@ankitgupta

Did u come across any production or sales figure molecule wise, so that we could relate to the growth potential in the company with the existing products.

Aarti drugs interview on Bloomberg regarding China supply issues

1 Like

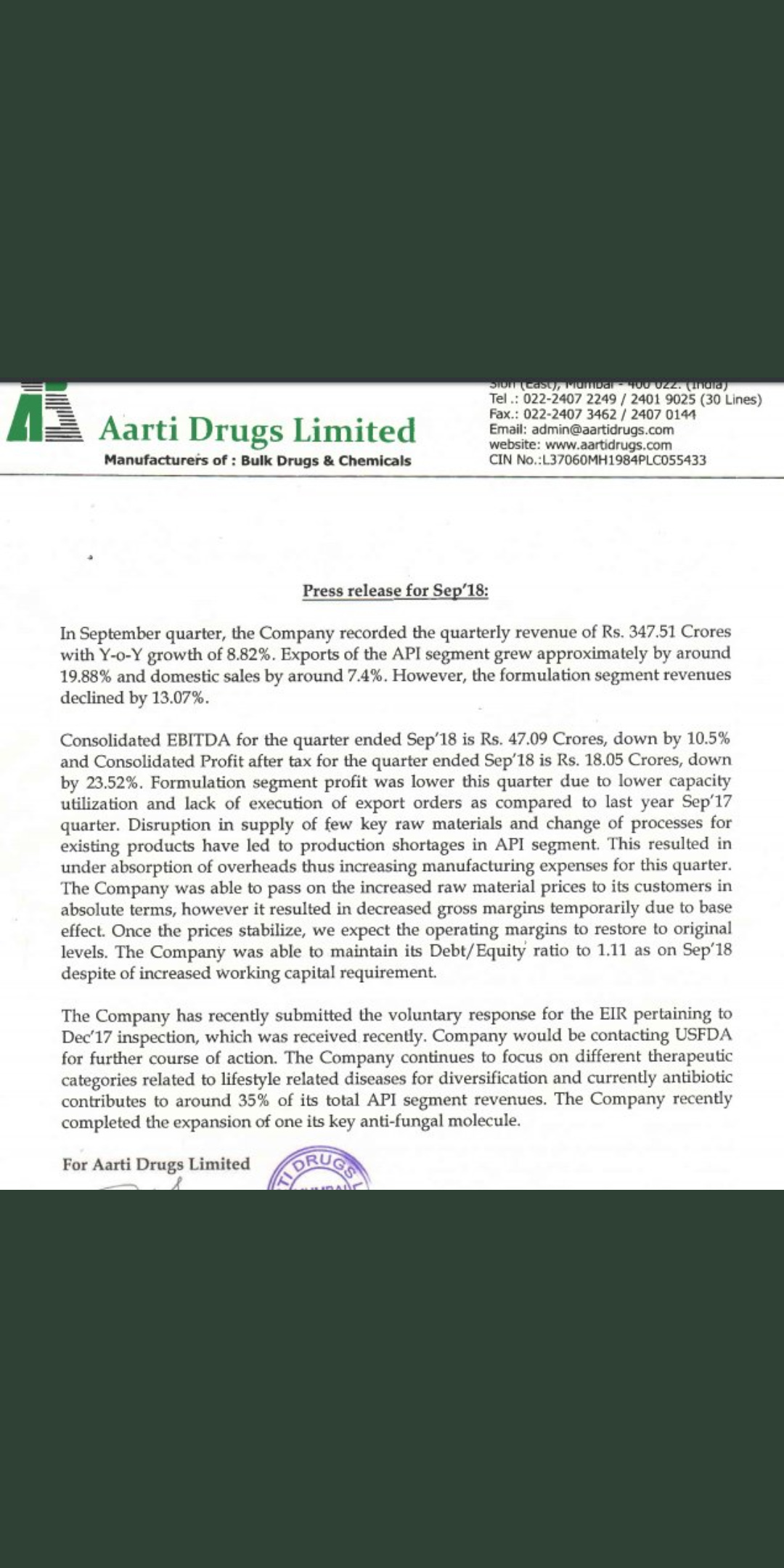

In the September’19 quarter, the Company recorded consolidated quarterly revenue of Rs.477.50 Crores with year-on-year growth of 37.45%. Domestic sales of the API segment grew by approximately 46.5% and exports by 26.57%. Entire growth of the API segment is driven by volume growth. Formulation segment revenues grew by around 29.75% on year-on-year basis.

