Alembic Pharma’s FY14 AR (even their FY13 AR was pretty good) pretty well explains company’s business and pharma sector as a whole. Reading the AR, one gets a sense that the company has a healthy pipelines of products for the international generic markets and international generic would continue to drive the growth for the company. Even in domestic market, the company plans to launch 2 divisions (respiratory and CVS) which should sustain growth. Apart from growth, the management emphasises on Return on Investment for any investment they make which is good for the shareholders. Overall, one gets a positive sense on the future course of the business after reading the AR.

Guys,

Today Alembic got some US FDA appoval on some drug, can sb explain what it means for it businesss in short and long term. I m not very good at these pharma stuff, thanks

Link: http://investingkitten.wordpress.com/2012/04/06/alembic-alembic-pharma/ http://investingkitten.wordpress.com/2012/04/06/alembic-alembic-pharma/ Link: http://investingkitten.wordpress.com/2012/04/06/alembic-alembic-pharma/

AlembicPharmaPosted on April 6, 2012 Link: http://investingkitten.wordpress.com/2012/04/06/alembic-alembic-pharma/ whatas respondentas itas demerged from Alembic Link: http://www.alembic-india.com/upload/05im.pdf a11). the businesses Link: http://www.alembiclimited.com/index.html donat Joel Greenblatt Link: http://en.wikipedia.org/wiki/Joel_Greenblatt recommended toAlchemy Link: http://www.alchemyindia.com/ aAlchemy companiesa. Shangri-La Link: http://www.alchemyindia.com/shangrila/index.htm Samsara project Link: http://www.alchemyindia.com/samsara/index.html acommission feesa donat

A report from CRISIL very well explains the risk associated with USFDA compliance:

http://www.crisil.com/Ratings/Brochureware/News/V5-Pharma%20Article%20EdV3.pdf

I think the main issue as highlighted by the report is the cultural issue of the employees.

1 Like

Results for Q1 FY15 are out.

Net sales up by 16% y-o-y

PAT up by 39% y-o-y.

Exports continue to do well, while Indian Generics and API businesses continue to show degrowth. Company filed 3 ANDA applications during the quarter and got approval for 3 ANDA.

Found an article on Microsoft site (though itas 6 month old) a

Pharma Company Goes Green, Reduces Carbon Footprint, Improves Productivity by 40 Percent

Alembic Pharmaceuticals are adopting technology (SharePoint 2013) and thus trying to improve on administrative hassles.

Alembic wanted significant control over processes in order to achieve a asingle source of trutha. Developing, maintaining and safeguarding highly sensitive information during development and production was the biggest priority for the company. Adhering to global compliance requirements was important too.

The case study shows how Alembic will benefit with this SharePoint implementation:

1 - Controlled Document Management System.

2 a Addressing Security Concerns.

3 a Reduces Time-To-Market.

4 - Improves Operations, Regulatory Compliance

5 - Increases Productivity by 40 Percent

6 - Reduces Paper Consumption and Related Costs

Hitesh, Donald, Ayush,

Any views on Alembic Pharma at current levels. I hold Alembic Pharma, Ajanta Pharma, Torrent Pharma, Natco and Polymedicure.

I was talking to a respected analyst today on pharma. He said pharma mid caps have become very expensive. He thinks people should sell some of their holdings and perhaps buy Cipla which can double from current levels. Cipla seems to have woken up after years. He also believes in 5 years a lot of mid cap pharma companies will find it hard to compete

There are just too many stocks in pharma and some expert inputs would be helpful to set the tone in the entire landscape.

Inauguration of Alembic Global Research at Hyderabad

https://www.slideshare.net/slideshow/embed_code/48339224

DMF Filing_Working.xlsx (2.4 MB) Approved ANDA.xlsx (17.6 KB) Key Launches in FY16 and FY17.xlsx (11.0 KB) Kotak Initiating Report_May 2015.pdf (207.5 KB)

Alembic Pharma looks pretty interesting. Please find attached the excel file on approved ANDAs, DMF file for future generic launches, key launches expected in FY16 and FY17 and recent report on Kotak on Alembic. The company has very interesting line up of generic launches during FY16 with the key being Abilify which has received very good response. Alembic along with Torrent, Hetero and Teva have received approval for generic Abilify . As per the Zauba link -

the export shipments to US have been more than Rs.2200 crore from April till date (zauba does give a good trend though not precise).

