I have written a brief note on Aarti Drugs Ltd.

Aarti Drugs (CMP - 549.30; Market Capitalization - Rs.1295 crore)

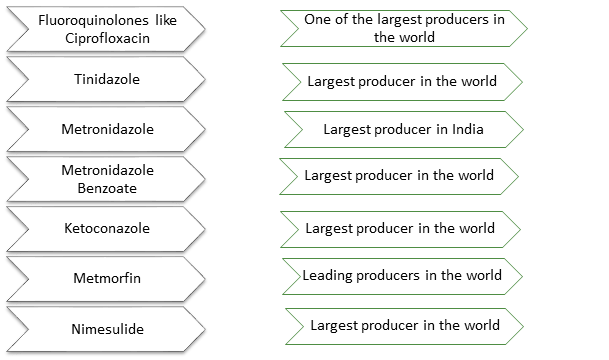

Aarti Drugs Limited (ADL) is engaged in manufacturing of active pharmaceutical ingredients (APIs), intermediates, specialty chemicals and formulations. During FY18, on a standalone basis, APIs and intermediates contributed 96.80% of sales. The company has 10 manufacturing units in Maharashtra and Gujarat. Domestic markets contributed 63% of the sales while exports contributed 37% of the sales of the company. The company has presence in 90 countries in regulated (except US), semi-regulated and unregulated markets. Top 10 export countries include Brazil, Mexico, Pakistan, Bangladesh, Turkey, Netherlands, Indonesia, Vietnam, Spain and Sudan (source: AR - FY18). Within the API Segment, Antibiotic Therapeutic Category contributes to around 37.66%, Anti-diarhoeals around 20.64%, Anti-inflammatory around 10.94%, followed by Anti-fungal, Anti-diabetic and Cardioprotectant Therapeutic categories during FY18. Over the years, the company has been trying to increase the proportion of lifestyle diseases like diabetes, cardiac related issues in its overall sales. The company is a market leader in India/World in many of its products. Products under APIs includes Ciprofloxacin Hydrochloride, Metronidazole, Metformin HCL, Ketoconazole, Ofloxacin etc. whereas Specialty Chemicals includes Benzene Sulphonyl Chloride, Methyl Nicotinate etc. Top 10 products contributed to around 75% of the total revenue of the company. The company has an installed capacity of 2,143 MT per month and capacity utilisation was around 75% during FY18.

(source: company’s annual report and presentation)

Customers

The company has a diversified customer base of over 300 customers. The client concentration risk is low as top 10 customers contributed less than 20% of the sales. The key clients of the company are given below:

The company has a diversified customer base of over 300 customers. The top 10 local clients contributed just 19.75% of total domestic sales while top 10 export clients contributed just 25.78% of total export sales. The topmost client in domestic markets (JB Chemicals) contributed 3.51% of domestic sales while in exports (Sanofi Aventis, Pakistan) contributed 5.60% of export sales. The key clients of the company are given below:

Backward Integration into manufacturing of intermediates

Over the years, the company has been trying to backward integrate by manufacturing intermediates and reduce its dependence on imports particularly China. It is backward integrated into many of its top molecules. The development of these intermediates will protect the company in case of shortage of raw material for China as well as protect it against any increase in the prices. Furthermore, any increase in prices of the final products will help in improving its profitability. The company has done capex of more than Rs.450 crore over the past 4 - 5 years and some part of it has also gone into backward integration.

Some of the snippets from the annual report regarding backward integration is given below:

(Source: AR – FY14)

(Source: AR FY15)

(Source: AR FY16)

Source: AR FY17)

Formulations

During FY15, the company acquired Pinnacle Life Science Pvt Ltd (Pinnacle) which was engaged in toll manufacturing for formulations. Pinnacle has one formulations facility at Baddi. ADL transferred its formulations business to Pinncale. ADL has tied up with a European distributor on profit sharing basis for formulation sales. The company has filed dossier formulation products with European regulators and UKMHRA out of which three products have got approval in Europe and two products (Zolpidem and Celecoxib) have got approval in UK. The performance of Pinnacle has also improved consistently post acquisition by ADL. During FY15, Pinnacle reported revenue of Rs.13.30 crore and net loss of Rs.3.20 crore during FY15 while it reported revenue of Rs.139 crore and PAT of Rs.9.01 crore during FY18.

R&D and product pipeline

The R&D facility of the company is located at Tarapur and consists of 2 Ph.Ds, 70 MScs, 9 BScs and 18 engineers. The company has expertise in various reactions. The R&D team has also helped the company in backward integrating by developing of intermediates & raw materials. The company spends around 0.50% - 1% of its revenue on R&D expenses.

Large Capacity expansion done over the years

Over the past five years ended March 31, 2018, the company has done capex of more than Rs.450 crore. The capex has largely been deployed to increase the capacities, for backward integration and for pollution control equipments. Despite such a large capex (more than doubling of gross block), the company’s sales have hardly grown from Rs.971.75 crore during FY14 to Rs.1,263 crore during FY18. The company’s asset turnover at around 1.20 times is at 5 – 6 years low.