Consolidated EBITDA for the quarter ended September’l9 is Rs.68.50 Crores, up by 45.45% and consolidated profit after tax for the quarter ended September’l9 is Rs.32.31 Crores, up’by 79.01% on year-on-year basis. Consolidated EBITDA margin improved by approximately 0.8% as compared to previous Jun’19 quarter due to higher utilization of production capacities. Company expects to improve on its gross margins in future due to better efficiencies in production. Due to continuous improvement in working capital management Company was able to further reduce its Debt/Equity ratio to 0.83 as of September’l9 o.n consolidated basis.

Company recently expanded its anti-Aiabetic capacity and currently scaling up its production quantities for the same. Further brown field CAPEX would be done in the current financial year to expand few capacities in antiinflammatory therapeutic category. Exports markets are slowly opening up for formulation division and it will drive the margins for that division.

2 Likes

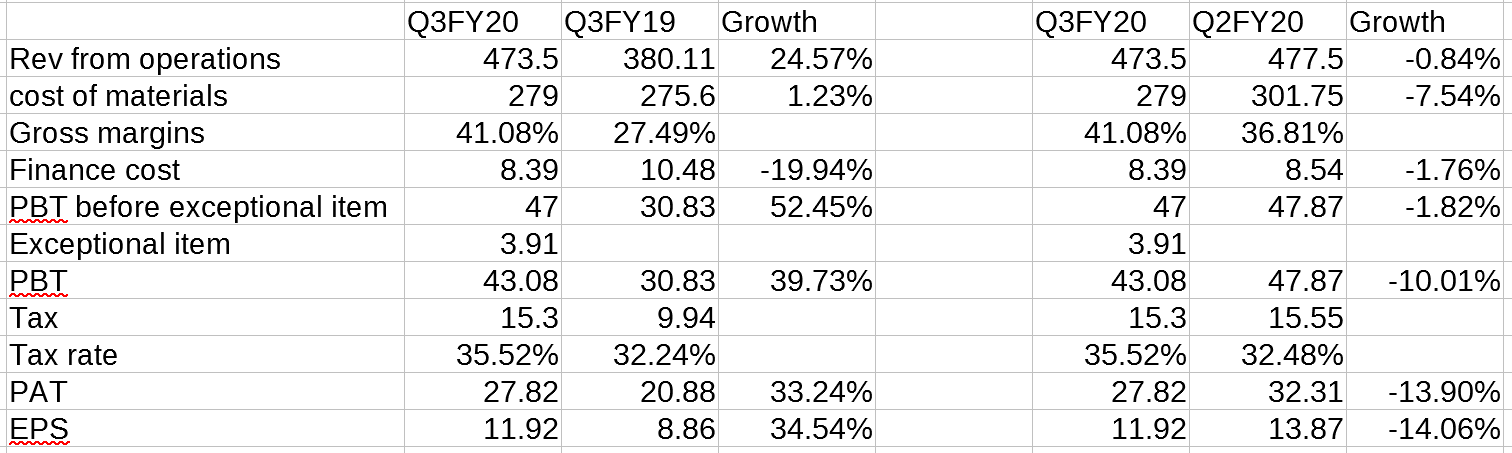

Q3FY20 results were out today. Below are the results. Company declared interim dividend of Rs 2.

Comments- Very good numbers again with good margin expansion. Finance cost has come down further. Will wait for press release commentary on utilization (if any) and volume growth/pricing as revenues are flattish qoq.

