The steady state numbers suggests it should be on an average 95%.

Hi @jirohit

You have raised a very pertinent question and @vivek_mashrani has answered it beautifully. I am invested in Ambika myself and I thought I will share what I think.

In my investments I like to think of the downside risk and margin of safety first. And for me margin of safety comes from business, management and valuation together.

Ambika is in a difficult industry but has never made a loss since inception. The business has been quite resilient in an industry where base rates are pretty horrendous.

The management is first rate and I draw a lot of comfort from their quality.

I am reasonably comfortable with the valuation. Current PE is overstated as economic depreciation seems to be lesser than accounting depreciation.

A downside risk here is that though Chandran sir’s yarn is niche and has higher realizations, a yarn price crash would affect his realizations also. But he is never made a loss and he has zero long-term debt currently (a very important point on MoS).

So for me, Ambika will survive in a very bad scenario. And there seems to be reasonable MoS.

Once I am reasonably sure of MoS, what is the upside? As you very rightly pointed out, it is heavily dependent of capex. If there is no capex the upside is pretty limited. Here what I am betting on is that over the past 15 years, if the management says capex is planned, they always end up doing it. So I am betting here on the management execution capabilities. But still, there is risk of execution here.

Given all the above, I think there is reasonable margin of safety, but growth depends on capex execution.

As such, my allocation for Ambika is ~4% of my portfolio, which could be changed.

Disc: Invested

5 Likes

Hi All,

Given that the company has been making optimum use of their resources most of the time, the profit growth of the company would directly depend on the capex that it puts in. At some point in time, the company will have narrowed down the bottlenecks and efficiency improvement will stagnate. So, it will come down to how much I sell, that is dependant on the capacity I have. That is, I have 10 spindles, I make RsX profit, now if I increase it to 20, i’d make Y. So, regular capex is the way to profit growth? That is, until the next capex, I’d continue to make similar profits and the jump will come after the capex is done. Is there anything that I’m missing out?

Disc: I’m invested, contemplating selling.

1 Like

Another steady quarter with good results and some 5%-8% improvement due to efficiency gains. Overall looks like current capacity utilization is to the fullest and they are constantly improving efficiency due to de-bottlenecking. Additional knitting facility coming up in Oct-16 should ideally add to profitability and margins further.

https://www.nseindia.com/corporate/RESULT_06082016143417.zip

Discl: Invested

4 Likes

Ambika Cotton looks like a good company with a good promoter. But is this business scalable? Trailing 12 months PAT is same as that in 2011? Such companies might turn out to be value traps. Just some food for thought!

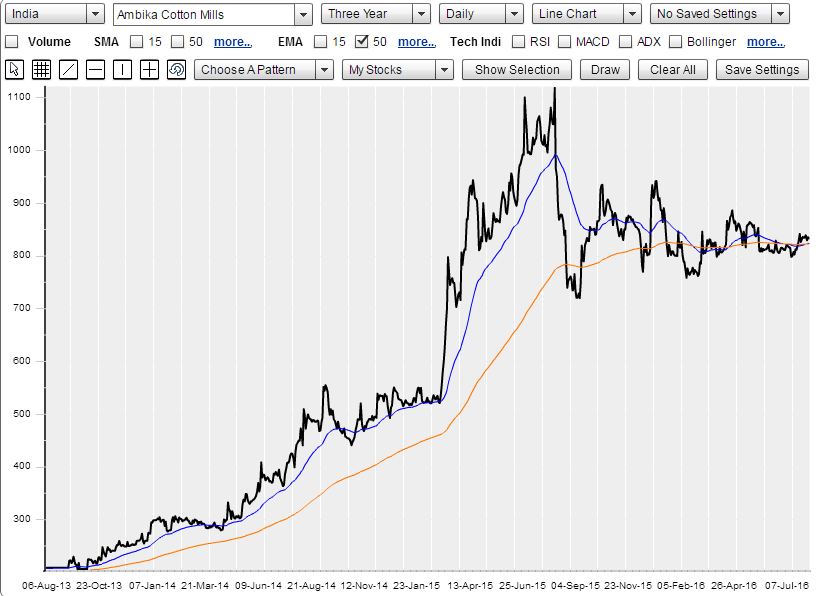

Hi @hitesh2710 & other technical experts,

Could you please have a look at chart below and give your views If theres bullish flag pattern forming in ambika?