The key things to note in Alembic is that US will be the major driver for growth in the near term with Indian market expected to grow at 15 - 20% p.a. The key positives for the company are:

- No regulatory risk in the medium term: Their plant was just inspected by USFDA without any 483s or alerts (which is quiet an achievement given bigger companies like Sun, Lupin, Zydus have received 483s) and usually they conduct inspections once in two years. Also, with other companies having regulatory issues, the competition gets reduced as seen in Abilify with Sun and Zydus having tentative approval but not receiving final approval from USFDA.

- Interesting US pipeline with half of it being Para IV and some being FTFs: Along with big opportunities like Abilify, Namenda, Celebrex and Nexium, Alembic also has pipeline for niche molecules which are difficult to manufacture and don’t have much competition like Sular, Elmiron etc.Around 50% of its ANDA filing is Para IV which is much better than other mid sized pharma companies like Ipca and Torrent and as good as biggies like Zydus and Lupin. Although, Desvenlafaxine [505 (b) (2) of pristiq] didn’'t achieve much success, it does show the R&D capability of the company.

- Front end launch in US in FY17: The company currently launches its product in the US through its partners where it shares profits to the tune of 30 - 40% with them. The company will launch its front end marketing in US in FY17 which will result in margin expansion.

(Disclosure - Invested from lower levels)

18 Likes

Thanks Ankit,

This is excellent stuff! Thanks for sharing.

Any wannabe analyst at VP can take inspiration from Ankit’s compilation - this requires some hard methodical work, but everything is in public domain.

@vnktshb

You can talk to analysts - posts collecting some facts for yourself. Try going through Alembic Pipeline as shared by Ankit - and ask him more interesting questions - about Aripiprazole for example - why is this a blockbuster drug Or why it isn’t

Your previous “motherhood” question on all Pharma - was too mundane and frankly boring:)

Ask intelligent questions - which means put in some efforts to understand the domain - check the pipeline. Read a few reports on the company - and you will increasing your chances of extracting more relevant information - just like we do in Mgmt Q&A

Everyone should put up their hand - do some work - before asking to be spoon-fed, that’s only fair isn’t it:)??

5 Likes

@ankitgupta thanks for this wonderful collation on Alembic Pharma

@Donald

Everyone should put up their hand - do some work - before asking to be spoon-fed, that’s only fair isn’t it:)??

Point taken. My mistake. Will not happen again

Your previous “motherhood” question on all Pharma - was too mundane and frankly boring:)

Sounds too condescending. Don’t you think?

Disclosure: Invested from lower levels

Venkatesh,

Thanks for being fair and also prompt to point out where we may be going wrong:) …condescending…

Sorry if you have taken offense. My comment was meant to provoke “Action” …which you have already responded to. Thanks. From your allocations (and earlier comments seen), it is clear that you are NOT a novice. The fact that you are talking to Analysts, shows that you are not investing on “borrowed conviction”, should be investing for some years…and will have well-formed methods of your own.

VP is a meritocracy (unlike what some people think, VP is not a democracy) …and we are MORE DEMANDING …of the more informed-investors. Agree my comment was harsh & off-the-cuff and not well-considered. It certainly could have been phrased better …the essence however will always be the same …put your hand up…do some work…and ask intelligent questions …rather than open-ended questions like what do you think of this investment at this juncture …is not the sort of discussion we want to encourage at VP. We are extremely demanding of each other in closer groups, and increasingly will be for those who we think…can do much better

9 Likes

Super work Ankit.

Alembic Pharma the stock,has continued to surprise me.It was one of my first investments and I got out recently.

Pros: Strong cash generation.