3 Likes

Press release-

revenue of Rs.473.51 Cr up 24.57%yoy.

- Domestic sales of the API segment grew 26.39% and exports by 5.27%. Entire growth of the API segment is driven by volume growth.

- Formulation segment revenues grew 72% yoy.

- EBITDA for the quarter ended December’19 is Rs.63.82 Crores, +22.68%

- PAT=Rs.27.78 crores, up by 33.01% yoy.

Company expects to improve on its gross margins in recent future due to better efficiencies in production.

Due to continuous WC management Debt/Equity ratio reduced to 0.70.

Company recently expanded its anti-diabetic capacity and successfully scaled up its production quantities for the same.

Further brown field CAPEX is in progress to expand few capacities in anti-inflammatory therapeutic category. As expected, Export markets are opening up for the formulation division and it will drive the margins for that division

Comment- Good reduction in debt levels. Debt/equity trend is shown as follows. Q3FY20 had a sharp reduction

March19= 0.91

June19= 0.9

Sept19= 0.83

Dec19= 0.7

As per Care report dated 25 Dec 2019, “The company has done capex of Rs.70.96 crore during FY19 & further capex of Rs.32.93 crore during FY20, which is for the multipurpose facility of vitamins/anti-inflammatory segment to target regulated markets…The company has a planned capex of around Rs.120 crore over FY20 and FY21.”

Company should do an EPS of about 47 for FY20. So it trades at a valuation of about 13x. Debt reduction, margin expansion (from higher formulations mix, lower RM, backward integration) and growth from expanded capacities should help in coming quarters.

2 Likes

Aarti Drugs Q3FY20 Concall Summary

Business Update

- Domestic API sales grew by 26% and exports by 5%

- Entire growth in API segemnt is driven by volume

- Formulations business grew by 74%

- Segmental revenue Dec 2019

- API: 86%

- Formulations: 14%

- Anti diabetic capacity has recently come up and functioning smoothly

- Exports market are opening up for formulation business and will drive margins going forward

Participants

- DSP Mutual Fund

- Turtle Capital

- HDFC Securities

- Sameeksha Capital

- Nirmal Bang

- Quest Investments

- Equitymaster

- Unifi Capital

- Centrum Broking

QnA

- Raw materials supply uptill March is covered and new supplies from China are expected to come up by February end if things improve

- If corona virus situation persists for another month situation could become negative fro supplies

- Enough raw materials to cover till 15th March

- If China stops shipments completely there is an Indian source for the same and after 15th March company will be able to operate at 60% of its capacity

- Currently operating at full capacity of the anti protozoal product of which supplies come out of China

- If China shuts down completely 20-30% of the revenues could get affected in the future

- However since finished goods prices have also started going up volumes will decrease but some of it can be managed through higher margins

- Currently not entering into long term contracts because unsure of raw material availability

- Have empanneled with a veteran of the pharma industry and expecting a USFDA audit to be triggered as one of the customer using the DMF is getting their plant audited

- Capex for 9MFY20 is around Rs 30 crores

- Doing an incremental specialty che mical capex of Rs 50 crores in FY21

- Insurance costs have gone up 5 times due to new regulations by the government

- The specialty chemicals plant can take 18-24 months for revenue to kick in

- Long term borrowings stand at around Rs 216 crores and short term around Rs 194 crores

- In some of the products prices have gone up by 10% due to perceived shortages happening in the future

- Currently 60% of raw material is imported and out of it 70% comes from China

- Asset turns vary from 2 - 2.5x for API and 4 - 4.5 for specialty chemicals

- Expanding footprints of formulation business to newer countries and registrations happening over last two years are now getting commercialised

- Currently utilising 70-75% of caapcity of formulations

- Margins in specialty chemicals are 4-5% higher than in the API segment

- Within the API segment margins vary between products

- Realisations in December quarter has been slightly lower than last year and growth has come entirely from volumes

- Able to sell higher capacities in the market and forseeing capacity utilisation to remain higher next year as well

