the yarn component maybe around 186-188 and the balance is for the knitting labour charges since I checked with industry players and they said knitting charges are maximum of 6-8rs per kg

4. If they’re using different yarn for knitting then it’s perfect. Then it will be value accretive instead of replacing profits and this seems to be the likely scenario as they are increasing the knitting unit and not the spindles unit so more yarn cannot be spun out just for knitting and so they must be buying yarn from outside for knitting and so captive consumption of yarn is highly improbable.

My query: Knitting is an old art. How is it possible to earn such high returns? Maybe coz they are using the same land parcel and their power cost is subsidized coz of captive wind power.

Please correct me if im wrong somewhere. Thanks.

1. Total capacity for knitted garments is 32000kg per day from November onwards as per the latest AGM. Yarn realizations are ~250 rs/kg and knitted garments realizations are ~200rs/kg. My only conclusion is that knitted garment uses lower quality Indian cotton and therefore lower realizations and yarn is higher coz of higher proportion of supima mix maybe. Also im assuming that yarn is not captively consumed since no man would sell something for 200rs after labour charges what he can sell for 250rs without the knitting labour, unless there is a demand problem for the product which I doubt is the case for Ambika

2. On an annualized basis: 32000kgs per day * 200 rs/kg realizations* 365 days * 70% utilization assumption *10% Pat margin = 16cr Pat added to existing 55cr PAT implying a growth of 30% on a capex of total 37cr giving 43% ROE. This is true if none of the yarn is used for captive. If yarn is used for captive then Pat accrued to yarn business will go down (if arms length price is not used, which I’m guessing it won’t be since the same company same division wont sell yarn to knitting business at a higher cost)

3. Yarn cost will get embedded into the cost of knitted garment if it’s used for captive consumption. And if yes, then profits of yarn will go down and will be replaced by knitting which is a lower margin business. So a realization of knitted garment per kg of 196rs essentially means that the yarn component maybe around 186-188 and the balance is for the knitting labour charges since I checked with industry players and they said knitting charges are maximum of 6-8rs per kg

4. If they’re using different yarn for knitting then it’s perfect. Then it will be value accretive instead of replacing profits and this seems to be the likely scenario as they are increasing the knitting unit and not the spindles unit so more yarn cannot be spun out just for knitting and so they must be buying yarn from outside for knitting and so captive consumption of yarn is highly improbable.

My query: Knitting is an old art. How is it possible to earn such high returns? Maybe coz they are using the same land parcel and their power cost is subsidized coz of captive wind power.

Please correct me if im wrong somewhere. Thanks.

2 Likes

Ambika cotton performs conistenetly in such a challenging macro environment. Letter to shareholders kind of stuff done this time by CEO, speaks a lot of the quality of company and management

http://www.bseindia.com/xml-data/corpfiling/AttachLive/b1f884b8-a64a-4494-af72-89e85969d809.pdf

3 Likes

They are increasing knitting capacity from 8000 kgs/day to 32000 kgs/day… That amounts to 300% increase in production capacity… which is quite huge… Have I read it correctly or I am missing something?

You are seeing just the knitting capacity increase which forms a part of the revenue. The major share of the revenue comes from spinning of yarn. So please don’t misunderstand that overall capacity will increase by 3 times. please read the above thread carefully. Members have shared the information in detail so I won’t repeat.

1 Like

ok… Got it… Sorry for my ignorance…

Do anyone has any information about ‘land use’ case which the company is fighting and because of which it has not been able to expand spinning capacity? Anyone attending AGM may like to share information which company might have shared during the AGM

They said since court is not functioning, they are stuck with the proceeding and it may still take time to get approval for the same.

2 Likes

Thanks Vivek for sharing the information.I believe that they are stuck with

the plan for over 2 years. I agree that court proceedings are painfully

slow in India and it may take more time. So as a management you just cannot

keep waiting forever (as in this case - if they don’t have any clarity how

long it would take to sort the issue). It would have been better that

management shelve this plan for now and look for other either a plan B with

a land with no issue or identify other opportunities to grow business (like

expanding knitting business).

Vivek in case you attended the AGM, can you share any other information/

clarification shared by the management.

Disclosure: Invested for over a year and forms a substantial part of my

portfolio

1 Like