Advanced Enzymes Q3 Results:

Q3 FY20 IP:

From Q2 FY20: (For Comparison/Outlook of the year)

Q3 FY20 CC:

I’m delighted to announce that we have a considerate growth in terms of profitability. This is mainly because of the product mix. Our business in India had positive results and has been up by 15%. Evoxx, which is our subsidiary in Germany is EBITDA positive in the current quarter as compared to the previous quarter and growing steadily. The EBIT for evoxx is also on the positive side.

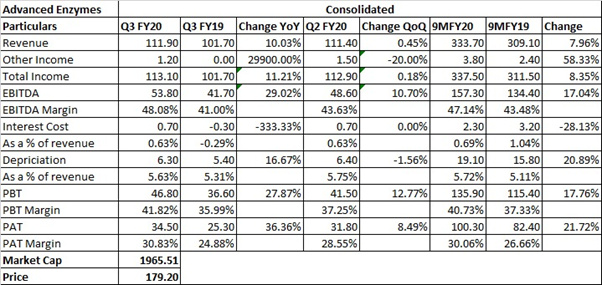

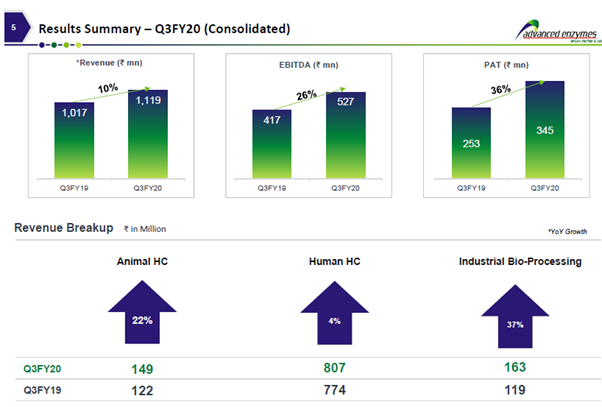

Our sales on year-to-year basis is on positive side and has an upstream of INR 102 million and has grown from INR 1,017 million to INR 1,119 million. That is approximately 10% growth in the revenue. Correspondingly, the EBITDA has increased by INR 112 million from INR 417 million – to INR 417 million from 259 – sorry, from INR 417 million to INR 529 million, and that is approximately 27% growth in EBITDA. And as a percentage of total sales, EBITDA is having a percentage of 47% as compared to 41%. Our consolidated PAT for this quarter has also increased by 37% from INR 253 million to INR 346 million in the current quarter.

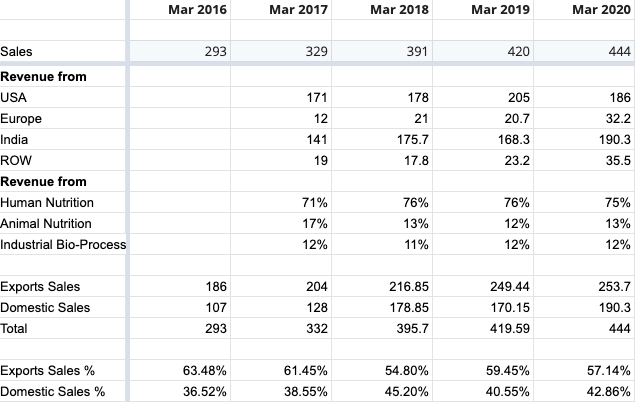

Revenue Details: The top product, which we have sold in the current quarter is serratiopeptidase. One minute. So Rohit, the sale for the top product is INR 9.5 crore versus INR 23.6 crore of quarter 3 December '18. The U.S. revenue has contracted significantly, but India’s revenue has gone up. So that overall basis, it’s like 10% growth from the quarter 3 '18 to this. But if we just remove the top customer, the growth is much higher. So the top client contribution is 9% in this quarter compared to 23% in the last quarter. So the evoxx sale is INR 57 million, INR 5.7 crore this quarter, and EBITDA is INR 1.77 crore. Not much dependence on China or raw materials.

Future: Will be able to achieve guidance of FY’20 PAT wise but not revenue wise. Our strategy is now to consolidate our various different strengths in areas and stay focused on the marketplace where our strengths are. So we continue to consolidate our position in the market where we have normal strength. And we feel that our growth will accelerate, hopefully, after further 3 to 4 quarters. Planning to invest more in R&D in the next year (CAPEX). We just acquired, in this quarter, a land of 15 acre in Nashik, and that we are building up a modern R&D center. And we are thinking about INR 100 crores in the next 3 years as a capital investment for the R&D center. Planning to add in more workforce to marketing in order to have a more focused approach.

Q2 FY20 CC: (for comparison)

Evoxx: The substantial increase in profit is primarily because of additional gross contribution on increased sales and lower financial cost. EVOXX is doing substantially well. It became EBITDA positive in the previous quarter and has registered 59% growth against the last quarter. EVOXX the top-line is INR 58 million and EBITDA is INR 13 million and then we have a amortization of about INR 17 million for this quarter as compared to the previous quarter of top-line of INR 56.5 million and EBITDA of about INR 8.2 million and amortization of about INR 15 million.

Industry Future: We are progressing towards meeting our goal for financial year 2020. Although the revenue growth is in single-digits, the bottom-line has shown a significant uptick as compared to last year. Next two years we see, probiotic, human nutrition, animal feed, bio catalyst, and the food industry, bakery industry, these are various which will take us further.

Raw Material Prices: Yes, when you see the raw material, it is because of some changes on product side when the sale mix is changed, number one. Number two, if you really compare YTD numbers, you will not see any drastic change, it is on quarter-to-quarter the change you are observing on, right? But if you see year-to-date number, year-to-date numbers are more or less similar. Last year, we had spent about I think 18% on raw material consumption and this time it is about 19%. So, there is a 1% extra and that comes because of some changes in the price of the input whatever we use. So there is no major change as such. So you look at the quarter-to-quarter basis it is like you need to see it on a broader perspective and a year-to-year basis.

Financials Future: Revenue Growth of about 10% in the future. EBITDA margins to be maintained between 40%-48%. Will increase in the future.

Top client contribution: 14%. (reduced to 9% in q3fy20 which is positive)

Disclaimer: Invested