10 Likes

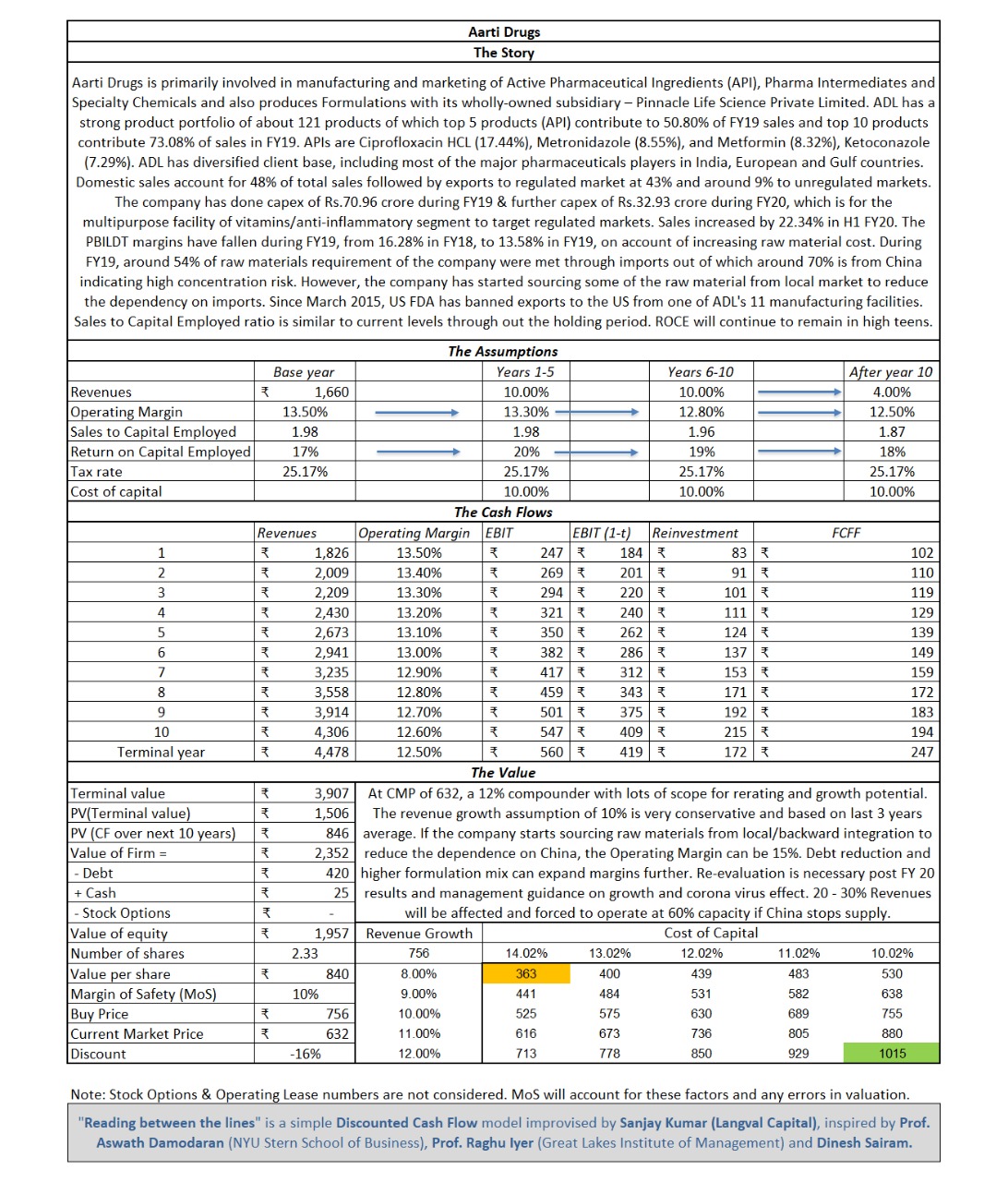

I did a very basic EPS based DCF to see if it was undervalued. It was.