To add to it, theres also a golden cross over (50 EMA over 200 EMA) as well.

Signs of breakout?

Thank you ![]()

Niranjan

Have you looked at the chart of Cotton lately? Did you see the reports on how cotton sowing in India has gone down by around 20% this year. DCM Shriram recently noted that their bioseeds division did badly, because there was a sharp drop in BT cotton sowing in North India.

I am not talking specifically about Ambica, which I believe imports its cotton, but in general to the Indian spinning industry, which has been greatly benefited by low cotton prices in the last few years, partly due to substantially increased production due to BT Cotton. If this trend reverses, then many of the companies will find it difficult, especially because they have all expanded and borrowed in the last few years. Companies like Nitin Spinners etc.

I had a position in Vardhman. Sold out a week ago.

Regards

Samir

5 Likes

@samir_brd Very relevant point that you have put in. I specifically like Ambika for the same reason. It is very conservative in doing capex and recent TUFS loan repayment suggests it stays away from borrowing as much as possible.

As Rohith had mentioned in his analysis, below 80% utilization most of the comapnies will be adversely impacted. While in case of Ambika since it has got good pricing power with good regular client base, plus conservative nature of management it is relatively well protected from the downward cycles. So, it may not give bumper profits in good times but will not get hit during the bad times as well. And as per my investment sytle, I keep capital protection ahead of capital appreciation when investing.

2 Likes

I am hearing similar things. One person I know worked at Ankur seeds in Maharashtra. He said that all seed companies are doing poorly in Maharashtra. 2-3 farmers also said sowing has gone down alot. Main reason for them to stop cotton is poor yields.

2 Likes

@ Samir

If rise in cotton price is all there was to a yarn business, then no sane promoter would set up a yarn shop in India. Yes there could be a disruption in regular business for 1-2 quarters, but this is self-correcting to some extent. Firstly, yarn prices may also follow and firm up. Secondly, we need to absorb that these entrepreneurs (read Nitin Spinners) are calculated risk-takers and understand the dynamics of cotton cycle better than you and me. These entrepreneurs have borrowed to expand as they see high opportunity of pay-back by the soft-interest loans extended to them by states.

If you are suggesting that ‘sell’ a yarn business when cotton prices are high and ‘buy’ it when cotton prices are low, then that may not be the correct way to ride the secular long-term growth of any business.

Keval

7 Likes

What r the implications for Ambika cotton mills whose main RM is Egyptian cotton. Egyptian Cotton Assn states 90% of products with the seal of The Cotton Egyptian contained no Egyptian cotton at all. Wellspun India Scandal opening Pandora"s Box??

Annual report for this year has been released today…

Anyone attending AGM tomorrow? I have few questions to ask to management. Thanks.

Amazon India is launching private labels in fashion along with Cloudtail (Amazon & Catamaran Ventures). Catamaran holds ~ 4% in Ambika Cotton. Could the Catamaran link mean business for Ambika Cotton?

1 Like

Maybe, but maybe not. Depends on the price points of the private labels. Ambika Cotton produces superior yarn that is used for high-end fabrics.

Hi,

I would like to know opinion from all invested in Ambika, about its future margins and PAT growth.

I am new investor in Ambika during past one year, and has not seen much uptick in sales and profits. I do understand that, capacity expansion and higher cotton prices have hampered PAT growth in the last one year. What is the likely scenario after 2-3 quarters? Is textile sector undergoing slow growth in general? Since I am new to textile sector, I am trying to understand dynamics of this sector.

My investment is for long term (Say, 3-4 years), and would like to know future prospects. I have invested based on reasonable valuations, debt free status and excellent management.

Thanks.

4 Likes

Any fundamental news for price volume action taking place since couple of days (particularly today…5x times avg volume with sharp upmove) or is this just CNBC video (link below) has led to increased participation in the counter? Thanks.

Disclaimer: Invested

1 Like

apart from a technical breakout point nothing much has changed…the expansion which was due for quite a long time has not yet been done as they have not received the clearance for that.

But maybe there may b some internal news u never know…

Disc: holding for a long time and still intend to hold…

1 Like

The reason for the up-move … News of the buyback.

Niranjan

Disc:Invested

4 Likes

Great news if this turns to be true…such strong signalling is necessary to show that stock is undervalued. We need to workaround math of minority shareholder rule (once the announcement is out) to see the potential benefits from buyback. Fingers crossed for now.

Disclosure: Invested