Excellent & rising payouts.

Smart capital allocation(EBITDA growth vs. gross block addition)

Strong ANDA pipeline

Transparent management: the management has generally been conservative in its guidance & has called a spade a spade(it was one of the first cos. to come out & state,that DPCO will have a negative impact on their margins)

The approval for Desvenlafaxine was a big shot in the arm for them and was the first evidence of their R&D capabilities.The filings since then,have been strong.

The recent AR seems to suggest that the company is sacrificing short-term growth,in order to make its growth more sustainable in the long term.

Cons: It is one thing to identify a good company,but price is also very important.The valuations of Alembic today,seem to reflect all good that one can discount.

The topline growth has consistently been in low double-digits,since many quarters.

Inability to gain market share,even in exclusivity period(for the Pristiq generic)

The company had planned to setup its own front end by FY16.However,it has been delayed by an year.Certainly,they would have learnt from the Pristiq experience(though,it was marketed by Ranbaxy) but how can one be so sure that a company entering a new market,will come out all guns blazing? Lupin had a lot of problems when they started out in the US generics market.Plus,in the generics market…once the exclusivity is off,price wars escalate & it becomes very difficult to hold on to market share.

I feel market men are taking a highly optimistic view of the company.Things will take time to work out.As a shareholder,it seems that returns have come ‘front ended’,which means that results have been discounted way ahead of time.Moreover,the recent lethargy of USFDA has added to woes,even for Pharma majors.Thus,its surprising that the stock has continued its upward march.I feel there is a disconnect,which has kept on rising.Add to that,rising competition from Indian companies…entering/planning to enter the US markets.

Alembic is valued similar to Ajanta now!! A company that has grown way faster than its industry(even in tough times),has consistently reported rising margins.And all this,without sacrificing quality.The incremental RoEs have been very strong,and so have been the asset turns.Plus,Ajanta is yet to enter the US markets in a big way.

Scratching my head on Alembic!!

2 Likes

So India does not stand alone in fighting for generics. The need to cheap medicine globally with form a powerful incentive for the current patent model to stay.

Gaurav

Post the Affordable Health Care Act, there is a huge push even in the US for generics to bring down the cost for Medicare & Medicaid.

Hi Sagar,

I think many of us including me (I had sold out Alembic at 350 - 400 levels) had never worked on the pipeline of the company in detail and thus got impatient with slow growth during FY15 and sold out. FY14 was an exceptional year for the company resulting in high base for FY15 and thus we saw lower growth. We should accept the fact that growth will be lumpy in companies operating in US market depending on the product launches. It has a great pipeline and have around 15 - 16 products to launch during FY16 and FY17 among which some can have 180 day exclusivity (some of them are blockbuster products) or are complex to manufacture resulting in low competition. Not many companies have 50% of their ANDA pipeline being FTF or Para IV (am currently working on Torrent and I can clearly differentiate between it and Alembic in terms of product pipeline). Even if 30% of this product are successful (company gets 180 day exclusivity), we would see good growth in their US business.

Coming to the run up in price, it has run up in anticipation of good results during Q1 and Q2 due to gAbilify (aripiprazole) being launched by the company. Given its small US sales (around Rs.350 crore during FY15; good thing is they gave a break up of sales to North America in this year’s AR), market is anticipating huge jump in sales and margins during the two quarters.

Coming to desvenlafaxine (Pristiq’s NDA), I think we dont know what happened on the marketing front (Ranbaxy was the marketer). But it does show company’s R&D capability. It spends 6 - 7% of its revenues on R&D which is pretty high given its size. In FY15’s AR, they have mentioned about entering into areas other than tables for US market like injectables etc.