I then went on to do a full DCF based on assumptions I am comfortable with. I used the latest results, concall summary and credit rating reports to arrive at the final model. I couln’t finalise the revenue growth assumption and I ended up using the 3 year averge. Would love the community’s thoughts on improving the model, especially on the major drivers - Revenue growth, Op. margin, sales to capital, ROCE and cost of capital.

- Wannabe value investor

- Bought some qty at 639 on Friday. Will buy more next week.

6 Likes

27 Feb 2020…interview of the CFO.

He sounds optimistic.

Expect a good q4 from Aarti Drugs.

Disc- invested.

Regards,

Ranvir Dehal

1 Like

Aarti Drugs Q4 results

Disc: Invested

Aarti Drugs Q4,FY20 concall was a very elaborate and comprehensive one.This is what all I can recall:

-

Q4 revenues were affected due to difficulty in cargo movement.Finished good prices had risen so it helped margins.However,most of the rise came during end-March so the real impact of rise will be felt in Q1.At the same time costs will be higher due to Covid related measures.

-

Currently operating at 70% utilisation.Earlier number was 75-80% range.Thus,it seems production is down about 10-12%.On the other hand,they have increased capacity a bit.So,this reduction is on a higher base.I am not completely clear on this.

-

Company expects to do 10-15% volume growth for FY21.EBITDA should be in the 15-16% range with chances of upward revision.

-

About 100cr. capex planned for FY21.Company generated around 200 cr. FCF in FY20.Most of it was used to reduce debt.Fy21 FCF is expected to be higher still.Thus,debt component in capex maybe quiet low(mgt had earlier guided for a 75:25 split between debt & internal accruals)

-

Government’s API policy in the current form will end up hurting the industry.Aarti has made recommendations for fine-tuning.The good part is that the ministry is willing to listen.Mgt even said that one govt. official called them up for suggestions.As of now,there is little clarity on how it will pan out.

-

Major capex plans will get delayed by 6 months.However,Aarti has adequate capacity for 25% kind of growth from here.

The management seems to be aware of the market conditions at all times and they are able to consistently ramp up specific therapies when demand is strong.From their commentary,they seemed very certain that situation will normalize once lockdown is removed.Even otherwise,a company able to operate at 70% and get good realizations is very rare in such times.While the end product prices may come down once lockdown is lifted,the company has enough in it’s arsenal to grow 15-20% with similar if not better margins.The next few years will see the company do atleast 2-300 cr. capex for it’s various products.They seem to be well placed for the next phase of growth.

Disc.: Invested,views are biased.

14 Likes

DGTR conducted an antidumping investigation on import of ciprofloxacin Hcl from China.

Aarti drugs ltd was the main applicant and supported by Godavari drugs ltd.

43% of total domestic production is by Aarti drugs.

Ciprofloxacin Hcl mainly imported from 4 companies from China

Dumping margin from 0-40% depending on the company.

Domestic industry sales 908 MT in fy16 to 1007 MT in Period of investigation.

Imports have grown from 117 MT in FY16 to to 347MT during POI.

Domestic industry has suffered material injury due to dumped imports.

Authority recommends an anti dumping duty of 0.9 to 3.2 US$ per Kg on different exporter companies from China.

Not sure when the final notification will come from Govt, being the major producer Aarti drugs should benefit from this.

http://www.dgtr.gov.in/anti-dumping-cases/anti-dumping-original-investigation-concerning-imports-ciprofloxacin

Discl:invested

4 Likes

Normally in such situations, for what period is the anti dumping duty imposed ? All I am trying to ascertain is the sustainability

2 Likes

Current anti dumping recomendation is for period of three years from the time of Gazette notification as mentioned in the above document.

Even in the past another Aarti drug product ofloxacin, anti dumping duty was for 3 years from the beginning of 2018 and likely to end in 2021. anti dump ch 30.pdf (73.9 KB)

I think these are subjects to changes and sometimes

companies will approach Govt to extend the anti dumping duty based on market condition of particular product.