The low growth in revenues is on account of following reasons:

-

Stricter regulatory norms and prolonged gestation period in APIs: The same has also been highlighted in the company’s FY16 annual report as highlighted below:

(Source: AR FY16)

-

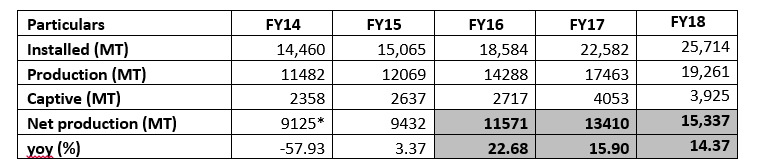

Decline in prices of crude leading to low value growth despite growth in volumes: On account of decline in prices of crude, there hasn’t been growth in revenues of the company despite decent growth in production volumes during the past 3 years. The details of installed capacity and production is given below:

*

-

Issues in key export markets like devaluation in currency, decline in crude prices impacting the economy etc and challenges faced in the domestic markets: Company’s key export markets like Brazil, Latin America, African countries have faced challenges including devaluation of currency, decline in crude prices impacting the economy and political issues. Furthermore, the domestic pharmaceutical markets faced issues like NLEM, demonetisation and implementation of GST which has impacted growth over the past three years.

-

One off events like demonetisation, GST, fire at adjacent plant impacting one of the units during Q4FY18 and pollution authorities shutting few of the units of the company: During the past few years, the company’s performance has also been impacted by one off events like demonetisation, GST, fire at adjacent plant impacting one of the units during Q4FY18 and pollution authorities shutting few of the units of the company.

Improvement in working capital intensity of the company: There has been significant improvement in the working capital intensity of the company as reflected in reduction in debtor and inventory days (except for March 31, 2018). The same has led to healthy cash flows from operations generated by it.

Regulatory issues

Except from USFDA, the company has approval from major regulatory markets of the world including Europe, UKMHRA, Korean FDA, ANVISA (Brazil) etc. The company hasn’t been able to resolve the USFDA issue for the past many years. Even the recent December, 2017 inspection seems to have failed. However, currently, the company doesn’t derive any revenue from US. USFDA approval whenever it comes will be an optionality.

What attracts me to the company?

-

One of the lowest cost producers of APIs: The company normally enters a mass market API where the market is highly fragmented. It is 7th- 8th player to enter the market for the particular API. Over the years, the company consolidates its market share because of its chemistry skills and scale. It becomes one of the lowest cost producer and one of the largest players in that particular molecule.

-

Attractive valuations and no one is talking about the company: Trading at 13 – 14 times TTM earnings and 9 – 10 times EV/EBITDA, the company’s valuations are not expensive. It seems not much growth is factored in the valuations. Furthermore, no one is talking about the stock currently. Once touted as potential ‘100 Bagger’ , not many analysts track it now.

-

Issues in China to boost growth in prices and volumes: China is the hub of APIs of the world with it supplying 70 – 80% of the world’s API requirement. Like other chemicals companies, even API companies are facing issues due to environmental clampdown, increasing fuel and manpower cost etc. The same is expected to benefit companies from India. Furthermore, a backward integrated player like ADL is expected to benefit from it. The same is expected to provide level playing field to API companies from India.

-

Anti-Dumping Duty (ADD) on ofloxacin and its intermediate O Acid: During December, 2017, the Government of India has imposed ADD on import from China of ofloxacin and its intermediate O acid for three years. The same came into effect from April, 2018 onwards. ADL is the biggest player in the segment and is the only player in India which manufactures its intermediate O Acid.

-

Promoter’s track record in Aarti Industries: Gogris and Patil families are the major promoters of the listed entities of Aarti group. The promoters have a track record of successfully scaling up business in their flagship company, Aarti Industries. Furthermore, the corporate governance track record has also been pretty good. Promoter group has increased their stake in the company from 48.36% during FY08 to 62.51% currently.

Key Risks

-

Can the promoter’s mind-set of running a chemical conglomerate become a challenge in running a pharmaceutical API company?: Aarti group has primarily been a chemical conglomerate running many chemical companies. The regulatory requirements of running a pharmaceutical API company are more stringent compared to a chemical company. The company has not been able to resolve the USFDA issues for almost five years now. Furthermore, some issues like pollution control and fire incidents do give some discomfort.

-

Customers in doldrums can the supplier make money? The whole pharmaceutical industry in India is going through a rough phase whether it is on domestic side due to price cap or in exports in key markets of US. The pricing pressure might be high from such customers. However, ADL might have some bargaining power being the largest player in some of the products and issues in China.

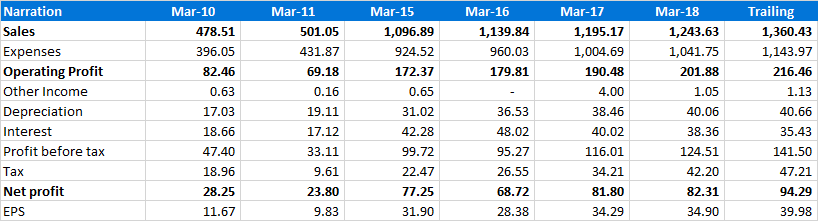

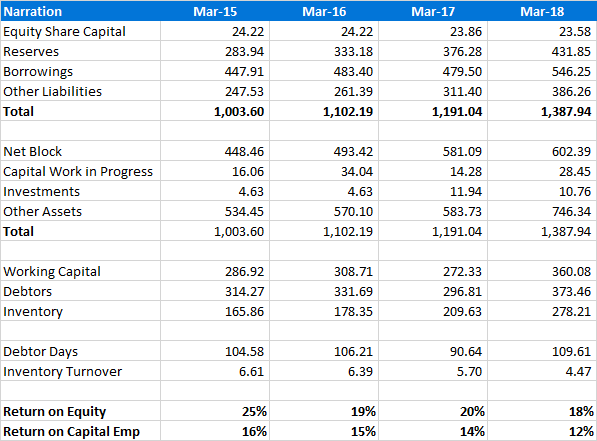

Key Financials

Profit and loss (consolidated)

Balance Sheet (consolidated)

(source: Screener.in)

(Disclosure: This is not a recommendation or an advice to purchase the stock)