In terms of setting up front end marketing for US, what I have observed is it takes a certain scale and lot of time to penetrate in the marketing. Approval from all the states is required and company has to launch few me too products as well to penetrate the distributors. Alembic is doing that and hopefully should launch that in FY17. Comparison with Ajanta wouldn’t be fair as it has shown a linear growth and I believe its an exceptional company. Ajanta has filed 23 ANDA and we are not sure about its pipeline as its not backward integrated into APIs (doesn’t file DMF). They do claim that the addressable market size of those molecules is around USD 1.5 billion. We need to ask Ajanta’s management about their front end set up in US and state wise approval (would totally agree that they are one of the smartest guys in terms of marketing as we would have seen from their first time launches and their ability to identify untapped markets). Am planning to attend Ajanta’s AGM and ask such questions.

13 Likes

Great work @ankitgupta.

More good news for Alembic/Torrent and further set back to Otsuka. No direct impact as such, but definitely a positive takeaway for future similar lawsuits.

3 Likes

Alembic receives tentative approval for gCelebrex -http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Search.DrugDetails. It had a market of USD 2.56 billion before entry of generic players. Teva, Mylan, Lupin, Apotex and Watson have already launched the generic. Till date only Alembic has received tentative approval. About the drug - Celebrex is used to treat the signs and symptoms of osteoarthritis, rheumatoid arthritis, ankylosing spondylitis, acute pain in adults, painful menstruation, and juvenile rheumatoid arthritis in patients two years or older.

2 Likes

Alembic receives approval for gPristiq (Desvenlafaxine Succinate) along with Lupin, Mylan and Sandoz. Prisiq is USD 538 million (pregeneric) molecule and marketed by Pfizer in USA. Alembic had NDA [505 b(2)] for Desvenlafaxine and sole exclusivity for 30 months received in March, 2013. Ranbaxy had the marketing tie up with Alembic for the product. However, it didnt meet expectations as it was difficult for customers to switch from innovator to the generic product and even the regulatory issues faced by Ranbaxy could have affected the sales.

3 Likes

Edit: Sanitized Zauba export data; deleted obvious duplicate entries (taking clue from Ankit’s comment)

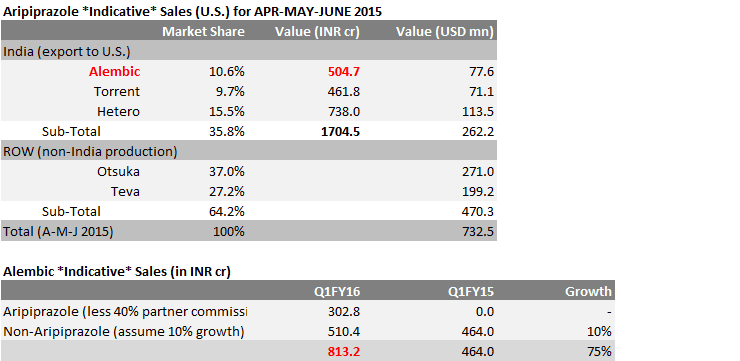

Alembic Pharma could be in a different orbit shortly - Thanks to gAbilify. Some data to chew -

Source: https://pbs.twimg.com/media/CHygV0RUwAAiJPL.jpg:large

- Aripiprazole Market Share (U.S.): Torrent 9.7%, Alembic 10.6%, Hetero

15.5%, Teva 27,2% and Otshuka 37% - Indian companies (i.e. Alembic, Hetero and Torrent) together shipped 1704cr of Aripiprazole to U.S.

in A-M-J 2015 - Indicates Alembic shipped ~504cr

- Less ~40% U.S. partner share, means ~302cr possible increase in Alembic’s Q1FY16 sales from Aripiprazole

- Assuming API serviced by Alembic’s captive use, means significant margin expansion possibility

{kind=link}

- Qtrly-sales number MAY NOT be equal to Qtrly-shipment number (caused by a typical revenue recognition delay)

- Please DO NOT focus on the accuracy of Q1FY16 ballpark estimates; primarily meant to illustrate the magnitude of the impact of gAbilify on Alembic’s sales number (orbit changing)

Details in the attached spreadsheet.

Alembic (Aripiprazole) v2.xlsx (309.8 KB)

Hat’s off to @ankitgupta for sharing invaluable pointers.

11 Likes