3 Likes

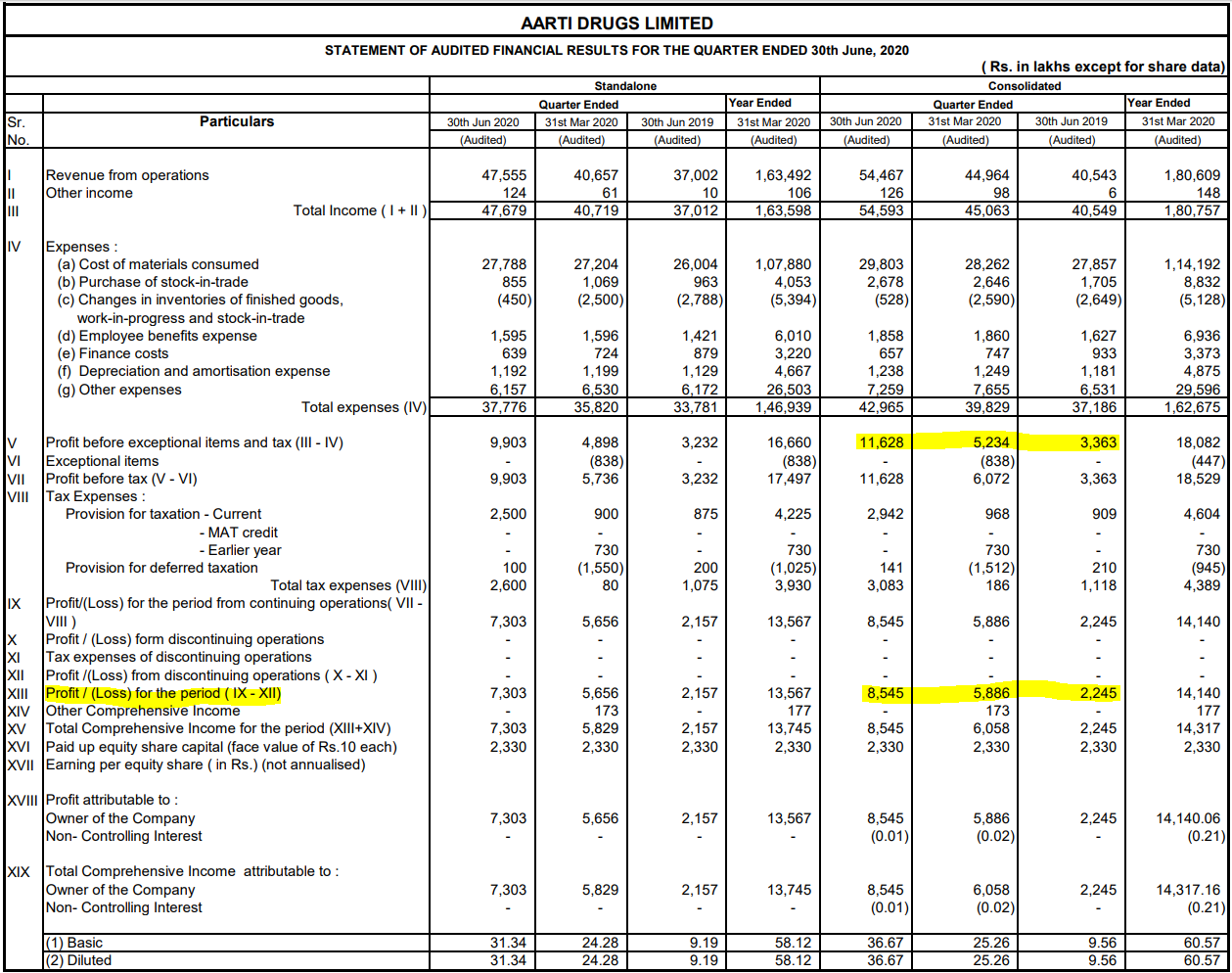

Really good Q1 Fy21 results:

QoQ: Revenues 25% up, PAT 50% up

YoY: Revenues 30% up, PAT 400% up!

https://www.bseindia.com/xml-data/corpfiling/AttachLive/de40c809-8317-4e7e-975f-5f896e9a3950.pdf

How such super performance? Some ADD kicked in already?

Disc.: Invested

5 Likes

Just a Guess, may be Local Procurement theme playing out, due to supply chain disruption.

1 Like

Aarti Drugs concall was a delight to attend with lot of industry specific insights.Some highlights:

-> 50/50 split between volume growth and realization growth in Q1.Volume growth could have been higher,if April ramp-up was better.Expect better volume growth in coming quarters.

-> API segment spillover of 10-15cr.,formulations 5-6cr.So around 20cr. revenues got deferred from Q4 to Q1.

-> Prices for most end products have gone up,as indicated earlier.However,this could be because of supply issues due to lockdown,etc.Q2 also prices are good.Tough to say when and where they will normalize but don’t see them getting back to earlier low levels.Guidance of 18-20% EBITDA margins for FY21 conservatively.

-> Peak revenue on standalone basis ~2200cr. on 3-4 month old prices.Formulations peak revenue is immaterial since subsidiary is IP owner and can easily outsource manufacturing.

-> Structurally,margins for the industry have moved higher.Chinese competitors have increased their prices.This has triggered better prices for companies like Aarti.Earlier,Chinese companies were even selling at low single-digit margins.This has changed now.Chinese players are now cognizant of profitability.

-> For any industry,high margins attract competition and are thus unsustainable but for API companies in the current scenario with stricter compliance norms on environmental and regulatory side the competition should be very limited.So,players like Aarti and other large players should have a good run.Company expects 18-20% as sustainable margins vs. 15-16% earlier.

-> Formulations segment continues to do well.Expect to finish this year with ~250-80cr. revenues.Order backlog is very strong.Will keep entering new markets and introducing new products to keep up the growth.Gross margins should also keep trending higher.

-> Company has followed the strategy of ramping up and introducing import substitutes since 6-7 years.With central government getting very active in supporting the same,Aarti will benefit.Even globally,seeing a trend of China+1.

-> Supplies from China have normalized completely.In case of severe disruption,company can buy from some domestic players.Price differential will be 5-10%+ but that can be easily passed on.Aarti in any case,continuously keeps looking at backward integration.So,that when supply disruptions occur company can manage well.

-> USFDA audit has gotten delayed due to Covid.However,company was able to reach out to some officials and has been told to get a third party validation of all the changes Aarti has made to be compliant with the objections raised by USFDA.This won’t take long(I think mgt mentioned end-August as a possible timeline)

-> Aarti is also looking at mfg. of some new intermediates covered in the govt.'s new policy.Over the next few years,3-400cr. of capex is in the works.Company has good revenue visibility.

-> Majority of the capex will be done from internal accruals since cash flow is strong.In case the need arises will look to raise some money via debt as well.Company is getting it at 7.5-7.7% rates.D/E stands at 0.55x,don’t see it going above 0.75x.

The management sounded far more upbeat than Q4 call.Overall also,the outlook for the industry profitability and revenues seems to have improved meaningfully.

Disc.: Invested.Views are biased.

28 Likes

1 Like

Aarti Drugs Q1FY20 Concall

We’ll be dividing this note in Business, risk, management and my view of the company

Business

-

API is 85% of sales and formulations is the rest.

-

Consolidated Topline saw a growth of 34% (544 crore)

-

Capacity utilisation at 75-80%

Api segment

-

In API segment, 65% of the sales come from domestic side and rest from exports. Domestic markets saw growth of 28% and exports saw growth of 29%.

-

Around 50% growth in API was due to volume growth.

-

API therapeutic category:

Antibiotic: 46%

Anti-Protozoal: 16%

Anti-inflammatory: 13%, increased from 10% on account of capacity enhancement

Anti Diabetic : 10%

Anti Fungal: 5%

Speciality and intermediates: 5%

-

Additional capex planned for anti-diabetic therapy towards the end of FY21.

-

Lot of discontent with Chinese suppliers. Demand shifting to Indian API and forsee the trend for next 3-5 years.

-

Top 12-13 products, leading manufacturer in India in all of them barring one. Some increase in margins can be sustained.

-

Volume growth to be much better in Domestic Api business going forward.

-

PLI can also be applied on brownfield capex, if we are setting up a new line of production. Not only limited to Greenfield capex.

-

Going forward, EBITDA margin trajectory has improved structurally. Earlier, used to guide for 15.5%, now 18-20%. As competitors in China are also increasing the prices. Have introduced a lot of products which are import substitutes in the market.

-

Only 1 product i.e. Ofloxacin benefits from Anti-dumping duty (renewal in next year March)

-

Peak potential turnover in API with current capacity and Capex in FY21 could be 2000-2200 crores.

-20% of Raw material is procured from China.

Likely Capex

-

Have 3 land parcels ready for expansion.

-

Likely to invest 300-400 crores in capex in next 3 years. Mainly for backwards integration and a lot of products that can be manufactured under PLI scheme.

-

Speciality chemical capex to be complete by FY23. (Also indicated facility might be ready by FY22 end)

Formulation business

-89% topline growth and 50% of sales come from exports.

-

Major growth in exports, earlier was mainly domestic focused. A lot of product registrations are expected to be approved and entering more markets.

-

Product mix is improving and see higher Gross margins as compared to historically.

-

Current quarter increase in gross margins was mainly due to institutional orders .

-

For coming quarter, a lot of open orders for formulation there. And have exclusive 3rd party tie ups for manufacturing.

-

No major capex in this segment, only investment to be done in R&D and Marketing.

-

Selling formulations via business partners in Row and other geographies. Going forward, we have a subsidiary in Latin America. Formulation business to be done as a front end business there rather than a B2B business. Targeting institutional and private retail market business.

-

Total potential turnover in Formulation business with current capacity could be 300 crores. But, this number is not relevant as they have exclusive 3rd party manufacturers for the same.

Management

-

Willing to pay a premium of 2-3 % for Indian suppliers as Chinese supply is erratic.

-

Expect EBITDA margins to sustain between 18-20%

-

For Usfda inspection: reached out to several people, FDA wants us to get all our changes audited by an external auditor and only then they will inspect. Timeline : August end to reply and get the auditing done. Most likely, auditor to be an ex FSA inspector from which a certificate is required to apply for reinspection of the the plant at Tarapur which runs at less than 50% utilisation

-

Asset turns are at 3-5x and in the long run can expect 20-25% Roce.

-

Margins likely to have moved up structurally. Likely to end year with 18-20% EBITDA margin.

-

Strategy of the company since 2013 has been import substitution.

-

Have got product approvals from Europe, where margins are better.

Risks

-

EBITDA Margins at 25%, due to increase in pricing of certain APIs. Can compress going forward.

-

Gross margins were also higher in Formulation business on account of higher institutional sales.

-

Tarapur inspection, Still caught up in Logjams.

-

20% RM dependence on China.

-

Net working capital went up by 100 crores.

My view seems well poised for any uptick in API production and can benefit out of PLI. One thing to watch out for is Asset turns, something seems a miss, asset turns cannot be 3-5x for a manufacturing company. Need to check.

No recommendations

16 Likes

Interesting Business of Aarti drug !

Few more hidden positive points found out from Analytical reports:

API consists of 85% of total sales and 65% of API Sales from domestic…which implies that 35% API sales from exports…And most of the exports are to Asian countries…So USA exposure and regulatory risk from USA as of today is minimal !

API growth from both domestic and exports @28-29% implies it is not only India , even other countries are reducing their exposure to China…So clearly Good days ahead for indian API makers if this attitude towards China is here to stay…

Risks

If there is a change in sourcing strategy of generic drug manufacturers of India and other Asian countries…

Raw material from China is still at 20%

Discl: Invested…may be biased

2 Likes